The Good Daughter that You Hate

About This Article

Many American families are in crisis when a parent, due to declining health or age, need long-term health care. The consequences are more than financial. One child must step up, and they wonder why this burden was placed on them

Linda Maxwell

Linda Maxwell is a journalist who writes about aging, health, chronic illness, caregiving, and long-term care issues impacting older adults and their families.

It happens to other families, certainly not ours. Those were the thoughts of Carol, a 54-year-old mother of three from Wichita who recalls the three-year nightmare her family has been living in since her mother had a stroke.

"My mom was an active and healthy 75-year-old. I usually spoke with her every morning before leaving for work. I remember that morning as she didn't answer the phone. That was unusual. Even if she started her day early, she would always answer or quickly call back," Carol explained.

That morning would be very different for Carol, her mother, and the rest of her family. Carol texted her mom before getting into the car for work. Carol's mom, Barbara, used her smartphone to text and take and send photos. Carol knew her mom would respond fairly quickly. This day things would be different.

"There was no response at all, and now it's lunchtime. I called again and no answer. Now am I officially worried," Carol explained.

Worry Turns into Crisis

Carol called her sister and expressed her concern. Carol's sister Valerie seemed less concerned, but her husband Ryan, who is a computer technician, agreed to drive to her house and check on her. What Ryan discovered would change everyone's life.

As Ryan pulled into the driveway, he noticed the garage door was open with the car in the garage. He took short steps as he approached the garage, looking around to see if anything was unusual. As he got closer, he saw Barbara on the floor of the garage next to her car. Her purse next to her with the contents scattered all over.

"My brother-in-law ran up and found her still alive but non-responsive. He called 911. The paramedics arrived quickly. Ryan said it seemed like it was less than two minutes before he heard the sirens as the police, fire department, and the ambulance arrived. The paramedics said it appeared to have been a stroke. He called, and we all left for the hospital," Carol said.

Barbara spent a week in the hospital with three days in the ICU. Barbara's doctor and the hospital case manager wanted a meeting with Barbara's family.

The Conference Room Meeting

Carol's husband Mike, her sister Valerie and her husband Ryan, and Carol's brother Eric, who flew in from San Diego, sat in this conference room at the hospital’s ICU unit. None of them were sure what would happen next.

"We all thought that Mom would recover and go back to her very active life. She was involved in everything. She volunteered at the church. She had her poker club; yes, all these older retired women loved to play poker. They all played with pennies just for fun. They said playing bridge was for older people. She walked her little poodle. Mom was full of life," Carol said.

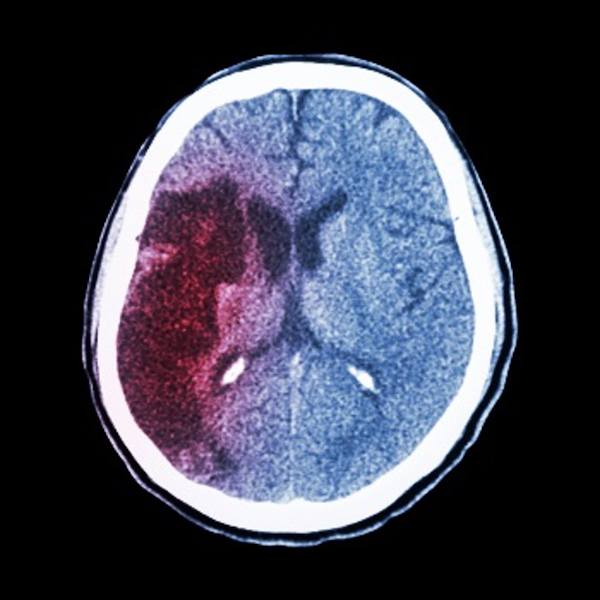

Life changed forever that day when Barbara had a significant stroke as she was getting into her car. The neurologist and three other doctors, and the hospital case manager explained the extent of the stroke.

Impact of the Stroke

The doctors said the stroke occurred on the right side of the brain. It left partial paralysis on her left side, some vision problems with one eye, and apparent memory loss. The doctors told the family that about one-third of all stroke victims experience problems with memory in addition to any physical issues they may experience.

This vascular dementia was going to change Barbara's life and that of her family dramatically. She will need rehabilitation to try to improve some of her functional and cognitive loss. However, the doctors said Barbara's likelihood of full recovery was slim. She would need long-term health care for the rest of her life. It would not be easy and could be very costly.

"We were all frozen as the doctors left. The hospital case manager explained that they would transfer Mom to a rehabilitation facility. When we asked what happens after that, the case manager started asking questions," Carol said.

The case manager asked who had medical and financial power-of-attorney. She wondered if Barbara owned Long-Term Care Insurance. She asked about the financial resources available to pay for a nursing home or in-home care.

"We never had these discussions. Mom was healthy. She was active. We never thought about what would happen because it wasn't going to happen. When Dad died, she bounced back, lost weight, and really started to live life to the fullest. We were very proud of her. My brother asked onetime about 'her plans,' and her response was nothing was going to happen, and she quickly changed the subject," she explained.

Daughter to Caregiver

Today Carol is the primary caregiver. Barbara has some savings they use to get caregivers to come in for about eight hours per day. Carol's sister Valerie helps a few hours each day as well. Mike, who lives in San Diego, likes to 'bark orders' from afar.

"This has become my responsibility. I was able to go part-time at work, so I have some time to be the caregiver. My sister can't do it. My brother just tells us the things we are doing wrong. My family never sees me, and I wonder why Mom didn't plan for this. At one point, I thought she hated me since she knew I would do all of this for her. But did she realize how difficult it would be? It isn't easy. I know she is suffering, but the rest of us are suffering as well," Carol said.

Carol's role as the primary caregiver is physically and emotionally demanding. Carol knows in her heart that her mom doesn't hate her. Nobody knows if Barbara ever thought about the consequences of aging and the costs and associated burdens that long-term care would have on her daughters and her son.

No Plan Means Family Crisis

Unfortunately, Carol's feelings are not that uncommon, nor is the family strife that occurs in this type of crisis. It is one of the adult children who take on caregiving's primary responsibility and managing any paid services.

Health insurance, including Medicare and supplements, will only pay for a small amount of skilled long-term care services. Medicaid, the medical welfare program, only pays when a person has little or no assets and income. In the absence of advance planning, the financial responsibility is placed on the person who needs care. The remaining responsibility falls on the family, usually a daughter or daughter-in-law.

Carol and her siblings know that Barbara didn't want them to carry this burden. Barbara's lack of planning was not out of hate or unconcern. Today's sandwich generation, those who are caring for a parent and their own children at the same time, are experiencing the consequences of long-term health care.

Long-Term Care Insurance Eases Future Family Burdens

As a result of this personal experience, many couples in their 40s and 50s are putting Long-Term Care Insurance into place, so their adult children don't face the stress and burden like Carol and her family are experiencing right now.

Think about which one of your children will take responsibility decades from now when your health starts to decline. How will your children interact with each other? Think about how the role of being a caregiver will affect their career, spouse, and children.

You probably don't hate your children. You probably do not want to intentionally burden them in the future. Caregiving is hard on your loved ones. Caregivers face health issues and anxiety. The cost of paid long-term health care is expensive. Even wealthy people can feel the pinch. Plus, the costs continue to increase with ever greater demand for services and fewer caregivers and facilities offering care.

The LTC NEWS Cost of Care Calculator will show you both the current and future cost of care services where you live.

LTC Insurance is Affordable but Be Careful When Shopping

Some people think Long-Term Care Insurance is prohibitively expensive. Some companies offer expensive policies, but premiums can vary over 100% between insurance companies. An experienced Long-Term Care Insurance specialist can review all the major companies and help you select the most affordable option based on your age, health, family history, and other factors.

There are several types of policies a person can choose. However, some policies are not Long-Term Care Insurance policies at all. Unqualified insurance agents or financial advisors who lack understanding will sometimes recommend an inappropriate or too expensive product.

Avoid the mistake of using a general insurance agent or financial advisor. Seek the help of a Long-Term Care Insurance specialist representing the industry's major companies and has substantial experience in this area. Experience is not calculated only in years. Experience is the number of clients that the agent has helped obtain Long-Term Care Insurance. A few hundred is good; however, top specialists have thousands of clients.

Find a trusted and experienced Long-Term Care Insurance specialist by clicking here.

Carol and her husband, and her sister Valerie and her husband are purchasing Long-Term Care Insurance because of what they witnessed with their mom. Their brother Mike was not convinced at first but now understands the importance of having a policy. Carol reminded him he was not providing Barbara's care and was not dealing firsthand with the consequences.

Aging Happens

Their families will enjoy peace-of-mind. No matter how healthy we may be today, we will experience changes in our health due to an illness, an accident, or the consequences of aging. Our bodies and minds decline over time.

We have more longevity than ever before. Preparing for the financial costs and related burdens of aging is an essential part of retirement planning. However, long-term care is not only a cash flow problem. It is a family problem. We cannot prevent aging. Aging happens. We can prepare for the consequence of aging and the related changes in our health.

Sponsored