Morbidity vs Mortality – Impact on Family & Assets

About This Article

Every stage of life has concerns. As we get to our fragile 50s, planning for the financial costs and burdens of aging becomes a key part of retirement planning. Have you thought about longevity?

James Kelly

LTC News staff writer specializing in long-term care and aging.

Remember when you were younger? You got out of college, landed that first great job, and started a family. While not everyone does those things precisely in that order, the big concern when you are younger is mortality. An early death creates a financial disaster for a spouse and children.

Mortality is the term used for the number of people who died within a population. Early death can be caused by an accident or a sudden or chronic health illness. Life insurance is often used to manage the risk of early death to protect your family from the loss of income from the person who passed away.

Everyone is Getting Older!

As you get older, so does your family. Your children get into college and graduate and start to have their own careers and families. Your concern for mortality becomes more personal but has less of an impact on your family's finances.

It's at this time when morbidity comes into the picture. Morbidity refers to the state of being diseased or unhealthy within a population. Once you get into your "fragile 50's," you start having health issues that begin to increase your morbidity risk. It may start with high blood pressure, high cholesterol, a few extra pounds, arthritis, and joint problems, and it continues from there.

Our Body Gets Fragile with Age

Morbidity means long-term care. As we age, the human body gets more fragile. However, advances in medical science allow us to live longer. The health issues that used to kill us no longer do. These two things add up to greater longevity. With longevity comes a much higher risk of needing long-term care services and supports. Long-term care is help with normal activities of daily living – otherwise known as ADL's.

These ADLs are the things we take for granted today and learned when we were very young. They include eating, dressing, bathing, transferring from one location to another, going to the bathroom, and holding our bowels.

At some point, due to illnesses, accidents, or the impact of aging, we will need help with these activities or require supervision due to cognitive decline. Cognitive deterioration comes in many forms, including Alzheimer's or other forms of dementia.

Who Will Take Care of You in the Future?

This "morbidity" requires planning to address the financial costs and burdens that come from aging. Who pays for long-term care services? You do. Health insurance and later, once you are 65, Medicare and any Medicare Supplement you will carry, will only pay a small amount of skilled care. The problem is most people require "custodial care." Custodial care is the help with ADLs or supervision due to cognitive decline.

The cost of these services can drain even a substantial amount of assets. Most long-term care services are at home, adult day care, assisted living, or memory care.

Long-Term Care Services are Expensive

All of this is not cheap. But the most expensive type of long-term care service is skilled nursing home care. According to the LTC NEWS Cost of Care Calculator, the national average for skilled nursing homes in the United States runs over $105,000 a year.

If you are age 55 today, the cost of this same nursing home, based on past trends, will run nearly $200,000 a year when you are age 80. How much of a dent will that have on your lifestyle?

Other forms of long-term care are not cheap, either. According to the LTC NEWS cost of care calculator, a 44-hour week of home care now averages over $53,000 a year. In 2042 this will average over $102,000 a year!

How about assisted living? The national base average runs today over $51,000 a year. In 2042, just 25 years from now, it will average over $98,000 a year. Keep in mind this is the base cost. The total cost will be reflective of the amount of ADL assistance or supervision you require.

Find Cost of Care in Your Area

The cost of care does vary depending on where you live. You can find the current and future cost of care services where you live by using the LTC NEWS COST OF CARE CALCULATOR. Click here to use this tool.

The CDC reports one in four adults has a disability. Not every disability requires extended care services, but as we age, this risk does increase.

The figure above is a bar chart showing that in 2016, aides provided more hours of care in the major sectors of long-term care than the other staffing types shown. Aides accounted for 59% of all staffing hours in nursing homes, compared with licensed practical or vocational nurses (21%), registered nurses (13%), activities staff members (5%), and social workers (2%). Aides accounted for 76% of all staffing hours in residential care communities, in contrast to activities staff members (10%), registered nurses (7%), licensed practical or vocational nurses (6%), and social workers (1%). In adult day services centers, aides provided 39% of all staffing hours, followed by activities staff members (30%), registered nurses (15%), licensed practical or vocational nurses (9%), and social workers (6%).

QuickStats: Percentage Distribution of Long-Term Care Staffing Hours, by Staff Member Type and Sector — the United States, 2016. MMWR Morb Mortal Wkly Rep 2018;67:506. DOI: http://dx.doi.org/10.15585/mmwr.mm6717a6

Most long-term care services are provided in the community … mostly in a person’s own home.

For those receiving benefits from Long-Term Care Insurance, you see most claimants are receiving care at home. The American Association for Long-Term Care Insurance (AALTCI) study of claims from these policies shows 52.1 percent of all new claims in 2017 began in the home setting.

"People mistakenly associate Long-Term Care Insurance exclusively with skilled nursing home care," said Jesse Slome, the director of the AALTCI. The AALTCI is a national education and advocacy group.

The AALTCI says the industry's major insurance companies paid over $11 Billion in claim benefits in 2019, helping American families access their choice of quality care at home or in a facility. These benefits give the family members time to be family and not hold the role of being Mom or Dad's caregiver.

The National Association of Insurance Commissioners (NAIC) LTC Experience Report (May 2016) says that from 1994 to 2014, slightly less than $100 Billion in claims have been paid to American families. The NAIC study also shows those with Long-Term Care Insurance receive more paid care at home than those who don't.

Your chance of needing long-term care services is a significant risk as medical science continues to give us longevity. Not everyone will need formal or informal care, but this risk increases with age.

Hospice

It doesn't end there. The same forces that cause more of us to require long-term care also impact end-of-life. Hospice has become an essential part of our end-of-life. Medicare does have hospice benefits, but often you may need more services and for more extended periods. Long-Term Care Insurance will pay for hospice services at home or in a facility if required.

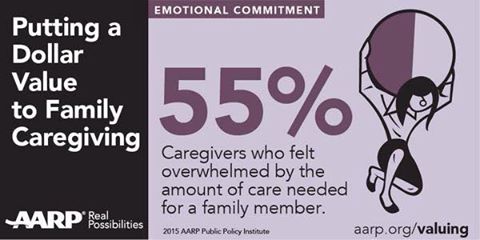

If you think your family can be caregivers – think again. Caregiving is tough work. It adds a tremendous amount of stress, both physically and mentally, to loved ones. Also, keep in mind your adult children have their own careers, families, and responsibilities. Being a caregiver is probably not the best plan to address longevity issues.

Just like you probably did when you were younger and planned for your early mortality with some life insurance, now you need to prepare for mortality – the longevity problems caused by aging due to illnesses, accidents, or just getting old.

LTC Insurance Protects Savings and Eases Family Burdens

Long-Term Care Insurance is a tool recommended by experts. There are three types of plans:

- Traditional – This is a pure insurance contract with tax advantages, low premiums if you plan before retirement and partnership benefits that provide additional asset protection in most states.

- Asset-Based or "Hybrid" – This is either a life insurance policy or annuity with a rider covering long-term care services. While many require you to be "terminal," the best ones have the same long-term care triggers as the traditional plans. For some people, the big selling point is the death benefit if you're lucky enough never to need long-term care. If you own a life insurance policy or annuity with enough cash value, you can complete a "1035 tax-free exchange" to one of these policies.

- Short-duration – This is a mini-policy that will cover a year, sometimes two of long-term care. Some of these plans only cover care at home; others include facilities. Generally, they have reduced underwriting criteria as well.

A qualified Long-Term Care Insurance specialist can make the proper recommendations for you based on your situation. They should take the time and ask many questions about your health, family history, finances, and retirement plans and your general concerns about how your family may – or may not be involved in your future care.

Premiums are Affordable but Seek Specialist to Help

Premiums are actually very affordable for most people. Key to premium costs is your age at application, your health, and the total benefits you wish to apply. Averages published in articles are often very exaggerated. If you purchase in your 40s or 50s, you can obtain outstanding coverage for $150 a month or less. Premiums can vary widely based on company and policy design. Since premiums vary so much for the same coverage, be sure to seek a specialist who works with multiple companies and has experience in policy design and claims.

LTC NEWS can help you find a licensed specialist representing all the major companies, has substantial knowledge of underwriting, policy design, and claims. Find a trusted and experienced Long-Term Care Insurance specialist by clicking here.

The best time to plan is before retirement as you can enjoy much lower premiums and perhaps obtain preferred health discounts.

Nobody ever said life was easy. As we age, it really doesn't get any easier unless you plan in advance and give yourself and your family peace-of-mind.

Sponsored