Medicaid is Never the Goal or Solution for Long-Term Care Planning

About This Article

Be cautious of schemes that involve hiding or gifting assets to qualify for Medicaid’s long-term care benefits. Such strategies are often legally questionable and can trigger severe penalty periods under the Deficit Reduction Act. Proper planning protects assets and ensures quality care.

Linda Maxwell

Linda Maxwell is a journalist who writes about aging, health, chronic illness, caregiving, and long-term care issues impacting older adults and their families.

Table of Contents

- Medicaid: Not Your Default Long-Term Care Solution

- Why Medicare and Health Insurance Are Not Long-Term Care Solutions

- Reality: Most Care Is "Custodial"

- Medicaid Rules: Navigating the Financial "Deep End"

- What Medicaid Does Cover for Those with Limited Resources

- The Deficit Reduction Act (DRA): Closing the "Loophole" Culture

- LTC Partnership Program: "Dollar-for-Dollar" Protection

- Fact: Long-Term Care Insurance is Customizable and Affordable

- Stability and Protection: The Role of Rate Stability Rules

- Rise of Hybrid Policies: Life Insurance Meets LTC

- Frequently Asked Questions About Long-Term Care, Medicaid, and LTC Insurance

For many families, long-term care has long been a looming concern. While the COVID-19 pandemic intensified this issue and brought it to the forefront of national conversation, the most powerful motivator for planning is often personal. Most Americans have witnessed a loved one struggle with the physical challenges of aging or sudden health changes.

Recent data from the Department of Health and Human Services (HHS) clarifies the scope of this risk. While a broad majority of older adults will need some form of assistance, approximately 56% of individuals turning 65 today will develop a "severe" long-term care need.

Under the federal definition, this level of care is required when an individual needs help with at least two of the six activities of daily living (ADLs)—eating, bathing, dressing, toileting, transferring, and continence—or requires substantial supervision due to a severe cognitive impairment, such as Alzheimer’s disease.

The Role of the Family Caregiver

Without a formal plan, the burden of care typically falls on family members who become caregivers, either full-time or part-time. This role is often demanding, both physically and emotionally. According to 2025–2026 industry reports, the "sandwich generation"—those caring for both aging parents and their own children—faces the highest levels of stress and burnout.

Financial Reality

Relying solely on paid care services can create significant financial strain, potentially depleting retirement savings and impacting the standard of living for the entire family. Long-term care costs are increasing nationwide but the actual cost will depend on where you live and the types of extended care services you require.

The reality remains that traditional health insurance and Medicare typically do not cover long-term care. Medicare's coverage is limited to short-term skilled care, such as rehabilitation following a hospital stay. It does not pay for the long-term custodial care that helps a person with daily functions over months or years.

Without private Long-Term Care Insurance, these costs must be paid out-of-pocket from personal savings or managed by unpaid family caregivers, often at the expense of their own careers and health.

Medicaid: Not Your Default Long-Term Care Solution

The long-term care landscape has become increasingly complex. While Medicaid remains a vital safety net, it is frequently misunderstood by middle-class families as a "default" insurance plan.

While some online content portrays Medicaid as a universal answer for aging, it was never designed to be a primary insurance plan for those with savings. The claim that Medicaid is "long-term care insurance for the middle class" is fundamentally misleading.

The Original Intent vs. Modern Reality

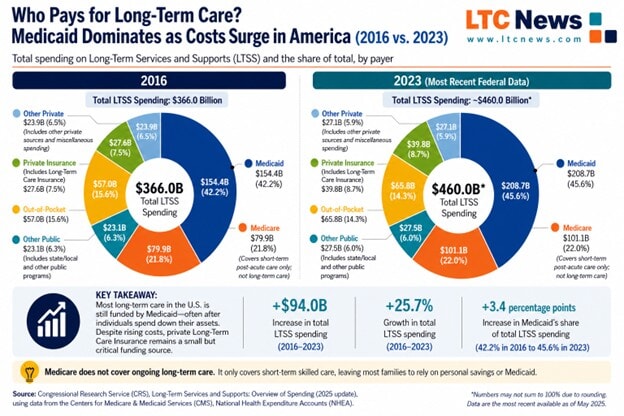

Medicaid was established as a public health insurance program for low-income individuals. While it has become the primary payer for long-term care in the U.S., it remains a needs-based program with strict eligibility requirements.

In 2026, those in the "middle-income squeeze" face the greatest risk: they often earn too much to qualify for Medicaid but do not have enough liquid assets to cover the skyrocketing costs of in-home care, assisted living, and private nursing homes, which now average over $117,000 to $132,000 per year.

Research: Use a zip code or city of town name to find current and prjected cost of long-term care services with the LTC News Cost of Long-Term Care Servcies Calculator.

The Strict Rules of the Deficit Reduction Act (DRA)

The Deficit Reduction Act of 2005 remains the governing force behind Medicaid eligibility. Its primary goal was to prevent individuals from transferring assets to heirs specifically to qualify for government-funded care.

-

The 60-Month Look-Back: State officials will review your financial history for the five years prior to your application. Any uncompensated transfers—including gifts to grandchildren, charitable donations, or assets moved into most trusts—can trigger a penalty.

-

The Penalty Period: If a transfer is flagged, you may face a period of ineligibility. Crucially, this penalty does not begin when the gift is made; it begins only when your assets have already been depleted (typically below $2,000 in most states) and you have officially applied for Medicaid.

-

Home Equity Limits: In 2026, most states limit home equity interest to between $752,000 and $1,130,000. If your home’s value exceeds these limits, it may be counted as a liquid asset, forcing a sale or preventing eligibility. These numbers are adjusted annually.

The Trade-Off: Choice and Quality

Beyond the financial hurdles, relying on Medicaid often means sacrificing control over your care.

-

Limited Provider Choice: You are restricted to facilities and agencies that accept Medicaid reimbursement. In 2026, many premier assisted living facilities and high-end nursing homes remain "private pay only."

-

Reimbursement Strains: Medicaid reimbursement rates to providers are significantly lower than private-pay rates. In a 2026 fiscal climate of rising labor costs, this disparity can lead to staffing challenges or reduced amenities in Medicaid-funded environments.

-

The "Spend-Down" Requirement: To qualify, you must effectively "spend down" nearly all of your life's savings, leaving a spouse (the "community spouse") with limited resources (the 2026 allowance is capped at approximately $162,660 in many states).

Most people are concerned with the quality of care, which some people say often lacks with Medicaid due to their low reimbursement rate for providers. A proactive approach can help you secure the care you need without jeopardizing your financial security.

The Kaiser Family Foundation reports that six in 10 nursing home residents are currently covered by Medicaid. While one in three people aged 65 and older will spend time in a nursing home, the definition of long-term care has expanded significantly. In 2026, more individuals are utilizing services in their own homes, adult day care centers, assisted living facilities, and specialized memory care units

Medicaid’s Shift Toward Community-Based Care

Historically, Medicaid primarily funded care within institutional nursing facilities. However, a major shift is underway. In 2026, nearly 70% of Medicaid’s long-term care spending is directed toward Home and Community-Based Services (HCBS). While this is good news, lack of providers willing to accept Medicaid reimbusrements is limited. Many peopel will wait for in-home care otpions or still be forced into a Medicaid nursing home.

Through federal waivers and state-level testing, community care programs are becoming more widely available. These programs aim to provide seniors with resources to age in place, though eligibility remains strictly tied to having little or no financial resources.

Key Utilization Trends for 2026

-

Nursing Home Occupancy: National occupancy rates for skilled nursing facilities (SNFs) have rebounded to roughly 81% in 2026, following the post-pandemic recovery.

-

Assisted Living Demand: Assisted living occupancy has reached a decade-high of over 87%, driven by a lack of new supply and a growing preference for "residential-style" care over traditional clinical settings.

-

Cost vs. Coverage: While states have expanded HCBS programs to reduce institutionalization, waiting lists for these community-based waivers remain common. For many, the transition to Medicaid still requires a total depletion of assets, often leaving nursing homes as the only guaranteed setting for care once funds are exhausted.

Why Medicare and Health Insurance Are Not Long-Term Care Solutions

Medicare remains a primary health insurance program for people 65 and older, but it is not a long-term care solution. It is designed to pay only for a limited amount of skilled services, such as skilled nursing care and rehabilitation, following a medical crisis.

"Medicare Gap": A Crisis for American Families

A dangerous and common misconception is that Medicare will act as a safety net for long-term care. In reality, this misunderstanding often leads to a "crisis point" for families. When an aging parent’s health declines—whether through a sudden fall or the slow onset of memory loss—adult children are often shocked to learn that Medicare provides almost no assistance for the help their loved ones actually need.

Data from LTC News and the U.S. Department of Health and Human Services highlights that Medicare only pays for short-term "skilled" care. It does not cover "custodial" care, which includes help with bathing, dressing, and supervision for those with cognitive impairments like dementia.

The 100-Day Rule and Its Limitations

In 2026, Medicare's rules for skilled nursing facility (SNF) care remain strict. To qualify for coverage:

-

You must have a "qualifying" hospital stay of at least three consecutive days as an inpatient (not including the day of discharge).

-

You must be admitted to a Medicare-approved SNF within 30 days of that hospital stay.

-

The care must be directly related to the same condition treated during your hospital stay.

Even if you meet these criteria, coverage is temporary. Medicare pays for up to 100 days of care per "benefit period." Once you run out of days or no longer require daily skilled care, Medicare coverage ends.

Rising Out-of-Pocket Costs

While Medicare pays the full cost for the first 20 days of skilled care, the financial responsibility shifts significantly thereafter. In 2026, the daily coinsurance for days 21 through 100 has risen to $217.00 per day.

While many people carry a Medicare Supplement (Medigap) policy to cover these daily deductibles, these supplements strictly follow Medicare’s rules. Once the 100-day limit is reached—or if the care is deemed no longer "skilled"—the supplement will also stop paying.

Reality: Most Care Is "Custodial"

A critical distinction for families to understand in 2026 is the difference between skilled care and custodial care.

What is Custodial Care?

The vast majority of long-term care is custodial. This refers to non-medical assistance with the six activities of daily living (ADLs):

-

Bathing

-

Dressing

-

Eating

-

Toileting

-

Transferring (e.g., getting in and out of a bed or chair)

-

Continence

Custodial care also includes supervision required due to a cognitive impairment, such as memory loss, poor judgment, or wandering associated with Alzheimer's disease or other forms of dementia.

Coverage Gap

The 2026 reality remains unchanged: Health insurance and Medicare do not pay for custodial care. If help with ADLs or supervision is the only care you need, Medicare will provide zero reimbursement.

Without private Long-Term Care Insurance, these costs must be paid entirely out-of-pocket from personal savings. While Medicaid does pay for custodial care, eligibility requires the near-total depletion of assets. A proactive plan ensures that you have the resources to pay for care in your own home or a facility of your choice without jeopardizing your financial legacy.

Medicaid Rules: Navigating the Financial "Deep End"

While Medicaid provides a critical safety net for long-term care, qualifying for it requires meeting strict financial eligibility tests. In 2026, the general rule remains that an individual can have no more than $2,000 in "countable" assets to qualify. However, some states have moved to expand these limits. Be cautious of legal schemes designed to hide or transfer assets to artificially qualify for Medicaid. While some "Medicaid planning" strategies promise to shelter your wealth, they often run afoul of the Deficit Reduction Act’s strict 60-month look-back period, leading to severe eligibility penalties and delayed care.

Beyond the legal risks, relying on Medicaid as a primary strategy severely limits your autonomy; you are often restricted to facilities with available Medicaid beds and lower reimbursement rates, which can impact staffing levels and overall quality. By circumventing federal laws instead of planning proactively, you sacrifice the ability to choose high-quality home care or premier assisted living, often resulting in a lower standard of extended care than private insurance would provide.

Understanding Asset Treatment

Some assets are excluded by law, such as a primary residence (up to certain equity limits), one vehicle, and basic personal belongings. For a more granular view, the LTC News Cost of Care Calculator provides state-specific Medicaid requirements and average care costs to help families visualize their potential financial exposure.

What Medicaid Does Cover for Those with Limited Resources

Medicaid does provide meaningful coverage for people with limited financial resources. It functions as a comprehensive health and long-term care program — but only for those who meet strict income and asset requirements. If you qualify, services must be obtained through approved Medicaid providers.

General Healthcare

For eligible individuals, Medicaid covers a broad range of routine and acute medical services, including doctor visits, preventive care, lab work, X-rays, and hospital stays — both inpatient and outpatient. Prescription drugs, medical equipment, and specialist referrals are also typically covered, depending on your state's plan.

Mental Health and Therapy

Medicaid includes coverage for mental health services, such as individual and group therapy, psychiatric evaluations, and counseling. Behavioral health treatment, including substance use disorder programs, is also available through approved mental health providers. Coverage varies by state, but federal law requires parity between mental health and medical benefits under Medicaid managed care plans. There are therapists who accept Medicaid, although availability depends on where you live. You may need a referral from your primary care physician to help find providers in your area who participate in Medicaid.

Long-Term Care Services

Medicaid is the largest payer of long-term care in the United States. For those who qualify, it can cover care in a nursing facility, as well as home and community-based services through state waiver programs. These services may include in-home personal care aides, adult day programs, and some assisted living support — all through Medicaid-approved providers.

A Safety Net, Not a Strategy

These services are real and, for those with genuinely limited financial resources, they provide critical support. But Medicaid was designed as a safety net of last resort — not a planning tool for middle-class families.

Qualifying means spending down nearly all of your savings. It limits your choice of doctors, facilities, and care settings to those willing to accept Medicaid reimbursement rates, which are significantly lower than private-pay rates. Many top-rated assisted living communities and home care agencies do not participate in Medicaid at all.

If you have assets to protect, Medicaid is not a solution — it is what happens when planning fails.

The Deficit Reduction Act (DRA): Closing the "Loophole" Culture

The Deficit Reduction Act of 2005 (often referred to as the DRA) fundamentally changed the landscape of long-term care by closing loopholes that allowed families to "hide" or give away assets to qualify for government assistance.

Key DRA Regulations for 2026:

-

The 60-Month Look-Back: State officials review all financial transfers made in the five years prior to a Medicaid application. Any "uncompensated" transfers (gifts) are flagged.

-

The Penalty Start Date: Under the DRA, the penalty period does not begin when you give the money away; it begins only when you are "otherwise eligible"—meaning you are already in a nursing home and your assets have fallen below the $2,000 threshold.

-

Treatment of Annuities and Notes: To prevent people from "sheltering" cash, annuities must now be actuarially sound and name the state as the remainder beneficiary. Similarly, promissory notes and life estates are heavily scrutinized and often treated as countable assets.

-

Home Equity Limits: In 2026, states generally limit home equity to between $752,000 and $1,130,000. If your home’s value exceeds these limits, you may be ineligible for Medicaid unless a spouse or dependent child still lives there.

-

Community Spouse Protections: To prevent the "impoverishment" of a spouse staying at home, the Community Spouse Resource Allowance (CSRA) allows them to keep a portion of the couple’s assets (up to approximately $162,660 in many states for 2026).

A Warning on "Gifting": While the IRS allows an annual gift tax exclusion (reaching $19,000 per person in 2026), Medicaid does not. Giving away $19,000 to a grandchild may be tax-free, but it will still trigger a Medicaid penalty period if done within the five-year look-back window.

LTC Partnership Program: "Dollar-for-Dollar" Protection

For middle and upper-middle-class families, the Long-Term Care Partnership Program is one of the most effective tools for protecting an estate. Now active in 45 states, this program was expanded by the DRA to encourage private planning over government reliance.

How "Asset Disregard" Works

Under a partnership-certified Long-Term Care Insurance policy, you gain dollar-for-dollar asset protection. This means that for every dollar your private insurance policy pays out in benefits, you can "shield" an equal amount of your personal assets from Medicaid’s spend-down requirements later.

-

Example: If your Partnership policy pays out $300,000 in benefits and you later exhaust those funds, you can apply for Medicaid and keep $300,000 of your own savings above the standard $2,000 limit.

-

Estate Recovery: These protected assets are also generally exempt from "estate recovery," meaning the state cannot seize them from your heirs after your death to repay the cost of your care.

The "Private-Pay to Medicaid" Transition

Using a Partnership policy also improves your choice of care. Many high-quality facilities that generally prefer private-pay residents are more likely to allow you to remain in the facility as a Medicaid resident if you have already spent several years paying their standard private rates through your insurance policy.

It is important to note that these are just a few of the changes that the DRA made to Medicaid's long-term care rules. If you are considering applying for Medicaid, it is important to speak with an attorney to understand the latest rules and regulations.

For many families, the decision to plan for aging comes down to a single factor: choice. While some financial strategies focus on asset manipulation to qualify for Medicaid, these methods often strip away an individual's autonomy. Today, a Long-Term Care policy remains the most effective way to maintain control over how and where you live without spending your assets and placing a burden on those you love.

Power of Autonomy

Unlike Medicaid, which often limits residents to specific facilities and shared rooms, an LTC policy provides the flexibility to select the setting that best fits your lifestyle:

-

In-Home Care: Maintaining independence in your own residence with professional help.

-

Adult Day Care: Engaging in community-based programs while living at home.

-

Assisted Living & Memory Care: Accessing residential environments that provide high-end amenities and specialized cognitive support.

-

Nursing Facilities: Choosing top-tier clinical care if intensive medical supervision becomes necessary.

👉 Learn more by reviewing the LTC News Long-Term Care Insurance Learning Center.

👉 Compare Long-Term Care Insurance Companies and Products

These policies are designed to cover both skilled and custodial care, ensuring that whether you need physical therapy or simply help with the activities of daily living, your benefits are available across the entire continuum of care.

Customization and Affordability in 2026

A common misconception is that long-term care insurance is prohibitively expensive. In reality, modern policies are highly customizable, allowing individuals to tailor coverage to their specific budget and needs.

Factors that influence the premium include:

-

The Daily/Monthly Benefit: Choosing how much the policy pays out toward care.

-

The Benefit Period/Pool of Money: Determining the amount of money in your policy to pay for your future extended care.

-

Inflation Protection: Ensuring your benefits keep pace with the rising cost of care over time.

Fact: Long-Term Care Insurance is Customizable and Affordable

The cost of a Long-Term Care Insurance policy is not a fixed price tag; it is a reflection of the choices you make during the design process. Premiums are primarily driven by your age and health at the time of application, but the ultimate cost is determined by the specific benefits you select. You choose a monthly or daily benefit and a benefit period or "pool of money" which is the amount ofmoney iwthin your policy to pay for yoru future extended care. However, other options will increase your premium if selected.

Protecting Against Rising Costs: Inflation Benefits

Because most people purchase a policy in their 50s or 60s but may not need care until their 80s, inflation protection is a critical component. In 2026, the most common options include:

-

Compound Inflation: Your benefit pool grows every year automatically, depednign on the company, from 1 to 5%, ensuring your coverage keeps pace with the rising cost of home health aides and long-term care facilities.

-

Simple Inflation: A more budget-friendly option where the benefit increases by a fixed percentage of the original amount each year.

- Options to Buy More: Your benefits only go up when you select the option every three years. However, your premiumn goes up as well.

The Elimination Period: Your "Time-Based" Deductible

Unlike traditional health insurance, which uses a dollar-amount deductible, LTC Insurance uses an elimination period. This is a waiting period—measured in days—that must pass before the insurance company begins paying benefits.

-

Common Choices: 30, 60, or 90 days.

-

The Strategy: Choosing a longer elimination period (such as 90 days) can significantly lower your annual premium. You essentially agree to "self-fund" the first few months of care from your own savings in exchange for a lower ongoing cost for the policy. This options is most often used as Medicare will pay up to 100 days of skileed care.

Tax Advantages

To further improve affordability, the IRS has increased the tax deductibility of LTCI premiums for 2026. For those ages 51 to 60 uo to $1,860 of your premium is eligible. For over age 60, as much as $4,960 of your annual premium may be considered a deductible medical expense. If you are over age 70, that limit increases to $6,200. Health Savinsg Accounts can be used to reimburse yourself the cost of your LTC policy. The same IRS limits apply as well.

For many, securing suitable coverage can cost under $150 monthly, with rates potentially dropping for those younger and in prime health. Couples often benefit from available discounts, and shared benefits are an option for spouses or partners. Some policies even come with death benefits.

For those with substantial assets, a heftier policy might be more fitting.

Options to choose policies with unlimited benefits are also on the table. Regardless of the policy's scale, many offer value-added features, including professional case management for most. Such provisions assist policyholders and their families devise care plans and coordinate care services, significantly easing the potential strain on loved ones. See for yourself the actual cost of LTC Insurance by reviewing our survey of premiums from all the top-rated isnurance companies offering these policies - How Much Does Long-Term Care Insurance Cost?

Stability and Protection: The Role of Rate Stability Rules

One of the most significant advancements in the LTC Insurance market is the implementation of Rate Stability Rules (also known as the NAIC Model Regulation). These rules were designed to protect consumers from the large, unexpected premium hikes seen in older "legacy" policies from the 1990s and early 2000s.

How Rate Stability Works Today

In states that have adopted these protections, insurance companies are held to much stricter actuarial standards. Before a company can issue a new policy, they must:

-

Price for the Long Term: They are required to set premiums based on conservative assumptions, such as near-zero lapse rates and sustained low interest rates.

-

Eliminate "Profit" from Hikes: If a company requests a rate increase later, they are generally prohibited from including a profit margin in that increase.

-

Actuarial Certification: Companies must provide certifications that their current pricing is sufficient to cover anticipated claims without the need for future increases under normal circumstances.

While no policy is strictly "guaranteed" never to increase, these rules make it significantly more difficult for insurers to raise rates on modern policies.

Rise of Hybrid Policies: Life Insurance Meets LTC

As of 2026, hybrid policies (also called "linked-benefit" or "combination" policies) have become the most popular choice for professionals planning for retirement. These plans combine the benefits of a life insurance policy or an annuity with a long-term care rider.

Why Hybrids Are Often Considered

-

With a hybrid policy, if you never need care, your heirs receive a tax-free death benefit. If you do need care, you can access your death benefit early to pay for it. However, that death benefits pays the long-term care benefit until it is exhausted so if you need long-term care, there is little or no death benefit.

-

Guaranteed Premiums: Unlike traditional policies, hybrid plans almost always come with a guaranteed premium. Whether you pay in a single lump sum or through an ongoing "multi-pay" plan, your rate is locked in and will never increase.

-

Return of Premium: Many hybrid designs include a "exit strategy" that allows you to surrender the policy and receive a portion—or sometimes all—of your original premium back if your plans change.

-

Asset-Based Versatility: These policies can be funded by repositioning existing assets, such as idle savings or 1035 exchanges from old life insurance policies, providing a way to leverage "lazy money" into a robust care fund.

- Because your are combining life insurance (or annuities) with a qualified long-term care benefit the premium is usually muich higher.Seek a qualified Long-Term Care Insurance specilaist who represents all the top-rated traditional and hybrid plans to see which one is best in your situation.

Expert Recommendation

Long-term care planning experts suggest that the "sweet spot" for long-term care planning is in your 40s or 50s. In fact, most people acquire Long-Term Care Insurance between the ages of 47 and 67. Planning during this window offers several advantages:

-

Lower Premiums: Rates are age-based, and locked-in early.

-

Health Eligibility: You are more likely to qualify for "preferred" health discounts before age-related conditions develop.

-

Compound Growth: If you select an inflation rider, your benefit pool has more time to grow, ensuring you have the maximum funds available when you actually need them.

Frequently Asked Questions About Long-Term Care, Medicaid, and LTC Insurance

What is long-term care and who needs it?

Long-term care refers to ongoing assistance with daily activities such as bathing, dressing, eating, and mobility, or supervision due to cognitive impairment like Alzheimer’s disease. According to the U.S. Department of Health and Human Services, about 56% of people turning 65 today will develop a severe long-term care need, requiring help with at least two activities of daily living or significant cognitive support.

Does Medicare cover long-term care?

No. Medicare does not cover ongoing long-term care. It only pays for short-term skilled care, such as rehabilitation after a hospital stay, and only under strict conditions. Coverage is limited to up to 100 days, and only if the care is medically necessary and skilled. Custodial care—the type most people need long term—is not covered.

What is custodial care and why does it matter?

Custodial care is non-medical assistance with everyday activities like bathing, dressing, eating, and supervision for memory loss. This is the most common type of long-term care, and it is not covered by Medicare or standard health insurance, making it a major financial risk for families.

How do most people pay for long-term care?

Most people pay for long-term care through a combination of:

- Out-of-pocket savings

- Unpaid family caregiving

- Medicaid (after assets are depleted)

Without Long-Term Care Insurance, many families must spend down their savings before qualifying for Medicaid, often limiting care options.

Is Medicaid a good long-term care solution?

Medicaid is a safety net, not a primary planning tool. It has strict income and asset requirements, typically requiring individuals to have less than $2,000 in countable assets to qualify. It may also limit your choice of providers and care settings, as not all facilities accept Medicaid.

What is the Medicaid 5-year look-back rule?

The Medicaid look-back rule reviews financial transactions made in the 60 months (5 years) before applying. If assets were gifted or transferred below market value, it can trigger a penalty period of ineligibility, delaying access to benefits.

What happens if you don’t plan for long-term care?

Without a plan, the burden often falls on family members. Today, 63 million Americans provide unpaid care, often balancing careers and caregiving responsibilities. This can lead to emotional stress, financial strain, and reduced quality of life for both caregivers and loved ones.

What is Long-Term Care Insurance and how does it help?

Long-Term Care Insurance helps cover the cost of extended care services, including:

- In-home care

- Assisted living

- Memory care

- Nursing homes

It allows you to protect your savings, maintain independence, and choose where you receive care, rather than relying on Medicaid.

What is the Long-Term Care Partnership Program?

The Partnership Program allows you to protect assets dollar-for-dollar based on the benefits your policy pays.

Example:

If your policy pays $300,000 in care, you can keep $300,000 in assets and still qualify for Medicaid later.

This helps preserve your financial legacy while ensuring access to care.

How much does long-term care cost in 2026?

Costs vary by location, but in 2026:

- Nursing homes can exceed $117,000 to $132,000 per year

- In-home care and assisted living costs continue to rise

You can estimate costs in your area using the LTC News Cost of Care Calculator, which provides real-time and projected pricing based on your ZIP code.

When should you consider Long-Term Care Insurance?

Most experts recommend planning in your 40s to 60s, when:

- Premiums are lower

- Health eligibility is better

- Benefits have more time to grow with inflation

Waiting too long can result in higher costs or disqualification due to health conditions.

What is the biggest mistake people make with long-term care planning?

The biggest mistake is assuming:

- Medicare will cover it

- Medicaid will be easily available

- Or that savings alone will be enough

In reality, long-term care is one of the largest financial and emotional risks in retirement, and requires proactive planning.

Share your thoughts and experiences about aging, caregiving, health, and long-term care with LTC News —Contact Us at LTC News.