Study: Nearly 4 in 10 U.S. Extended Families of Older Adults Include a Relative with Dementia

About This Article

A University of Michigan study finds that nearly 4 in 10 extended families with older adults in the U.S. include a relative with dementia, highlighting widespread impact and racial disparities.

James Kelly

LTC News staff writer specializing in long-term care and aging.

Nearly 40% of extended families that include someone age 65 or older in the United States have at least one relative living with dementia, according to new research from the University of Michigan’s Institute for Social Research.

The study, published in JAMA Neurology, provides a first-of-its-kind national estimate of the prevalence of dementia across multiple layers of American families.

The researchers analyzed data from the 2021 Panel Study of Income Dynamics, a nationally representative survey that tracks families over time. While 21 percent of individuals age 65 and older were found to have dementia, the prevalence increased to 26 percent when researchers considered households and immediate families. Among extended family networks, the figure jumped to nearly 37 percent.

This research highlights that dementia is not just an individual or household issue—it’s a widespread family concern. Many people are dealing with dementia in their family, even if it hasn’t directly affected their household yet." — Dr. Kenneth Langa, a professor of medicine and health policy at the University of Michigan.

Dementia Across Education and Racial Lines

The study also found significant disparities in dementia prevalence across education and racial lines. Older adults in families with lower levels of educational attainment were more likely to have a relative with dementia.

Black and Hispanic families were also disproportionately affected compared with non-Hispanic white families, raising concerns about unequal access to care and support systems.

Researchers argue these findings underscore the urgent need for public health policies that provide broader support to families, not just individuals living with dementia. They suggest that caregiver assistance, paid leave policies, and culturally appropriate resources are vital to managing the growing burden of dementia on American families.

This is a wake-up call. We need to think beyond the nuclear family and recognize the extended ripple effects that dementia has on communities, especially among marginalized populations." — Jessica Finlay, a research investigator at the University of Michigan.

Planning Not Considered

Researchers failed to consider options like Long-Term Care Insurance and partnership LTC policies available in most states that offer additional asset protection.

It’s not surprising—many financial professionals still overlook long-term care planning and fail to explore the full range of options that different types of Long-Term Care Insurance provide." — Matt McCann, a leading expert on long-term care planning.

LTC Insurance offers affordable options to provide guaranteed tax-free benefits for paying for quality extended care, including in-home care. Many consumers don't think about long-term care planning until their health starts to fail, or a loved one already requires care services. By that time, however, few options are available, if any.

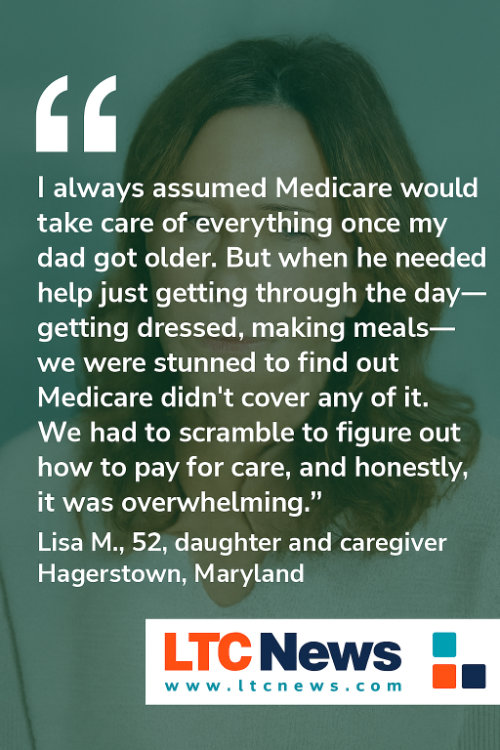

Medicare Doesn't Pay for Long-Term Care

Many people are shocked to learn that Medicare doesn’t cover most long-term care services. While Medicare helps older adults with hospital stays, doctor visits, and short-term rehabilitation after an illness or injury, it does not cover ongoing assistance with daily activities such as bathing, dressing, or eating—services that comprise the core of long-term care.

This misunderstanding often leads families to delay planning until a health crisis forces them to act.

You can share your thoughts and experiences about aging, caregiving, health, and long-term care with LTC News —Contact Us at LTC News.

Medicare may briefly cover skilled nursing care, but only under strict conditions. For example, it requires a qualifying hospital stay and only pays for up to 100 days in a skilled nursing facility—after that, patients are on their own. Even during those 100 days, full coverage only lasts for the first 20. After that, a Medicare supplement will pay through day 100.

Because Medicare falls short, families often turn to their savings or, once their assets are gone, to Medicaid, which does cover long-term care—but only for those with limited income and assets.

With the rising cost of long-term care services, being prepared is essential.

That’s why many Americans choose to prepare in advance with Long-Term Care Insurance, which can help protect retirement savings, provide access to better care options, and relieve the burden on adult children. Be sure to get accurate LTC Insurance quotes from all the top-rated insurance companies that offer long-term care solutions.

Planning early, ideally before retirement, while you’re still healthy, is the best way to ensure you’ll have choices and dignity when you need extended care.