State Filial Responsibility Laws Getting Kid’s Attention

About This Article

Filial responsibility laws have been around for a while. But now that Americans are living longer than ever and more require long-term care services, could they become another problem impacting families in the future?

James Kelly

LTC News staff writer specializing in long-term care and aging.

Filial responsibility laws have been around for a while. But now that American's are living longer than ever and more require long-term health care services and supports, these laws are getting a fresh look by cash-strapped states.

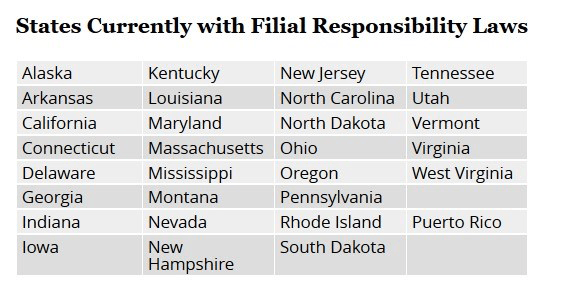

These filial responsibility laws impose a duty upon third parties, usually adult children, for the support of their impoverished parents or other relatives. Currently, 29 states and Puerto Rico have these laws in place.

Generally, family members usually are not responsible for a dead relative's debts, including long-term health care costs, unless they have co-signed a loan that is still unpaid. Assets given to a family member during the five-year lookback period for Medicaid qualification would still be considered the care recipient's asset and could be recovered by the state.

But could filial responsibility make adult children responsible for their parents' long-term health care costs? Perhaps.

This filial responsibility is going even further as a North Dakota nursing home recently sued the adult children for more than $43,000 in unpaid bills relating to their father's seven-month stay in the facility. They are not alone. Some facilities are seeking legal action to recover unpaid costs citing North Dakota's "filial support" law. The statute was adopted in 1877, a decade before North Dakota became a state. Filial statutes are modeled after England's Elizabethan Poor Laws of 1601.

Read the story here: Little-known law forces adult children to pay for nursing home care for parents

Will Your Kids Be Legally Responsible for Your Future Long-Term Care Costs?

Do you want your children decades from now held legally responsible for your future long-term health care costs if you no longer have sufficient financial resources to pay for it yourself? Until recently, these statutes have been largely ignored.

In addition to the actions in North Dakota, several recent court decisions around the country indicate that there might be renewed interest in enforcing them. Since most state budgets are under a severe financial strain, a lack of a long-term care plan might be placed on your loved ones.

If the legal action taken by these facilities in North Dakota becomes successful, you will see other nursing homes, assisted living facilities, and even home health agencies do the same thing.

Increasing Number of People Need Long-Term Health Care

Many of us will need help with activities of daily living or supervision due to memory issues like Alzheimer's. Unless you have an advance plan in place, your savings will pay the costs, for your adult children can become caregivers, something they are untrained and unprepared to provide.

If you have little or no assets, Medicaid will pay. Health insurance and Medicare, including Medicare supplements, will only pay for 100 days of skilled services. Otherwise, you will be responsible for these costs unless you own Long-Term Care Insurance. If you exhaust assets and don't pay all the bills, your adult children may end up being responsible. Certainly, your legacy will be adversely impacted by the expensive costs of long-term care services.

Most people obtain Long-Term Care Insurance in their 50s. Most states offer Partnership Long-Term Care Insurance plans that offer additional dollar-for-dollar asset protection, something many financial advisors are unaware of and don't talk about with their clients.

Keep in mind that the problem of declining health and aging is more than just a financial problem. Yes, be concerned about the cash flow issue that long-term health care costs create. But long-term care is also a family problem creating stress, anxiety, and burden for everyone.

There is an easy and affordable solution. Before you retire, add a Long-Term Care policy to your pre-retirement plan. Now you will have the resources to pay for your choice of quality care while protecting your savings. You won't have to ask your children to be caregivers (that won't work), and someone won't be seeking legal action against them to recover costs of care you were not able to pay.

Even if you live in a state that does not have filial responsibility laws, you probably still want to avoid sending hundreds of thousands of dollars on long-term care. You probably understand that caregiving is hard on family members as well.

LTC NEWS Cost of Care Calculator Great Tool

Planning in advance will give you and your family extra peace of mind. Start your research by finding the cost of long-term care in your state and the availability of tax incentives and state partnership programs - Cost of Care Calculator - Choose Your State | LTC News.

Be sure to plan before retirement so you can take advantage of low premiums and even preferred health discounts. Long-Term Care Insurance might be your answer to keep your kids out of the courtroom after you're gone.

Sponsored