Long-Term Care Getting Attention on 2020 Campaign Trail

About This Article

The campaign for President is in full swing. One of the big issues is health care, but this time around many candidates are talking about long-term care. Proposals include free care to additional tax incentives for Long-Term Care Insurance.

Linda Kople

Linda Kople is a freelance writer focused on caregiving, aging, health, wellness, long-term care, and retirement planning

At one point 20+ candidates were seeking the Democrat nomination to face President Trump in November. The issue of long-term care had captured the attention of candidates and voters alike. This attention has gained ground as a result of the COVID-19 pandemic. The virus crisis and the resulting market downturn illustrates the need for long-term care planning.

Currently, health insurance, including Medicare, pays only a limited amount of skilled long-term care services and nothing toward “custodial” care which is what most people end up needing at some point. People require long-term care due to illness, accident, or the impact of aging. The risk of needing care increases dramatically with age. The U.S. Department of Health and Human Services says if you reach age 65 you have a seven in ten chance of needing some long-term care service, including supervision due to cognitive decline.

Two Government Plans Today – Medicaid and LTC Partnership Program

Medicaid will pay for long-term care services, including custodial care, but only if you have little or no assets and income. The Long-Term Care Partnership Program, which currently 45 states participate in, provides dollar-for-dollar asset protection if you own a qualified Long-Term Care Insurance policy. This is a safety-net program that allows the person to qualify for Medicaid without exhausting all their assets. They can shelter part of their estate based on the total amount of benefits paid by the policy and still qualify for the Medicaid long-term care benefit.

“Medicare-for-All”

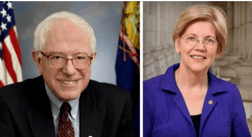

Much of the attention was focused on the so-called “Medicare-for-All” that Sen. Bernie Sanders has spearheaded in his campaign. This proposal was also embraced by Sen. Elizabeth Warren and Andrew Yang. Those proposals, which many on the Democrat side will still support, would eliminate private insurance and would include benefits for long-term care. While many argue the cost of this program would make it impossible to implement even with large tax increases, they claim it is the only way to provide adequate health care for all Americans.

Much of the attention was focused on the so-called “Medicare-for-All” that Sen. Bernie Sanders has spearheaded in his campaign. This proposal was also embraced by Sen. Elizabeth Warren and Andrew Yang. Those proposals, which many on the Democrat side will still support, would eliminate private insurance and would include benefits for long-term care. While many argue the cost of this program would make it impossible to implement even with large tax increases, they claim it is the only way to provide adequate health care for all Americans.

Klobuchar’s Long-Term Care Insurance Credit

However, Sen Amy Klobuchar, as a potential Vice Presidential candidate, may have influence on the policy plans of former Vice President Joe Biden. She had supported a program for those who are now in need of care or future care, as well as for those who wish to plan for their future care. She supported a tax credit for caregivers and private Long-Term Care Insurance. The tax credit can assist in paying for long-term care services and supports either at home or in a facility. It could also be used to pay for assistive technologies, respite care and required home modifications. She would pay for this credit with a new tax on certain types of investments. Klobuchar’s Long-Term Care Insurance tax credit would be equal to 20% of the total premium which can make premiums even more affordable.

However, Sen Amy Klobuchar, as a potential Vice Presidential candidate, may have influence on the policy plans of former Vice President Joe Biden. She had supported a program for those who are now in need of care or future care, as well as for those who wish to plan for their future care. She supported a tax credit for caregivers and private Long-Term Care Insurance. The tax credit can assist in paying for long-term care services and supports either at home or in a facility. It could also be used to pay for assistive technologies, respite care and required home modifications. She would pay for this credit with a new tax on certain types of investments. Klobuchar’s Long-Term Care Insurance tax credit would be equal to 20% of the total premium which can make premiums even more affordable.

Joe Biden and Long-Term Care

Former Vice President Joe Biden, now the presumptive Democratic presidential nominee, is talking about long-term care issues. Biden's plan includes tax relief to help solve the long-term care challenge. The plan provides tax benefits for those who purchase long-term care insurance as well as supporting caregivers who are providing care for family members.

Former Vice President Joe Biden, now the presumptive Democratic presidential nominee, is talking about long-term care issues. Biden's plan includes tax relief to help solve the long-term care challenge. The plan provides tax benefits for those who purchase long-term care insurance as well as supporting caregivers who are providing care for family members.

He wants to create a $5,000 tax credit for informal caregivers, modeled off of legislation supported by AARP. Informal caregivers – whether family members or other loved ones – provide much of the long-term care in the home.

The former Vice President says he will increase the generosity of tax benefits for people who choose to buy Long-Term Care Insurance and the ability to access qualified retirement accounts to pay for the premium.

President Trump – Tax Incentives for LTC Insurance – Expanded HSA

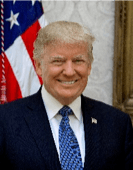

Meanwhile, President Trump had supported a tax credit for all health insurance as part of his tax plan, including Long-Term Care Insurance. However, the tax plan which was passed by Congress did not include that option.

Meanwhile, President Trump had supported a tax credit for all health insurance as part of his tax plan, including Long-Term Care Insurance. However, the tax plan which was passed by Congress did not include that option.

The President also supports an expansion of Health Savings Accounts. These pre-tax – tax-deferred accounts can be used for all types of health-related expenses including Long-Term Care Insurance. An expansion would allow more people to have these accounts and add more money than what is currently allowed.

The administration is looking into ways to increase the private Long-Term Care Insurance market. This would include additional tax incentives for Long-Term Care Insurance. At the moment, Long-Term Care Insurance premiums can only be deductible if you itemize (part of overall medical expenses), you are self-employed, or as a business expense for S Corporations, C Corporations, LLCs and other limited partnerships.

In March, speaking at the 19th Annual Intercompany Long-Term Care Insurance (ILTCI) Conference, several political insiders specializing in healthcare, from both sides of the aisle, agreed that a complete healthcare reform like Medicare-for-All would never be passed by Congress.

With long-term care, many people are in denial about their future need for long-term care. Yet, many American families are personally dealing with a parent or other family member who is receiving extended care services. Longevity will increase this risk in the decades to come.

LTC Insurance is Affordable for Many Americans

Some people assume Long-Term Care Insurance is expensive. However, as more people purchase plans before retirement, in their 40s and 50s, they are finding these policies are very affordable. Additional tax benefits will help make the costs even more affordable for more American families.

Premiums today are also rate-stable as many states have rate stability rules in place (click here to find your state). In addition, single premium products exist with death benefits in the event you never require care. While campaigns will come and go, the need to plan for the financial costs and burdens of aging remains a major part of retirement planning that needs to be addressed.