LTC-Life Settlements: Cashing Out Life Insurance Policies for Long-Term Care

About This Article

A life settlement can turn an unneeded life insurance policy into immediate tax-advantaged funds for home care, assisted living, memory care, or nursing home costs without fees or long delays.

Chris Orestis

Chris Orestis, CSA, is a nationally recognized expert on financial, health, long-term care, and retirement issues with over 25 years of experience in the insurance and LTC industries.

More than 136 million adults in the United States own some form of life insurance as of October 2025, a striking reminder of how central these policies are to financial security. What’s even more telling is that an estimated 46-48 million policyholders are age 60 or older.

What you may not be aware of is that these policies are no longer just about leaving a death benefit; they’ve become powerful tools for funding extended care, supplementing retirement, and preserving family assets.

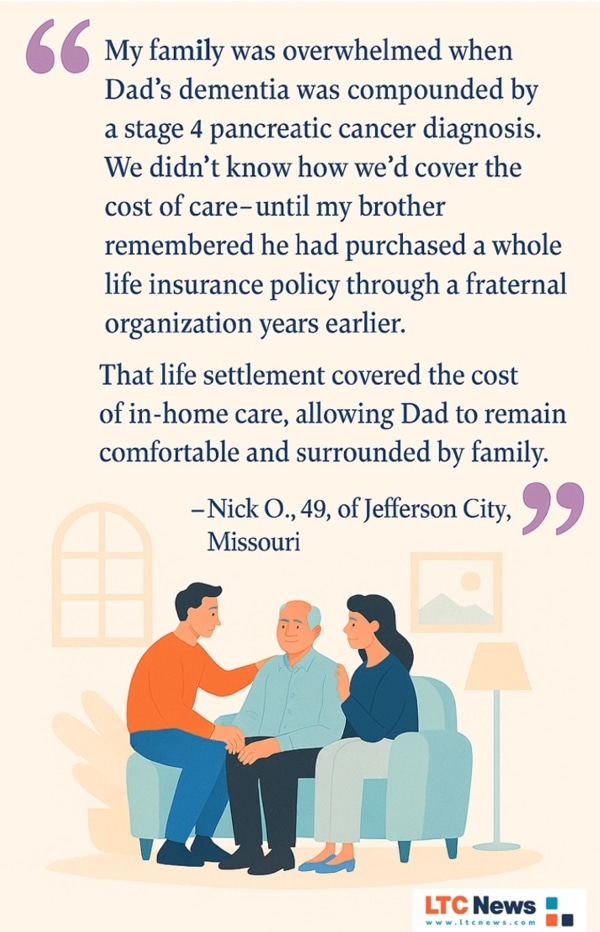

If you have an older spouse or parent, that life insurance policy can become very valuable right now. The owners of life insurance policies have had the right for years to sell their policies through a life settlement rather than abandon them after years of premium payments.

The money from these life settlements can be used while a loved one is alive. For someone who needs long-term care services and does not have a Long-Term Care Insurance policy, the proceeds from a life settlement can provide quality care and reduce some of the burden placed on the extended family.

What is a Life Insurance Policy Settlement

A life settlement is the sale of a life insurance policy by the original owner to a third party, who pays the owner a percentage of the death benefit while they are still alive. There are no out-of-pocket costs to the policy owner, and the process typically takes 60 to 90 days. Once the ownership of the policy is transferred, the original owner is no longer responsible for premium payments.

This strategy allows people to unlock the cash value of their policy later in life instead of letting it lapse unused. Because the settlement value increases with age and declining health, older policyholders often receive the most benefit.

LTC-Life Settlements for Long-Term Care

LTC-Life Settlements are a powerful financial tool for seniors who have a life insurance policy and need help paying for long-term care (LTC). This option can provide immediate funding for:

- Home care

- Assisted living

- Skilled nursing care

- Memory care

- Hospice care

Learn More: What Is Long-Term Care?

Unlike traditional Long-Term Care Insurance, annuities, or loans, LTC-Life Settlements eliminate waiting periods and the claims processes, allowing payments to begin immediately. Policyholders gain flexibility and control to address evolving care needs without bureaucratic delays.

There are also potential tax advantages. For policyholders with chronic or terminal conditions who meet specific medical criteria, such as needing help with two or more activities of daily living (ADLs) or having a life expectancy of two years or less, the proceeds can be received tax-free.* These funds are considered private pay, which can help delay Medicaid and count toward a Medicaid-qualified spend down.

How a Life Settlement Works

Most life settlements involve policyholders age 65 or older with a policy face value of at least $100,000. Settlement value is determined through “reverse underwriting,” meaning the older and sicker the insured, the higher the payout.

Typical candidates are between ages 75 and 92, though younger or older applicants can qualify depending on health conditions. Life expectancy for eligible applicants usually ranges from two to ten years.

Any in-force policy type can potentially qualify, including Term Life, Universal Life, and Whole Life. Settlement amounts often range between 10 and 50 percent of the death benefit, with the industry average around 22.5 percent.

Life Insurance: A Legally Recognized Asset

Life insurance has been legally recognized as an asset for more than 100 years, carrying the same personal property rights as real estate or stocks. Just as a homeowner wouldn’t walk away from their house without selling it, a policy owner should not abandon a life insurance policy without knowing its fair market value.

Lapsing or surrendering a policy leaves money on the table. A life settlement can unlock that value.

Ideal Candidates for a Life Settlement

Declining health plays a central role in determining eligibility and payout value. Qualifying is the opposite of applying for new coverage, the older and less healthy the insured, the higher the settlement. Someone healthy enough to qualify for new insurance usually won’t be eligible for a settlement.

For many seniors facing health or financial challenges, this can be a lifeline to help pay for extended care.

Why Life Settlements Matter

Life settlements are designed to maximize policy value while helping older adults address care costs, maintain independence, or preserve assets.

Settlement funds can:

- Pay for care at home or in senior living communities

- Supplement income

- Delay liquidation of investments

- Support estate planning goals

- Protect families from financial strain due to care costs

Fast Facts

- No costs to transact a life settlement; completion typically takes 60–90 days.

- Term Life, Universal Life, Whole Life, and Variable Life policies can qualify.

- Payouts range from 5% to 50% of the death benefit; the average is 20% to 25%.

- Older age and greater impairment increase payout value.

- LTC-Life Settlements can be a tax-free way to pay for care as part of a Medicaid spend down.*

- Over 260 million in-force life insurance policies exist in the U.S., with more than $20 trillion in death benefits.

- 88% of policies are at risk of lapse or surrender.

- An estimated $200 billion in death benefits could be settled annually.

- $4.5 billion in life settlement transactions are completed in the U.S. each year.

- Life insurance policies are legally recognized assets, with owners holding the right to sell.

- Typical life expectancy range for settlement eligibility is two to ten years.

- NAIC has endorsed life settlements as a private market option for financing long-term care.

Real-Life Case Studies

Case Study A: $100,000 Death Benefit — Assisted Living Move-In

A son helped his mother convert a life insurance policy they were about to abandon. Within 30 days, she received $2,000 monthly payments and moved into the assisted living community of her choice.

- $35,000 total LTC settlement

- $2,000 monthly payments for 18 months

Case Study B: $500,000 Term Policy — Home Care Funding

A policyholder facing declining health used an LTC-Life Settlement to fund skilled home care after rehab, avoiding a lapse and gaining immediate access to care services.

- $200,000 total LTC settlement

- $5,000 monthly payments for 40 months

Case Study C: $400,000 Universal Life Policy — Assisted Living Eviction Prevented

Facing eviction, the policy owner used settlement funds to pay for assisted living for three years.

- $175,000 total LTC settlement

- $4,000 monthly payments for 35 months

Case Study D: $100,000 Death Benefit — Family Relief Before Deployment

A son preparing for deployment helped his mother settle her policy before it lapsed, moving her into assisted living without delay.

- $39,000 total LTC settlement

- $2,100 monthly payments for 19 months

LTC-Life Settlement Q&A

Q: What types of care qualify?

A: You get cash, so it pays for all forms of care: home care, assisted living, memory care, nursing home, and hospice.

Q: Is this like Long-Term Care Insurance?

A: No. There are no waiting periods, claims, or restrictions, and eligibility differs entirely from insurance underwriting.

Q: Are there any fees or premiums?

A: No. Policyholders pay no fees, and once settled, they are no longer responsible for premiums.

Q: What happens to ownership?

A: The enrollee transfers ownership and beneficiary rights. The policy is no longer considered an asset for Medicaid eligibility.

Q: How does it impact Medicaid?

A: By obtaining the fair market value for the life policy, and then spending the money to pay for senior living and long-term care services, the LTC-Life Settlement is a regulated financial transaction, and a Medicaid-qualified spend down to help cover the costs of long-term care.

Q: Is this available nationwide?

A: Yes, first introduced into the market in 2007, LTC-Life Settlements are available in all 50 states and enjoy tremendous support from political leaders across the country. Since the settlements pay cash, all forms of senior living and long-term care providers can easily be paid. These settlements have been used to pay millions of dollars in senior care costs.

The Bottom Line

For many seniors, a life settlement can mean the difference between financial stress and financial control during retirement and long-term care.

Before lapsing or surrendering a life insurance policy, explore its fair market value. It may help you or your loved one stay in the care setting of choice and preserve assets for the future.

Learn more and find out what a loved one's life insurance policy can be worth: Life Settlements: A Lifeline for Long-Term Care Funding.

* The author and/or Retirement Genius does not provide tax or legal advice. Nothing herein should be construed as investment, insurance, securities, tax, or legal advice. Consumers should consult with their own tax, legal and/or financial advisors before engaging in any transaction. The information contained herein does not provide any advice as to the value of securities or as to the advisability of investing in, purchasing, or selling securities or insurance products. Decisions based on this information are the sole responsibility of the reader. The information contained herein is not an offer to sell or a solicitation of an offer to buy any security or any investment or insurance product or service.

Chris Orestis, CSA, is President of Retirement Genius and a nationally recognized expert on financial, health, long-term care, and retirement issues. With over 25 years in the insurance and LTC industries, he’s a former Washington, D.C., lobbyist who worked in the White House and for the Senate Majority Leader.