Longer Lives, Rising Costs, and the Growing Need for Long-Term Care Planning. What to Do Now to Avoid Family Crisis

About This Article

Long-term care can cost thousands of dollars each month and quickly drain retirement savings if you are unprepared. Planning now with savings strategies, Long-Term Care Insurance, and family discussions can help protect your independence, preserve assets, and reduce emotional and financial stress on loved ones.

Jacob Thomas

Jacob Thomas writes on health, wellness, and retirement topics, including aging, caregiving, insurance, and long-term care.

Table of Contents

- What Long-Term Care Really Means

- Real Cost of Long-Term Care in 2026

- How Long Will Your Savings Last?

- Why So Many Americans Underestimate the Risk

- 7 Reasons to Start Planning Earlier

- How Long Would Your Retirement Savings Last?

- Building Retirement Savings That Can Support Retirement and Future Care

- Include Long-Term Care in Retirement Planning

- Can Downsizing Help Protect Retirement Savings?

- Role of Long-Term Care Insurance

- Traditional vs. Hybrid Long-Term Care Insurance

- 7 Long-Term Care Planning Mistakes to Avoid

- When Should You Start Planning?

- Build a Plan Before You Need One

You have spent decades building your retirement savings, believing the hardest work is behind you. Then a parent develops dementia, a spouse suffers a stroke, or your own health changes unexpectedly — and suddenly retirement becomes less about freedom and more about figuring out how to pay for extended care.

For millions of Americans, long-term care is the single largest uninsured financial risk of retirement. Yet many families avoid discussing it until a crisis forces difficult decisions.

The best hedge against the rising costs of tomorrow is the clarity of the plan you create today. — Dawid Siuda, finance expert at Omni Calculator.

Planning now for long-term care is not just about money. It ensures you can maintain a good quality of life and reduce stress for your family. A good plan also helps you to prepare for the impacts of unexpected lifestyle changes.

Carolyn McClanahan, a physician and certified financial planner based in Jacksonville, Florida, put it bluntly when interviewed by CNBC. She said that Medicare doesn’t cover “custodial” care, which is when you or a loved one needs help with basic everyday tasks that make up the majority of long-term care needs, according to the HHS-Urban report.

People don't plan for it in advance. It's a huge problem. — Carolyn McClanahan, a member of CNBC’s Financial Advisor Council.

Federal researchers estimate that about 56 percent of Americans turning 65 today will eventually require long-term services and supports that meet the federal definition of long-term care, including assistance with multiple activities of daily living or supervision due to cognitive impairment, according to a 2022 analysis published by the U.S. Department of Health and Human Services Office of the Assistant Secretary for Planning and Evaluation.

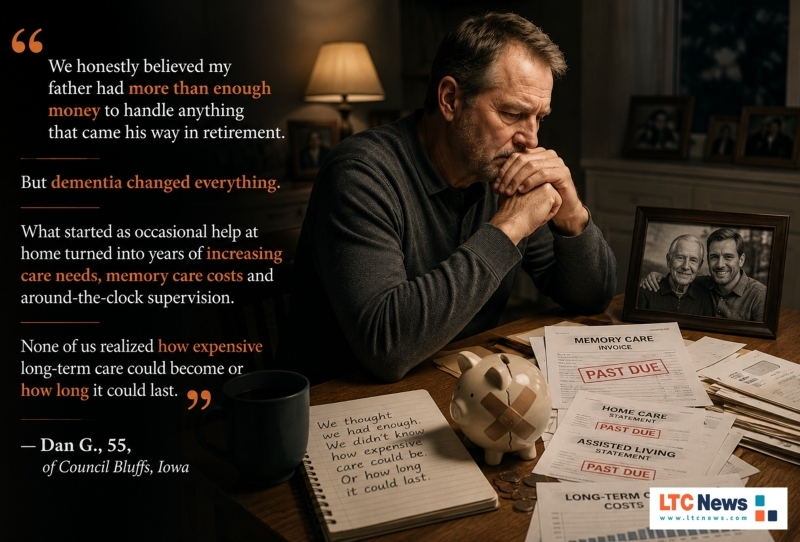

Alzheimer’s disease remains one of the leading drivers of long-term care needs in the United States. More than 7.2 million Americans age 65 and older are living with Alzheimer’s disease, according to the Alzheimer’s Association’s 2026 Alzheimer’s Disease Facts and Figures report published by the Alzheimer’s Association. Dementia-related care is often longer in duration, more emotionally demanding, and substantially more expensive for families.

Caregiving advocates, including Jason Resendez of the National Alliance for Caregiving, have repeatedly warned that families often delay long-term care planning until a crisis limits their options and increases emotional and financial stress.

Nearly half of family caregivers have experienced one negative financial impact because of their caregiving responsibilities, like going into debt or reducing savings or even leaving the workforce due to caregiving. — Jason Resendez, President and CEO of the National Alliance for Caregiving.

The financial consequences can be enormous, but the emotional impact on spouses and adult children is often even greater. The earlier you begin planning, the more choices you keep.

What Long-Term Care Really Means

Many people assume long-term care only refers to nursing homes. In reality, most long-term care is delivered at home or in assisted living. Long-term care includes a wide range of services that help people safely manage chronic illness, disability, injury, frailty, or cognitive decline.

Long-term care may include:

- Assistance with activities of daily living like bathing, dressing, or eating

- Help with transferring, balance, or walking safely

- Medication management

- Dementia supervision

- Home care services

- Adult day care

- Assisted living

- Memory care

- Skilled nursing care

Most care begins gradually. A few hours of help at home can eventually turn into full-time support. Common conditions that trigger long-term care needs include Alzheimer’s disease, Parkinson’s disease, stroke recovery, severe arthritis, diabetes complications, mobility limitations, and frailty associated with aging.

While increased longevity and the consequences of aging are leading factors behind long-term care needs, this is not only an issue for people in their 80s or 90s. Falls and accidents, neurological disorders, and chronic illnesses can create care needs much earlier in life. In other words, with advances in medical science, it can and does happen at all ages. However, the risk increases dramatically as you age.

Real Cost of Long-Term Care in 2026

Many families underestimate how expensive care has become until they begin calling providers. According to the LTC News nationwide survey of long-term care providers, long-term care costs vary significantly by location, labor shortages, level of care, and inflation trends.

In many parts of the country in 2026:

- Home care can exceed $7,000 monthly

- Assisted living frequently ranges from $5,500 to more than $8,000 monthly, plus surcharges

- Memory care often exceeds $9,000 monthly

- Nursing home care in some metropolitan areas can surpass $12,000 monthly

Those numbers reflect today’s pricing. Costs are expected to continue rising due to:

- Caregiver shortages

- Wage inflation

- Increased demand from an aging population

- Higher operational costs

- Regional labor pressures increasing wages

A two- or three-year care event can easily consume hundreds of thousands of dollars from retirement savings. Five years or more can be catastrophic even for a family that is well to do. However, long-term care often starts small, with in-home care several times a week, and expands as the progression of care necessitates more care.

What shocks many families is that base care costs are only part of the equation. Additional expenses often include:

- Medications

- Medical supplies

- Transportation

- Specialized therapies

- Home modifications

- Private caregivers

- Family travel expenses

Use the LTC News Cost of Long-Term Care Services Calculator to compare extended care costs where you live and project future expenses based on inflation trends.

How Long Will Your Savings Last?

One of the most important questions in retirement planning is whether your savings and income will last long enough to support both your lifestyle and any extended care you may eventually need. Unless you have Long-Term Care Insurance or another dedicated funding strategy in place, your retirement income and assets will likely be responsible for paying for future extended care expenses.

The real question becomes: how long would your assets last if you suddenly needed several years of home care, assisted living, or nursing home care?

Share your thoughts and experiences about aging, caregiving, health, retirement, and long-term care with LTC News —Contact LTC News.

For many families, the cost of long-term care will reduce retirement income, force the liquidation of investments, even during unfavorable market conditions, and significantly change a spouse’s lifestyle and financial security. In some situations, extended care costs can drain much of a lifetime of savings far faster than most people ever expected.

To estimate how long your money will last, you can use a retirement withdrawal calculator, which will help you understand how long your assets may last given different variables, such as:

- Withdrawal amount,

- Annual interest rate, and

- Inflation rate.

Many people assume their savings will last longer than they actually do. Running the numbers gives a clearer, more realistic picture of financial security as early as the planning phase.

If you have Long-Term Care Insurance, those numbers will look different since you will have a guaranteed tax-free fund to pay for some or all those expenses. That scenario can also be charted.

Why So Many Americans Underestimate the Risk

Long-term care planning is often delayed because people make assumptions that simply do not reflect reality. One of the biggest misconceptions is the belief that long-term care will never happen to them. Some say they are too healthy, too wealthy, too young, or have no family history of chronic illness. Others assume they will simply “deal with it later.”

In many cases, those beliefs become a form of denial that prevents families from planning before a health crisis limits their options.

Here are several common reasons people fail to plan for long-term care. You may even recognize some of these thoughts in your own planning conversations.

Many People Think Medicare Covers Long-Term Care

It does not. Medicare may pay for short-term skilled nursing or rehabilitation following a qualifying hospital stay, but it does not pay for ongoing custodial care, such as help with bathing, dressing, supervision due to memory loss, or extended assistance at home or in assisted living.

That misunderstanding leaves many families financially exposed and can place a substantial burden on loved ones.

Families Assume Loved Ones Will Provide Care

Family caregivers already shoulder a massive burden in the United States.

According to an LTC News analysis of national caregiving trends and recent industry research, more than 63 million Americans now provide unpaid extended care for aging or disabled loved ones.

Many adult children suddenly become caregivers after a parent’s fall, stroke, or dementia diagnosis. Without legal documents, financial plans, or care instructions already in place, families often face rushed decisions during emotionally overwhelming situations.

Caregiving often affects:

- Careers

- Retirement savings

- Mental health

- Marriages

- Physical health

- Family relationships

Adult children frequently reduce work hours or leave jobs entirely to provide care. Without a plan, the financial damage can spread across generations.

People Believe They Will Stay Healthy

No one expects a stroke, dementia diagnosis, or serious mobility issue. Health changes can happen quickly. Long-term care needs often arrive with little warning. A University of Minnesota School of Public Health study illustrates the problem. The study behind that quote found that 60 percent of middle-aged adults think they are unlikely to need long-term care, while in reality only 30 percent will not need it.

Our study found that middle-aged Americans have unrealistically low expectations about their need for future health care, putting added pressure and strain on family members and friends. —Carrie Henning-Smith, lead author and researcher at the University of Minnesota School of Public Health.

Many Wait Too Long to Plan

Long-Term Care Insurance is medically underwritten. Your health at application largely determines eligibility and pricing. Waiting until after a diagnosis often means:

- Higher premiums

- Reduced benefits

- Policy denial

The healthiest years are usually the best years to plan. In fact, most people obtain Long-Term Care Insurance between the ages of 47 and 67.

7 Reasons to Start Planning Earlier

Planning for long-term care is not about fear. It is about maintaining control.

1. Costs Continue Rising

Long-term care costs have continued rising due to labor shortages, wage pressure, and increased demand from an aging population.

The longer you wait, the more expensive care and insurance become.

2. Americans Are Living Longer

You are likely to live a long life. A longer life expectancy increases the likelihood of eventually needing aging support, aging-in-place assistance, or custodial care services.

3. Family Caregiving Has Real Consequences

A care plan protects not only your income and savings but also your spouse, children, and extended family. You probably don't want to be a burden on your family, who, without a plan, will be responsible for you.

The Caregiving in the U.S. 2025 report found that nearly half of the nation's 63 million family caregivers experienced at least one major financial impact — including taking on debt, stopping saving or being unable to afford food — because of their caregiving responsibilities

Family caregivers are a backbone of our health and long-term care systems, often providing complex care with little or no training, sacrificing their financial future and their own health, and too often doing it alone. — Myechia Minter-Jordan, CEO of AARP.

4. Health Can Change Quickly

Even healthy, active adults can suddenly require extended care after illness or injury.

5. Younger Applicants Usually Receive Better Coverage Options

Applicants in their 40s and 50s generally have:

- Lower premiums

- Better underwriting outcomes

- More inflation protection choices

- Greater policy flexibility

Sure, there are healthy people in their 60s, even into their 70s, but the longer you wait, the greater the chance of having health issues. Inflation protection riders can help policy benefits keep pace with rising future care costs, which is especially important for applicants purchasing coverage years before retirement.

6. Market Volatility Can Hurt Retirement Income

Without a dedicated care plan, families may need to liquidate investments during market downturns to pay for care. That can permanently reduce retirement income. You can't time the markets, nor can you time when you will need care.

7. Planning Reduces Stress During a Crisis

Families with a plan already in place often make better decisions under pressure because options have already been discussed and organized.

How Long Would Your Retirement Savings Last?

One of the most important retirement planning exercises is testing your savings against a real long-term care event.

Ask yourself:

- What happens if care lasts two years?

- What if one spouse needs care while the other remains healthy?

- What if care begins during a market downturn?

- What if dementia care lasts five years or longer?

Many retirees discover their savings could erode far faster than expected.

Factors that affect financial exposure include:

- Retirement savings

- Investment income

- Social Security

- Pension income

- Inflation

- Local care costs

- Length of care

- Home equity

- Existing insurance protection

The LTC News Learning Center offers tools and educational resources to help families better understand potential risks and funding options.

Building Retirement Savings That Can Support Retirement and Future Care

Building retirement savings early is one of the most important steps you can take to maintain financial flexibility later in life. The more time your money has to grow, the greater your ability to handle unexpected expenses, including rising long-term care costs. Even modest savings strategies started early can have a substantial impact over time.

Many people underestimate how quickly healthcare and long-term care expenses can affect retirement income. A stronger financial foundation not only improves lifestyle options in retirement but also provides greater independence and more choices when care becomes necessary later in life.

Here are several strategies that can help strengthen retirement savings and improve long-term financial security:

Start Early

Time matters enormously because compound growth rewards consistency. Money invested in your 30s, 40s, and 50s typically has far greater long-term growth potential than money invested later in life. Starting early also allows smaller contributions to grow over decades, rather than relying on larger catch-up contributions closer to retirement.

Many people delay retirement planning, believing they will save more later when income rises. Unfortunately, unexpected expenses, market downturns, and health changes can interfere with those plans. Starting earlier provides a larger financial cushion and more flexibility over time.

Contribute Consistently

Automatic retirement contributions can help eliminate savings gaps and build disciplined long-term habits. Consistency often matters more than trying to perfectly time markets.

Even during periods of market volatility, continuing regular contributions may allow investors to purchase investments at lower prices over time. Employer-sponsored retirement plans, IRAs, and health savings accounts can all play an important role in long-term financial preparation.

Small increases in monthly contributions can also produce significant long-term growth over decades.

Diversify Investments

Diversification may help reduce exposure to severe market swings during retirement. A balanced investment strategy can help protect retirement income while still allowing for long-term growth potential.

Retirement assets concentrated too heavily in one investment sector, business interest, or asset class may face greater volatility during economic downturns. A diversified approach that considers age, risk tolerance, and income needs can help reduce financial stress later in life.

Avoid Early Withdrawals

Early withdrawals from retirement accounts can trigger taxes, penalties, and the loss of years of compounded growth. Using retirement savings for non-retirement purposes can significantly weaken future financial security.

Many people do not realize that every dollar removed early is not only lost principal but also lost future growth potential. Rebuilding retirement savings later can become much harder as competing expenses increase with age.

Protecting retirement accounts today may provide greater financial independence and more care choices later.

Increase Savings as Income Rises

Lifestyle inflation can quietly erode long-term financial progress. Redirecting raises, bonuses, or additional business income into retirement accounts instead of increasing spending can substantially improve long-term preparedness.

As careers advance and your income rises, many households gradually increase spending on homes, vehicles, travel, and lifestyle upgrades. While enjoying financial success is important, balancing lifestyle improvements with additional retirement savings can significantly strengthen long-term financial stability.

Even modest increases in annual retirement contributions can produce meaningful results over time.

To better understand your future savings potential, a future value calculator can help estimate how much your money may grow over time based on contributions and interest rates.

Include Long-Term Care in Retirement Planning

Many people build retirement plans focused solely on income and investments, while ignoring the potential costs of future extended care needs. Including long-term care expenses in retirement projections provides a more realistic picture of future financial exposure and helps families avoid major surprises later.

A retirement plan that does not account for home care, assisted living, memory care, or nursing home costs may underestimate future financial risk.

You can use a very small portion of investment earnings to pay for your Long-Term Care Insurance, safeguarding the bulk of your retirement account, ensuring access to your choice of quality care, and without burdening those you love.

The earlier these discussions begin, the more choices families usually have regarding care preferences, housing options, and financial strategies.

Can Downsizing Help Protect Retirement Savings?

For many Americans, home equity represents one of their largest assets.

Strategic downsizing may:

- Reduce monthly expenses

- Lower property taxes

- Reduce maintenance costs

- Increase available retirement cash flow

- Provide liquidity for future care needs

Downsizing is not always simple. Housing markets, relocation expenses, emotional attachment to family homes, and accessibility needs can complicate decisions. Some retirees also downsize into homes better suited for aging in place, including those with safer layouts, fewer stairs, and lower maintenance requirements.

For many retirees, simplifying housing expenses creates meaningful financial flexibility and helps support future care needs.

Role of Long-Term Care Insurance

The cost of long-term care is significant and will adversely impact your income and lifestyle. Long-Term Care Insurance is designed specifically to help cover the cost of care services, including:

An LTC policy will help maintain financial independence while providing greater flexibility and care choices. Benefits from qualified Long-Term Care Insurance policies are received tax-free, reducing the emotional and financial pressure on spouses and adult children.

Coverage may also provide access to:

- Better quality home care options

- Money to pay for equipment like ramps, chair lifts, and medical alert systems

- Higher-quality facilities

- Case management/care coordination services

Surveys show that most people prefer receiving care at home for as long as possible. Modern LTC Insurance policies often prioritize home care and aging in place benefits, although the decisions are always left to the policyholder.

In many states, Partnership-qualified Long-Term Care Insurance policies can also help preserve assets through dollar-for-dollar asset protection features.

Traditional vs. Hybrid Long-Term Care Insurance

Today’s market includes traditional Long-Term Care Insurance, hybrid policies linked to life insurance or annuities, and short-term cash indemnity policies. Traditional LTC Insurance focuses primarily on long-term care benefits and is what most consumers choose.

Hybrid policies combine long-term care protection with another financial product, such as:

- Permanent life insurance

- Asset-based policies

- Fixed annuities

Some consumers prefer hybrid products because the benefits may still provide value if long-term care is never needed.

Short-term cash indemnity policies pay the full benefit in cash over a short period of time. Usually, bills do not need to be submitted. The primary benefit of this type of policy is the reduced underwriting requirements, which allow more people to qualify.

An independent LTC Insurance specialist will help compare options from multiple insurers and explain underwriting requirements, inflation protection, elimination periods, benefit structures, and the claims process.

Most people acquire an LTC Insurance policy between the ages of 47 and 67. However, no matter your age or health, seek the advice of an experienced specialist to help you understand your options.

7 Long-Term Care Planning Mistakes to Avoid

1. Waiting Too Long

Health changes can eliminate options quickly, and premiums are based in part on your age and health when you apply.

2. Underestimating Total Costs

Be sure to review the LTC News Cost of Long-Term Care Services Calculator and look at the current and projected future cost of extended care services where you live. Will you relocate? If that is a possibility, also review the cost of long-term care in that location.

3. Ignoring Inflation

Care costs 20 years from now will be much higher than current care service pricing.

4. Thinking You Can Depend on Medicare and Supplements

Medicare and Medicare supplements, like traditional health insurance, cover medical services and skilled care, not long-term custodial care that most people will require. Medicare falls short on long-term care and is not an answer for the extended care that most of us will need.

5. Thinking Medicaid is a Solution

Be cautious of strategies that involve hiding, transferring, or gifting assets solely to qualify for Medicaid long-term care benefits. Improper planning can trigger significant penalty periods under federal Medicaid rules, including provisions established by the Deficit Reduction Act. Proper long-term care planning helps preserve assets legally while maintaining access to quality care and greater financial stability. Medicaid is never a goal or a solution for long-term care; it is a safety net for those with very limited financial resources, not a comprehensive retirement strategy.

6. Avoiding Family Discussions

Whether you have Long-Term Care Insurance or not, and whether you have significant assets to protect or not, having honest conversations about aging is essential. Your loved ones should understand your wishes, care preferences, and financial plans before a health crisis forces difficult decisions under pressure.

7. Assuming You Can “Figure It Out Later”

Care decisions become harder under stress and limited timelines. Waiting until later to figure out how to address long-term care will create a family crisis. The earlier you have an honest conversation, the more control you maintain over where you receive care, how it is funded, how family will be involved, and how much financial and emotional strain your family may avoid later.

When Should You Start Planning?

Every decade matters. While there are people who obtain long-term care coverage in their 20s and 30s, most start thinking about it after age 40.

In Your 40s

Begin discussing retirement exposure, caregiving risks, and long-term planning goals. If you are financially secure or own a business, purchasing a Long-Term Care Insurance policy in your 40s can be a smart strategy. Some policies can be paid up within 10 years, meaning premiums may be eliminated before retirement begins. In many cases, self-employed individuals and business owners may also be able to deduct some or all of the premium as a business expense, depending on tax status and policy design.

If your parents are still living and have not planned for long-term care, this is the time to begin that conversation. Discussing aging, caregiving wishes, finances, and care preferences before a crisis occurs can help avoid confusion, family conflict, and rushed decisions later.

In Your 50s

Your 50s are when most people begin exploring and purchasing Long-Term Care Insurance, while premiums and underwriting remain more favorable. Your 50s are also when many people start experiencing the early signs of aging and health changes, which is why the decade is sometimes referred to as the “fragile 50s.” Waiting too long can limit coverage options, increase premiums, or lead to underwriting declines after medical conditions develop.

In Your Early 60s

Many healthy applicants still qualify for Long-Term Care Insurance in their early 60s, although pricing typically rises with age. Do not assume premiums are automatically out of reach or that pre-existing health conditions mean coverage is impossible to obtain. Underwriting guidelines vary significantly between insurers, and some companies are more flexible with certain medical conditions than others. That is why it is essential to work with an independent LTC Insurance specialist who represents all major companies and understands how each insurer evaluates health history, medications, family history, and risk factors.

Late 60s and Beyond

Coverage options often narrow significantly in your late 60s and beyond as medical conditions, prescription drug use, and mobility issues become more common. Premiums are typically higher at older ages, and underwriting becomes more challenging with every additional health concern. Still, you probably can find affordable options.

Do not assume all options disappear because of age or pre-existing health conditions. Some products, including certain hybrid Long-Term Care Insurance policies and short-term cash indemnity plans, may offer simplified or reduced underwriting requirements compared with traditional LTC Insurance. These policies can still provide meaningful benefits that help offset home care, assisted living, or other extended care expenses.

Even if traditional Long-Term Care Insurance is no longer available or affordable, this remains a critical time to put a long-term care strategy in place. Families should discuss caregiving expectations, legal documents, housing plans, asset protection strategies, and how future care costs may affect retirement income and loved ones. Waiting until a health crisis occurs can leave families with fewer choices and far greater emotional and financial stress.

Build a Plan Before You Need One

The families who navigate long-term care most successfully are not always the wealthiest. They are usually the most prepared. Being prepared is essential.

They discussed their aging options early. They realistically reviewed the potential costs and their impact on their families. They explored insurance, savings strategies, legal planning, and family expectations before a health crisis forced them to make rushed decisions.

Planning now may not prevent aging, illness, or unexpected health changes. But it can help preserve your dignity, maintain independence, and reduce avoidable financial and emotional hardship for the people you love most.

The best time to plan is before a health emergency removes choices. In life, most people prefer choice.

Frequently Asked Questions

Does Medicare pay for long-term care?

No. Medicare generally does not pay for ongoing custodial long-term care, which is the type of care most people eventually require as they age.

Medicare may pay for short-term skilled nursing or rehabilitation following a qualifying hospital stay, but it typically does not cover extended assistance with daily living activities, dementia supervision or long-term home care.

What is the difference between traditional and hybrid Long-Term Care Insurance?

Traditional Long-Term Care Insurance focuses primarily on paying for extended care services such as home care, assisted living and nursing home care.

Hybrid policies combine long-term care benefits with life insurance or annuity products. Some consumers prefer hybrid products because benefits may still provide value even if long-term care is never needed.

Can long-term care drain retirement savings?

Yes. Extended care costs can quickly reduce retirement income, force the liquidation of investments and significantly affect a spouse’s financial security.

Without a dedicated funding strategy such as Long-Term Care Insurance, many families rely heavily on personal savings and unpaid caregiving support from loved ones.

Why is dementia such a major long-term care issue?

Dementia-related care is often more expensive because care may continue for many years and frequently requires around-the-clock supervision.

According to the Alzheimer’s Association’s 2025 Alzheimer’s Disease Facts and Figures report, more than 7.2 million Americans age 65 and older are living with Alzheimer’s disease. Dementia is one of the leading reasons families require home care, memory care or nursing home services.

What is the biggest mistake families make with long-term care planning?

One of the biggest mistakes is waiting too long to plan. Many families assume they will “figure it out later,” only to face rushed decisions after a stroke, dementia diagnosis or serious health event.

Delaying planning can reduce insurance options, increase financial stress and place major caregiving burdens on spouses and adult children.

How much does long-term care cost in 2026?

Long-term care costs vary widely depending on location and level of care. According to LTC News surveys of long-term care providers:

- Home care can exceed $7,000 monthly

- Assisted living often ranges from $5,500 to more than $8,000 monthly

- Memory care frequently exceeds $9,000 monthly

- Nursing home care in some metro areas can surpass $12,000 monthly

Costs are expected to continue rising because of caregiver shortages, inflation and increased demand from an aging population.

What is long-term care?

Long-term care includes a wide range of services designed to help people manage chronic illness, disability, cognitive decline or frailty associated with aging. Care may involve assistance with bathing, dressing, mobility, eating, medication management or supervision due to dementia or memory loss.

Long-term care is often provided at home, in assisted living, memory care communities or nursing homes depending on a person’s needs.

For more information, you can read our FAQ article about what long-term care is and what it covers.

Can you still qualify for Long-Term Care Insurance with health problems?

Possibly. Underwriting guidelines vary significantly between insurance companies. Some insurers are more flexible with certain medical conditions, medications or health histories than others.

In addition, some hybrid Long-Term Care Insurance products and short-term cash indemnity policies may offer simplified underwriting requirements compared with traditional LTC Insurance.

When is the best time to buy Long-Term Care Insurance?

Most people begin exploring Long-Term Care Insurance in their 40s or 50s while health and underwriting conditions are generally more favorable.

Applying earlier often means:

- Lower premiums

- More policy choices

- Better underwriting outcomes

- Greater inflation protection options

Waiting until health conditions develop can limit eligibility or make coverage significantly more expensive.

Why should families discuss long-term care before a crisis occurs?

Discussing aging, caregiving wishes and financial plans before a health emergency helps families avoid confusion, conflict and rushed decisions later.

Planning ahead gives families more control over:

- Care preferences

- Housing choices

- Financial strategies

- Legal planning

- Family caregiving expectations

The earlier these conversations begin, the more choices families usually keep.