Why Families Face Legal Disputes When Planning Long-Term Care

About This Article

Family disputes during long-term care planning often arise over finances, property, medical decisions, and legal authority. Without clear documentation, such as powers of attorney and estate plans, misunderstandings can escalate into legal conflicts.

Anna Marino

Anna Marino is a seasoned writer specializing in topics related to family, aging, and lifestyle in retirement. She shares advice on intergenerational relationships and strategies for enjoying retirement.

Table of Contents

- Differing Views on Care Often Trigger Disputes

- Financial Pressure Is Often the Breaking Point

- Property and Inheritance Disputes Add Another Layer

- Communication Breakdowns Often Make Conflict Worse

- Legal Planning Can Prevent Many Disputes

- When Families Turn to Attorneys

- Tools That Help You Plan Before Conflict Begins

- Best Time to Prevent Conflict Is Now

Planning long-term care for aging parents can quickly lead to family conflict, especially when finances, property, and decision-making authority are involved. The consequences of aging have become a growing source of family conflict in the United States, Canada, and worldwide.

You might not expect planning for a parent’s care to divide your family. But across the country, attorneys and care professionals say it happens more often than people realize. The crisis is even more complicated as many families have never even discussed long-term care and other age-related issues, much less do anything about it, despite the aging of America and the Long-Term Care Insurance claims now expected to reach $44 billion in the coming years.

Americans are often unprepared for long-term care decisions.

Americans in general aren’t planning in this way, and much of the responsibility for providing and paying for long-term care is falling on their children.” — AARP report.

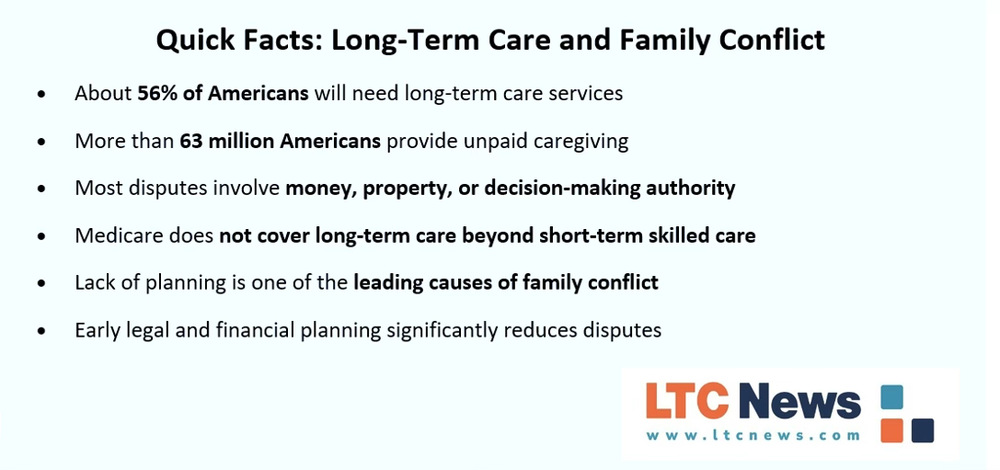

As Americans live longer and require more help with daily activities, families are being forced to make complex decisions—often quickly and under stress. According to federal data, about 56% of Americans will need long-term care services, while more than 63 million Americans are already providing unpaid care to loved ones.

That combination—longer lives, rising care needs, and financial pressure—is creating a perfect storm for disagreement. What starts as a conversation about care can quickly turn into conflict about money, control, and responsibility.

As parents age, family dynamics can shift, sometimes leading to conflict.

Adult children may disagree about financial responsibilities, living arrangements, medical decisions, or who should have legal authority through powers of attorney or guardianship.

These situations can quickly become emotional because they involve deeply personal relationships, long-standing family roles, and concerns about a loved one’s safety and independence. Lawrence S. Viola, a San Mateo, California litigation lawyer, says that when disagreements escalate or involve property, caregiving obligations, or the management of assets, families often turn to attorneys for guidance.

Families often seek an experienced elder law or estate attorney who can help clarify legal rights, mediate disputes, and ensure decisions about care, finances, and authority follow the law while protecting the older adult’s best interests.

“Family conflicts over aging parents are more common than people realize. When disagreements involve finances, property, or medical decision-making, the legal issues can quickly become complicated. An attorney often steps in not only to interpret the law but to help families create clear legal authority, resolve disputes, and establish a plan that protects the older adult while preserving family relationships whenever possible.” — Lawrence S. Viola, Attorney, Viola Law Firm P.C.

Differing Views on Care Often Trigger Disputes

One of the first and most emotional points of conflict is deciding what kind of care is best. In many families, there is no clear agreement. One sibling may see professional care as the safest option. Another may believe staying at home preserves dignity and independence.

These disagreements are rarely just about logistics. They reflect deeper concerns about:

- Safety and medical needs

- Emotional well-being

- Financial sustainability

- Respecting a parent’s wishes

Without written guidance or prior discussion, families are often left to interpret what a parent “would have wanted.” That uncertainty can quickly escalate into arguments, especially when health declines, and decisions become urgent.

Financial Pressure Is Often the Breaking Point

While emotions may start the conflict, money often intensifies it.

Long-term care costs can quickly reach thousands of dollars per month, depending on the level of care and location. Many families are unprepared for these expenses and are surprised to learn that Medicare and traditional health insurance only cover short-term skilled care, not ongoing assistance.

That leaves families to make difficult financial decisions, including:

- Using savings or retirement funds

- Selling a home or other assets

- Dividing costs among siblings

- Managing accounts through a power of attorney

Tensions often rise when one person controls the finances, especially if other family members feel excluded or uninformed. Even when everyone has good intentions, a lack of transparency can lead to suspicion—and, in some cases, legal challenges.

Long-Term Care Insurance, when in place, can help reduce these pressures by providing tax-free benefits for care in any setting. Without it, families are more likely to face both financial strain and conflict.

Property and Inheritance Disputes Add Another Layer

For many families, the largest asset involved in care planning is the family home. Deciding what to do with that property can be deeply divisive.

Some family members may want to preserve it for inheritance. Others may see it as necessary to sell in order to fund care. These disagreements often go beyond finances; they are tied to memories, expectations, and perceptions of fairness.

Without a clear estate plan, these situations can lead to:

- Accusations of favoritism

- Disputes over asset control

- Legal intervention

And once legal action begins, relationships can be permanently damaged.

Communication Breakdowns Often Make Conflict Worse

In many cases, disputes are not caused by bad intentions—but by a lack of communication. Families often avoid difficult conversations about:

- Aging and declining health

- Financial limitations

- End-of-life preferences

When those conversations don’t happen early, decisions are made in moments of crisis—when emotions are high and time is limited.

You may see:

- One person taking control without full agreement

- Others feeling excluded or unheard

- Assumptions replacing clear decisions

Once trust breaks down, even small disagreements can escalate quickly.

Legal Planning Can Prevent Many Disputes

The most effective way to reduce conflict is to plan before it’s needed. Legal documents provide clarity and structure at a time when families need it most.

Key tools include:

- Power of attorney (financial and healthcare)

- Living wills or advance directives

- Comprehensive estate plans

These documents clearly define:

- Who makes decisions

- How finances are handled

- What care preferences should be followed

When prepared early and shared openly, they remove uncertainty—and significantly reduce the risk of disputes.

When Families Turn to Attorneys

Despite careful planning, some disagreements cannot be resolved privately. In those cases, families often seek legal guidance to:

- Clarify rights and responsibilities

- Mediate disputes

- Ensure compliance with state laws

- Resolve conflicts through negotiation or court action

While litigation is usually a last resort, it can provide structure when communication breaks down, and decisions must be made.

Tools That Help You Plan Before Conflict Begins

You don’t have to navigate this alone. Ideally, planning for aging, retirement, and future long-term care happens before you retire. Experts say you start by talking about it, something many of us refuse to do.

“Ideally, planning for aging, retirement, and long-term care starts long before retirement—but too often, families avoid the conversation until a crisis forces it. That delay can limit choices and increase conflict.”

You can:

- Use the LTC News Cost of Care Calculator to understand real costs where you or a loved one lives

- Explore the LTC News Caregiver Directory to find in-home caregivers and long-term care facilities, like assisted living. This is helpful for family members to start finding help for their older loved one

- Learn about planning strategies through the LTC News Long-Term Care Insurance Learning Center

- If a loved one has a Long-Term Care policy, be sure to tell the attorney and use the benefits right away. Get free expert help to file the claim, at no cost or obligation. LTC News partners with Amada Senior Care to get this professional assistance — File a Long-Term Care Insurance Claim.

Having accurate information early can help you make informed decisions before emotions take over.

Best Time to Prevent Conflict Is Now

You may believe your family will come together when it matters most. Many families do, but many also struggle when decisions are rushed and unclear. If your family had to make these decisions tomorrow, would everyone agree—or would conflict slow down the care your parent needs?

Planning now is not just about finances or legal documents. It is about preserving relationships, protecting dignity, and ensuring your loved one receives the right care at the right time. Because when you plan early, you don’t just avoid disputes, you create peace of mind for everyone involved.

Frequently Asked Questions

Can siblings be forced to pay for a parent’s care?

In most states, adult children are not legally required to pay. However, expectations, family dynamics, and emotional pressure often lead to disagreements about financial contributions.

How can families avoid conflict when planning care?

You can reduce conflict by:

- Starting conversations early

- Involving all key family members

- Documenting wishes clearly

- Seeking legal and financial guidance

What causes family disputes when planning long-term care?

Family disputes often arise due to disagreements over finances, property, medical decisions, and who has legal authority. Without clear documentation, such as powers of attorney or estate plans, misunderstandings can quickly escalate into conflict.

What legal documents help prevent family disputes?

Key documents include:

- Power of attorney (financial and healthcare)

- Living will or advance directive

- Estate plan

These documents clearly define who makes decisions and how finances are managed, reducing confusion and conflict.

How can Long-Term Care Insurance reduce family conflict?

Long-Term Care Insurance provides tax-free benefits to help cover care costs. This reduces financial pressure on family members, limits disagreements over money, and allows care decisions to focus on quality and preferences rather than cost alone.

What happens if there is no long-term care plan?

Without a plan, families often make decisions during a crisis. This can lead to:

- Delays in care

- Family disagreements

- Court involvement (guardianship)

- Increased financial stress

Does Medicare pay for long-term care?

No. Medicare and traditional health insurance typically only cover short-term skilled care (up to 100 days) and do not pay for ongoing long-term care such as extended in-home care, assisted living, or custodial care.

When should families start planning for long-term care?

Ideally, planning should begin before retirement, while your loved one is still healthy and able to communicate their wishes clearly. Early planning allows more options, reduces stress, and helps prevent disagreements during a crisis.

Sponsored