Long-Term Care Insurance Claims to Hit $44 Billion—A Warning Sign for Every Aging American

About This Article

Long-Term Care Insurance claims are expected to reach $44 billion annually by 2041, reflecting a sharp increase in the number of older Americans needing help with daily activities. This surge is driven by aging baby boomers, longer life expectancy, and higher rates of chronic illness.

James Kelly

LTC News staff writer specializing in long-term care and aging.

Table of Contents

- The Claims Surge: What the Data Shows

- The Bigger Story: Insurance Data Mirrors a National Aging Trend

- The Demographic Forces Driving Demand

- Why LTC Insurance Claims Are Rising Now—And Why They Will Keep Climbing

- The Care Gap: Most Americans Will Need Help—Few Have a Plan

- The Disconnect is Clear:

- Medicare Won’t Cover What You Think

- A System Already Under Pressure

- The Financial Reality: Costs Continue to Rise

- What This Means for You and Your Family

- The Aging Trend is in Motion

- Take the Next Step

A quiet shift is underway. Across the country, more Americans are reaching the point where everyday tasks like getting dressed, preparing meals, and moving safely around their home or about town start to require help. It rarely happens all at once. It builds over time, often unnoticed, until support becomes necessary.

New data now shows how large that shift is becoming.

You may not think about long-term care today, but the need is rising fast across the country. New projections show a surge in claims that reflects a much larger challenge facing millions of American families.

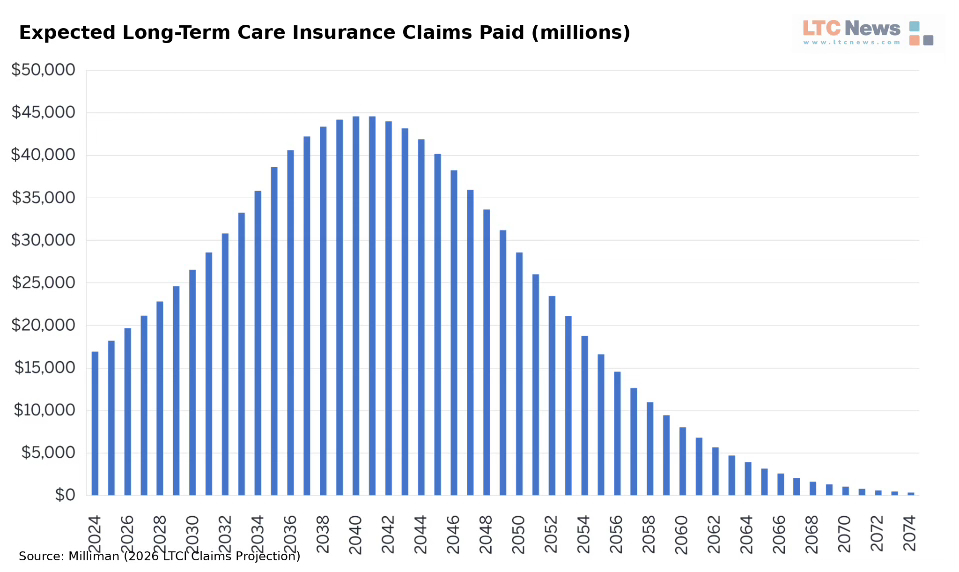

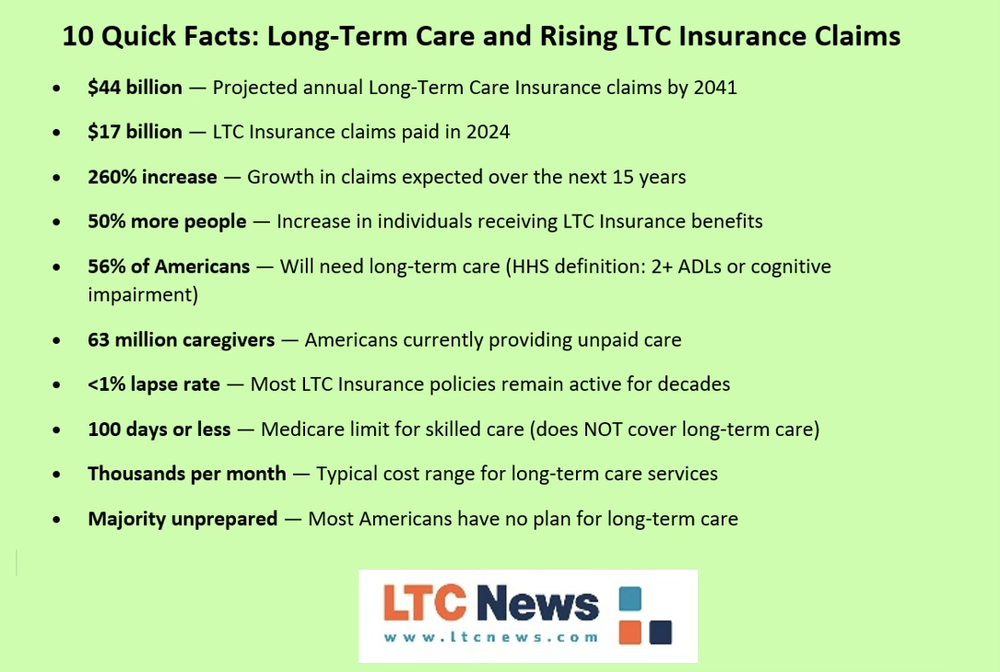

A 2026 report from Milliman (Milliman is a global actuarial and consulting firm that provides data-driven analysis and risk management expertise to insurers, governments, and financial institutions, including research on long-term care trends and insurance projections) projects Long-Term Care Insurance claims will climb from about $17 billion in 2024 to $44 billion annually by 2041—a 260% increase in 15 years.

As more older Americans require assistance, it becomes increasingly urgent to address the cost of caregiving,” according to researchers at American University, reflecting a broader reality that millions of Americans are now entering the stage of life where long-term care becomes necessary.

Millions of Americans are now entering the stage of life where long-term care becomes a reality, and the impact on American families like yours is a real concern.

The United States is on the brink of an age wave of unprecedented proportions.” — Ken Dychtwald, founder and CEO of Age Wave.

Today, the United States ranks 68th globally in healthspan, according to the Institute for Health Metrics and Evaluation. Healthspan refers to the number of years a person lives in good health, maintaining independence and the ability to perform daily activities.

But with data showing that 79 percent of adults age 60 and older live with two or more chronic conditions, such as diabetes, heart disease, and high blood pressure, and more than half of younger adults already reporting at least one chronic illness, health experts are shifting their focus.

The question is no longer just how long you live. It’s how long you can live well—free from disease, disability, and loss of independence. That’s what experts call your healthspan.

Healthspan means living better, not just longer. We're talking about those years that are free from any significant chronic disease or any significant disability that might affect one's quality of life.” — Dr. Corey Rovzar, a postdoctoral fellow at the Stanford Prevention Research Center within the university's School of Medicine in California.

These numbers are striking. The meaning behind it matters more. This is not just an insurance story, even though it shows that Long-Term Care Insurance works. It reflects millions of Americans entering the stage of life when long-term care becomes a reality.

The Claims Surge: What the Data Shows

The shift is already visible in today’s numbers. According to the National Association of Insurance Commissioners:

- LTC Insurance claims reached approximately $17 billion in 2024

- Claims are projected to peak at $44 billion by 2041

- The number of people receiving benefits will increase by about 50%

Additional insights from the Milliman analysis:

- Projections exclude future policy sales, meaning totals will be higher

- Elevated claim levels are expected to persist for decades

The increase reflects a long-term demographic shift, not a temporary spike.

The Bigger Story: Insurance Data Mirrors a National Aging Trend

Focusing only on insurance misses the broader reality. Most Americans do not have Long-Term Care Insurance. However, marketers tell LTC News that the overall number of people expressing interest is increasing. Yet the need for extended care is rising across the entire population, and too many people tend to ignore the problem until a family crisis hits them.

The Demographic Forces Driving Demand

- The population age 65 and older continues to grow rapidly

- Millions of baby boomers are entering their 80s, when care needs rise sharply

- Longer life expectancy increases the likelihood of needing extended support

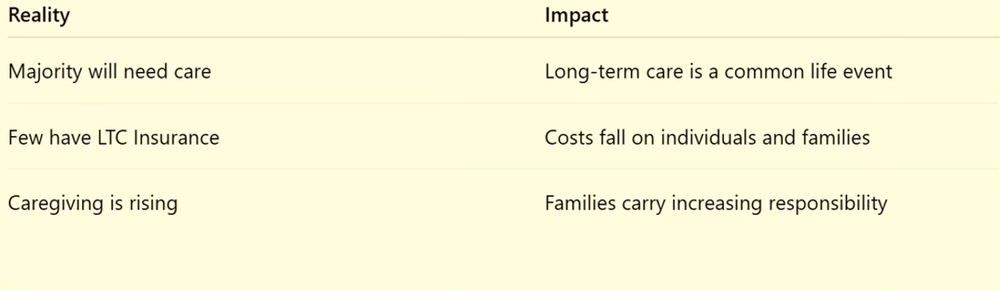

The U.S. Department of Health and Human Services estimates that 56 percent of Americans will require long-term services and supports—defined as needing help with at least two activities of daily living or cognitive impairment.

Key takeaway: The surge in LTC Insurance claims reflects only part of a much larger increase in care needs nationwide.

Why LTC Insurance Claims Are Rising Now—And Why They Will Keep Climbing

The timing of this surge is not accidental. During peak sales years in the late 1990s and early 2000s:

- Millions of Americans purchased LTC Insurance

- Policies were structured for use decades later

- Very low lapse rates meant most policies remained active

Now those policyholders are reaching advanced age. A person who purchased coverage at age 60 in 2002 is now in their early 80s—precisely when long-term care needs typically emerge.

👉 The broader implication: The same aging pattern applies to the general population, not just those with insurance.

The Care Gap: Most Americans Will Need Help—Few Have a Plan

This is where the data becomes personal. Most Americans will need long-term care at some point. Most are not financially prepared. Nor are families even discussing the issue.

At the same time:

- 63 million Americans are providing unpaid care, creating a family crisis

- Family caregivers often step in without preparation or resources

- Many caregivers face financial strain, lost income, and long-term stress

The Disconnect is Clear:

Experts say that long-term care is one of the most overlooked financial risks because it develops gradually and often goes unplanned until a crisis occurs.

“The key to long-term care planning is doing it early before there’s a crisis, because when that happens, you’re trying to make decisions about care under pressure.” — Experts at the University of Washington Medicine.

Medicare Won’t Cover What You Think

A common misconception continues to create risk with too many families assuming their health insurance or Medicare over long-term care services. They never did.

👉 Medicare Falls Short on Long-Term Care: Families Face Financial Strain

Medicare and traditional health insurance:

- Cover short-term skilled care only

- Limit benefits to up to 100 days following a qualifying hospital stay

- Do not cover ongoing custodial care, such as help with daily activities or dementia supervision

👉 What this means: Without preparation, long-term care costs are paid out-of-pocket, or loved ones will provide extended care until assets are depleted or Medicaid eligibility is reached.

A System Already Under Pressure

The growing demand for care is colliding with existing challenges:

- Workforce shortages

- Rising labor costs

- Uneven access to services depending on location

As demand increases, access to quality care may become more limited—especially during urgent situations.

The Financial Reality: Costs Continue to Rise

Long-term care remains expensive and continues to increase in cost. Prices vary by location and type of care, but they can quickly reach thousands of dollars per month.

You can explore real-time costs where you or a loved one lives by using the LTC News Cost of Care Calculator, the most updated and comprehensive survey of long-term care costs in the United States.

👉 LTC News Cost of Care Calculator

You can also find quality long-term care providers, including home caregivers, adult day care centers, assisted living, memory care, rehab centers, and nursing homes, by searching through the LTC News Caregiver Directory, the largest free database of caregivers and facilities in the United States.

👉 LTC News Caregiver Directory

If a loved one has Long-Term Care Insurance, be sure to use the policy benefits without delay. The sooner a loved one receives quality care, the better their quality of life, and the sooner they receive care, the sooner the family burden is eased, and income and assets are protected.

Need help filing a claim? LTC News partners with Amada Senior Care to offer free, no-obligation claim support. Their trained specialists guide you through the process step by step, helping you access your Long-Term Care Insurance benefits quickly and correctly — File a Long-Term Care Insurance Claim.

Share your insights and personal experiences on aging, caregiving, health, retirement, and long-term care with LTC News. Your story can help others navigate similar challenges —Contact LTC News.

What This Means for You and Your Family

The projected rise in claims reflects a broader shift that will affect millions of families.

Common outcomes include:

- Sudden care needs

- Financial pressure

- Emotional strain on loved ones

Planning now changes those outcomes. It allows you to:

- Protect your income and assets

- Maintain independence

- Choose care options on your terms

- Reduce the burden on your family

The Aging Trend is in Motion

The projected increase to $44 billion in Long-Term Care Insurance claims is not just an industry milestone. It is a signal. More Americans are entering the stage of life where long-term care becomes necessary—and the gap between need and preparation remains wide.

You may not need extended care today. But the trend is already in motion. Will you have a plan in place—or will decisions be made under pressure later?

Take the Next Step

- Review care costs using the LTC News Cost of Care Calculator

- Explore providers through the LTC News Caregiver Directory

- Learn about planning options in the LTC News Long-Term Care Insurance Learning Center

- Seek help from a qualified LTC Insurance specialist to get free and accurate quotes from all the top insurance companies offering long-term care insurance solutions.

Are you prepared for the consequences of aging and long-term care? Aging and changing health are realities, and planning will ease the burdens that would otherwise be placed on those you love.

Frequently Asked Questions

Why do experts say long-term care is often overlooked?

Long-term care needs usually develop gradually, not suddenly. Many families delay planning because the need feels distant. As a result, decisions are often made during a crisis, when options are limited and costs are higher.

What happens if you need long-term care without insurance?

Without Long-Term Care Insurance, most people pay out-of-pocket until their assets are depleted. At that point, they may qualify for Medicaid. In many cases, family members step in to provide unpaid care, which can create financial and emotional strain.

What is driving the increase in Long-Term Care Insurance claims?

The rise in claims is largely driven by aging demographics. Millions of Americans who purchased Long-Term Care Insurance 20 to 30 years ago are now reaching their 80s, when care needs typically increase. Longer life expectancy and higher rates of chronic illness are also contributing to the growing demand for long-term care services.

How can you prepare for future long-term care needs?

You can take several steps now:

- Learn about costs using the LTC News Cost of Care Calculator

- Explore care options through the LTC News Caregiver Directory

- Discuss a plan with your family

- Consider Long-Term Care Insurance while you are still healthy

How many Americans actually have Long-Term Care Insurance?

Only a small percentage of Americans have Long-Term Care Insurance. While millions of policies are in force, the majority of older adults do not have coverage, which means most families rely on personal savings or unpaid caregiving when care is needed.

What types of care does Long-Term Care Insurance cover?

Most modern LTC Insurance policies cover a range of services, including:

- In-home care

- Assisted living

- Memory care

- Nursing home care

- Adult day care services

Benefits are typically paid tax-free and can be used in the setting you choose.

How much does long-term care cost?

Costs vary depending on location and type of care, but services can range from several thousand to over $10,000 per month. You can find current, location-based costs using the LTC News Cost of Care Calculator.

Will Medicare pay for long-term care services?

No. Medicare and most health insurance plans only cover short-term skilled care, typically up to 100 days after a hospital stay. They do not cover ongoing custodial care, such as help with bathing, dressing, or supervision due to dementia.

What is the biggest takeaway from rising LTC Insurance claims?

The surge in claims is not just about insurance—it is a clear signal that more Americans will need long-term care. Planning ahead gives you control, protects your finances, and reduces the burden on your loved ones.

When should you start planning for long-term care?

Planning is most effective when done before retirement or in your 40s or 50s. Most people acquire an LTC policy between the ages of 47 to 67. Waiting until health issues arise can limit your options and increase costs.

Does the increase in LTC Insurance claims mean more people need care?

Yes. The increase in claims reflects a broader trend—more Americans are entering the stage of life where help with daily activities becomes necessary. The U.S. Department of Health and Human Services estimates that about 56% of Americans will need long-term care services at some point.