Scams Targeting Older Adults Are Surging: How to Protect Your Aging Parents

About This Article

Identity theft targeting older adults is on the rise. Learn how to protect your aging parents, spot scams early, and safeguard finances and independence.

Mallory Knee

Mallory Knee is a freelance writer for multiple online publications where she can showcase her affinity for all things beauty and fashion.

Table of Contents

- Scope of the Problem Is Growing

- Why Older Adults Are Prime Targets

- Strengthen Passwords and Digital Security

- Protect Paper Records and Mail

- Secure All Paper Records

- Paper Records You Should Keep—and How to Secure Them

- Watch for Red Flags of Fraud

- Talk About It Without Shame

- Monitor Accounts and Create a Simple System

- Why Older Adults in Extended Care Settings Face Even Greater Risk

- How To Protect Your Parent in a Facility or With In-Home Care

- Take Action Now—Small Steps Matter

- Frequently Asked Questions About Protecting Older Adults From Scams and Financial Fraud

You get a call from your mother. Her voice is shaky. She tells you someone from the bank called. They said there was suspicious activity on her account and she needed to “verify” her information immediately. She gave them what they asked for. Now she’s not sure what just happened.

You pause. Your instincts kick in.

This wasn’t the bank.

It’s happening every day, often to people who have done everything right their entire lives. Today’s scams don’t just target technology. They target trust, fear, and urgency. And when your older parent becomes a victim, the consequences can ripple through every part of their life—from finances to independence.

The Federal Trade Commission warns that many scams “pretend to be from trusted sources and use fear to get people to act quickly.” The U.S. Department of Justice reports that older adults lose billions of dollars every year to elder fraud schemes.

Scammers are increasingly using AI to mimic voices of family members, making fraud more convincing and harder to detect. Here’s what you need to know—and how to step in before damage is done.

Scope of the Problem Is Growing

You are not imagining the risk. It is increasing and accelerating as criminals refine their tactics. According to the Federal Trade Commission, Americans reported losing more than $10 billion to fraud in 2023. That number climbed to about $12.5 billion in 2024—and may be even higher in 2025 as scams become more sophisticated.

The FBI Internet Crime Complaint Center continues to report that older adults experience some of the highest per-person losses. In fact, adults age 60 and older reported about $2.4 billion in fraud losses in 2024, nearly four times higher than just four years earlier.

Even more concerning, high-dollar losses are rising sharply, with a growing number of older victims losing $100,000 or more in a single scam. And because many cases go unreported, experts say the true financial impact is likely far greater.

Recent AARP reporting indicates that fraud schemes targeting older adults are becoming more sophisticated, often using impersonation and digital tools to gain trust.

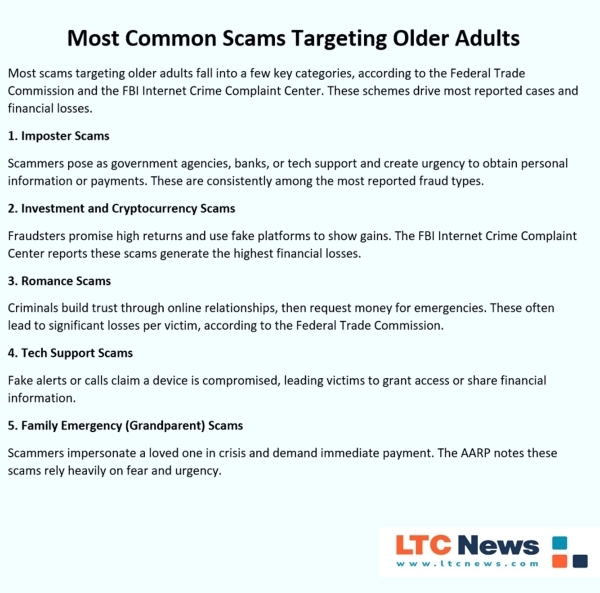

Impostor scams, tech support fraud, and romance scams remain among the most common threats. This is not just an inconvenience. It is financial disruption that can derail retirement plans and long-term stability.

Why Older Adults Are Prime Targets

Understanding why scammers target older adults helps you anticipate and prevent attacks more effectively. Aging adults often present several risk factors that criminals actively exploit:

- Larger savings or home equity

- Frequent medical and insurance transactions

- Increased reliance on others for assistance

- Less familiarity with evolving technology

When fraud occurs, recovery is often difficult. Lost assets can directly impact the quality of life and long-term independence.

Strengthen Passwords and Digital Security

Many fraud cases begin with a single compromised login. Once access is gained, scammers can move quickly across accounts. That’s why strengthening digital security is one of the most effective first steps you can take.

- Use unique passwords for each account

- Avoid personal details like birthdays or names

- Enable multi-factor authentication (MFA)

- Remove unused or old devices

- Keep software updated

A password manager can simplify this process and reduce confusion for your parent. A clean, organized digital setup reduces the number of entry points for criminals.

When helping your parent update logins, generate truly random, unique passwords for each account with a secure password generator, then store them in a password manager. Aim for 16+ characters using letters, numbers, and symbols, and replace any reused or weak passwords first.

Protect Paper Records and Mail

Even in a digital world, physical documents remain one of the easiest ways for criminals to steal sensitive information. Years of saved paperwork, bank statements, insurance forms, medical records can expose everything a scammer needs.

To reduce that risk:

- Review mail daily

- Store sensitive documents in a locked location

- Switch to paperless billing when possible

- Shred documents containing: Social Security numbers, Account numbers, Insurance details, or Medical records.

A simple cleanup of old files can significantly reduce exposure.

Secure All Paper Records

Fraud isn’t isolated to online accounts. Physical documents pose serious risks to families, especially in homes with years of stored bank statements and medical records. Sort mail soon after it arrives, place sensitive papers in a locked drawer, and switch to digital delivery for records.

Figure out which documents you can discard after sorting the mail. Then, choose a paper shredder to safeguard your parents’ information. If there is a lot of paperwork to shred, get one that can shred multiple pages at once. Review the number of sheets you can shred at one time. People tend to keep a lot of paper documents, and over a long lifetime, it can add up. Otherwise, take the documents to a commercial shredder.

Paper Records You Should Keep—and How to Secure Them

Even in a digital world, paper documents remain a major source of identity theft if they’re lost, stolen, or improperly discarded. Start by knowing what to keep—and how to protect it.

Essential Documents to Keep:

Identity and legal

- Birth certificate

- Social Security card

- Passport

- Driver’s license (copy)

- Marriage, divorce, or adoption records

Financial

- Bank and credit card statements (recent 12–24 months)

- Tax returns (at least 3–7 years)

- Pension and retirement account statements

- Property deeds, titles, and mortgage documents

Insurance

- Health, Medicare, and Long-Term Care Insurance policies

- Life, home, and auto insurance policies

Medical

- Advance directives (living will, DNR)

- Health care proxy or power of attorney

- Medication lists and key medical records

Estate and legal planning

- Will and trust documents

- Durable power of attorney

- Beneficiary designations

Protecting these documents is just as important as keeping them.

- Store originals in a locked, fireproof safe at home

- Keep backup copies in a safe deposit box or with a trusted attorney

- Limit who has access—share only with trusted family members

- Avoid carrying sensitive documents unless absolutely necessary

- Create a simple document inventory list for easy tracking

Watch for Red Flags of Fraud

Fraud rarely appears out of nowhere. In many cases, elder fraud begins with small, subtle warning signs—often behavioral—that signal something is wrong. Knowing what to look for can help you intervene before serious financial damage occurs.

Pay attention if your parent:

- Misses bills or routine payments

- Mentions a “new friend” asking for money

- Receives urgent or repeated calls

- Buys gift cards unexpectedly

- Transfers or withdraws large sums

- Becomes secretive about finances

Scammers rely on urgency and fear to override judgment. That is your signal to pause and investigate.

Talk About It Without Shame

This is where many families hesitate, but it may be the most important step you take. Your parent may feel embarrassed, defensive, or even fearful that admitting a mistake could lead to a loss of independence.

Approach the conversation with empathy and respect:

- “I’ve been seeing more scams targeting people our age—can we review things together?”

- “Let’s make sure everything is secure so you stay in control.”

The goal is not to take over. It is to protect while preserving dignity. Trust builds over time—and that trust becomes your strongest defense.

Monitor Accounts and Create a Simple System

Ongoing oversight does not need to be complicated. In fact, simple and consistent habits are often the most effective. Creating a routine helps you catch issues early and gives your parent confidence that someone is watching out for them.

- Review financial statements weekly

- Set up transaction alerts

- Check credit reports at AnnualCreditReport.com

- Consolidate unnecessary accounts

- Add a trusted contact to financial accounts

If appropriate, legal tools such as a durable power of attorney can provide added oversight while preserving independence.

Why Older Adults in Extended Care Settings Face Even Greater Risk

When your parent begins receiving help due to an chronic illness, accident, mobility issues, dementia, or frailty due to aging, their exposure to fraud can increase—not decrease. Care settings introduce more people, more transactions, and more opportunities for access to personal information.

Older adults in assisted living, memory care, or receiving in-home care may have:

- More people entering their living space

- Greater reliance on others for financial or personal tasks

- Cognitive decline or memory loss that limits awareness of scams or unusual activity

- Reduced oversight of daily financial activity

This increased exposure creates more opportunities for both external scams and internal exploitation, especially when oversight is limited. The National Council on Aging warns that elder financial abuse is one of the most common forms of mistreatment, often going unreported.

Financial exploitation is the 'crime of the 21st century,' yet it remains largely invisible because it so often happens at the hands of someone the older adult knows and trusts. The shame and fear of losing independence keep many from coming forward, allowing billions of dollars to be siphoned away from those who can least afford it. — Ramsey Alwin, President and CEO of the National Council on Aging.

In some cases, exploitation can come from individuals trusted to provide care, which makes oversight even more critical.

How To Protect Your Parent in a Facility or With In-Home Care

You cannot monitor every moment—but you can create systems that reduce risk and increase accountability.

The key is to stay involved while putting safeguards in place.

Vet Providers Carefully

Choosing the right provider is your first line of defense. Start by narrowing down extended care options with the LTC News Caregiving Directory.

Don't stop there.

- Verify state licensing and inspection reports

- Ask about employee background checks

- Review staff training on fraud prevention and elder abuse

- Look for a history of complaints or violations

Transparency should be expected—not optional.

Ask About Financial Safeguards

A reputable provider should be able to clearly explain how they protect residents and clients.

Ask direct questions:

- Are staff prohibited from handling resident finances?

- How are personal belongings and documents secured?

- Are there protocols for reporting suspected fraud or abuse?

- Is there supervision of visitors and outside vendors?

Unclear answers should raise concern.

Limit Access to Financial Information

Even well-meaning caregivers do not need access to everything.

Setting boundaries protects your parent without interfering with care.

- Keep financial documents locked

- Do not share PINs or passwords

- Use a separate account for care-related expenses

- Set spending limits where possible

This creates an added layer of protection.

Monitor Activity and Stay Involved

Your presence matters more than any system you put in place.

Regular involvement can deter problems before they begin.

- Visit at different times

- Review statements and invoices

- Watch for missing items or unusual charges

- Notice changes in mood or behavior

If something feels off, trust your instincts.

Watch for Signs of Exploitation in Care Settings

Financial abuse often overlaps with emotional manipulation.

Knowing the signs helps you act quickly.

- Unexplained withdrawals or charges

- Changes in legal or financial documents

- Caregivers limiting access or communication

- Missing valuables

- Sudden isolation or anxiety

These are warning signs that should never be ignored.

Use Oversight Tools and Legal Protections

When appropriate, formal safeguards can provide an extra layer of protection.

- Assign a durable power of attorney

- Set up account alerts

- Add a trusted contact

- Consult a financial advisor or elder law attorney

These tools help ensure someone is watching—even when you cannot be there.

Take Action Now—Small Steps Matter

It’s easy to feel overwhelmed, but you do not need to solve everything at once. Small, consistent actions create meaningful protection over time.

Start with three steps this week:

- Update passwords on one key account

- Secure one group of important documents

- Have one conversation with your parent

Progress—not perfection—is what protects your family.

Frequently Asked Questions About Protecting Older Adults From Scams and Financial Fraud

Why are older adults frequently targeted by scammers?

Older adults are often targeted because many have retirement savings, home equity, regular medical or insurance interactions, and a trusting nature developed over decades. Criminals also exploit isolation, urgency, and confusion caused by rapidly changing technology.

What are the most common scams targeting seniors today?

Common scams include bank impersonation calls, tech support scams, romance scams, Medicare fraud, phishing emails, fake grandchild emergencies, and AI-generated voice scams that mimic family members. Fraudsters often create panic to pressure older adults into acting quickly.

How can you protect aging parents from financial scams?

You can help protect your parent by strengthening passwords, enabling multi-factor authentication, monitoring financial accounts, setting transaction alerts, securing paper records, and having regular conversations about fraud risks. Staying involved consistently is one of the best defenses.

What are warning signs that an older adult may be the victim of fraud?

Warning signs include missed bills, unusual withdrawals, gift card purchases, secrecy about finances, repeated urgent phone calls, sudden new friendships asking for money, or emotional changes such as anxiety or confusion.

How do scammers use artificial intelligence to target seniors?

Scammers increasingly use AI voice-cloning technology to imitate family members or trusted individuals. These scams can sound highly realistic and are often used during fake emergencies to pressure older adults into sending money quickly.

What documents should older adults keep secure?

Important documents include Social Security cards, birth certificates, wills, trusts, insurance policies, Medicare information, Long-Term Care Insurance policies, tax returns, bank records, and powers of attorney. These documents should be stored in a locked, fireproof location.

How can families safely monitor an older parent’s finances?

Families can create a simple oversight system by reviewing statements weekly, using transaction alerts, consolidating accounts, checking credit reports, and designating trusted contacts on financial accounts. Durable powers of attorney may also help when appropriate.

Are older adults in assisted living or home care at greater risk for fraud?

Yes. Older adults receiving long-term care services or living in assisted living or memory care settings may face greater fraud risk due to increased dependence on others, cognitive decline, and more people having access to personal information and financial activity.

How can you protect a loved one in assisted living or receiving in-home care?

You can reduce risks by vetting care providers carefully, reviewing licensing and inspection reports, limiting access to financial information, monitoring statements regularly, visiting frequently, and watching for behavioral or financial warning signs.

Does Medicare cover financial fraud losses or identity theft recovery?

No. Medicare does not reimburse victims for fraud losses or identity theft. However, older adults should report Medicare-related scams immediately and monitor Medicare Summary Notices for suspicious activity.

What should you do immediately if your parent is scammed?

Contact the bank or financial institution immediately, freeze compromised accounts if necessary, change passwords, report the fraud to local authorities and the Federal Trade Commission, and monitor credit reports for unusual activity. Quick action may reduce financial damage.

Why is elder financial abuse often underreported?

Many older adults feel embarrassed, ashamed, or fearful that reporting fraud could cause them to lose independence or financial control. Criminals rely on that silence, which is why supportive family conversations are so important.

Frequently Asked Questions

How do scammers target older adults?

They use phone calls, emails, texts, and social media to create urgency or emotional pressure. Many impersonate government agencies, tech support, or family members.

Should you monitor your parent’s accounts?

Yes, with permission. Regular monitoring helps detect fraud early and limit financial damage.

What is the best first step to protect your parents?

Start with a conversation. Then secure key accounts and review financial activity regularly.

Can identity theft happen in assisted living or with caregivers?

Yes. Increased access to personal information and finances can create additional risk if safeguards are not in place.

What are the biggest warning signs of fraud?

Unexpected withdrawals, urgent money requests, gift card purchases, and secrecy about finances are key red flags.