Dementia Planning: Decisions Families Regret Waiting On

About This Article

Many families only begin planning for dementia after memory problems appear, but by then, critical legal, financial, and caregiving decisions may already be limited. Early preparation helps protect independence, reduce family conflict, and safeguard retirement savings if cognitive decline eventually requires long-term care.

Mallory Knee

Mallory Knee is a freelance writer for multiple online publications where she can showcase her affinity for all things beauty and fashion.

Table of Contents

- Dementia Often Reveals Planning Gaps Families Didn’t Expect

- Dementia Is Becoming More Common as Americans Live Longer

- Decisions Families Most Regret Delaying

- Long-Term Care Planning Belongs in Every Retirement Strategy

- How Long-Term Care Insurance Can Help Protect Retirement Savings

- Guardianship or Conservatorship Can Become Necessary Without Planning

- Practical Steps Families Can Take Now

- Key Legal Documents to Have in Place

- Early Planning Protects Independence and Family Peace

You may assume there will always be time to plan for dementia or other cognitive decline. Yet many families discover too late that critical legal, financial, and caregiving decisions were never made—leaving loved ones confused, involved in court, and facing costly care decisions during a crisis.

Early planning protects independence, reduces family conflict, and helps safeguard retirement savings if memory loss or chronic illness eventually requires long-term care.

Dementia Often Reveals Planning Gaps Families Didn’t Expect

You probably expect retirement planning to focus on investments, Social Security, and travel goals. Few people want to think about dementia or losing the ability to manage daily life. Yet that moment arrives for many families.

A missed bill payment. Repeated stories in the same conversation. Confusion about a bank account that has been managed for decades. Those early warning signs often reveal something else: the family never discussed who would make decisions if memory and judgment decline.

When a diagnosis arrives, adult children and spouses frequently discover they lack the legal authority to help. Financial institutions may refuse to share account information. Doctors may require formal medical authorization before discussing treatment options.

Planning can prevent those barriers. Legal documents such as advance directives and powers of attorney allow trusted individuals to step in if cognitive decline affects decision-making.

Advance directives allow people to express their wishes for care before they lose the ability to decide. — Barak Gaster, MD, professor of medicine at the University of Washington and developer of a dementia advance directive. Barak Gaster, MD, professor of medicine at the University of Washington and developer of a dementia advance directive.

He notes that many families struggle because planning often happens too late to document those preferences clearly. Without these preparations in place, families may find themselves unable to access accounts, coordinate care, or even speak with healthcare providers during critical moments. Without planning, families often face the worst possible moment to make critical decisions.

Families often assume they will have time to organize finances or legal authority later - Jason Karlawish, MD, professor of medicine and medical ethics at the University of Pennsylvania and co-director of the Penn Memory Center.

But dementia progressively affects decision-making capacity, and once that capacity is lost, legal options become far more limited.

Dementia Is Becoming More Common as Americans Live Longer

Population aging is one reason dementia planning has become increasingly important. According to the Alzheimer’s Association 2025 Alzheimer’s Disease Facts and Figures report, an estimated 7.2 million Americans age 65 and older are living with Alzheimer’s disease in 2025, the most common form of dementia. About 74% of those individuals are age 75 or older.

- Review: Alzheimer’s Association, 2025 Alzheimer’s Disease Facts and Figures

The global picture is also significant. The World Health Organization reports more than 55 million people worldwide are living with dementia, and nearly 10 million new cases are diagnosed every year. As we live longer, the risk of dementia increases, and the impact on our families and finances is significant.

As these dementia cases rise, families increasingly provide care, as they often have not planned for long-term care. In fact, 63 million Americans now provide unpaid care for family members, reflecting the growing caregiving demands created by longevity and chronic illness.

Alzheimer’s disease slowly robs people of memory, thinking skills and eventually the ability to carry out simple tasks. Early planning allows individuals and families to prepare for the future and ensure their wishes are respected. — Joanne Pike, DrPH, president and CEO of the Alzheimer’s Association, in the organization’s 2025 report.

Decisions Families Most Regret Delaying

When families look back after a dementia diagnosis, several missed decisions appear again and again.

Establishing Legal Authority

Banks, insurance companies, and healthcare providers require formal legal documents before allowing someone to act on another person’s behalf.

Key documents typically include:

- Durable financial power of attorney

- Healthcare power of attorney

- Advance medical directive (living will)

- HIPAA medical privacy authorization

Without these documents, even a spouse or adult child may be unable to manage accounts or approve medical care. Families sometimes learn this only after a crisis—when the only option may be pursuing court-appointed guardianship, which can involve legal costs, court oversight, and public records.

Discussing Long-Term Care Preferences

Many families avoid discussing extended care needs because the topic feels uncomfortable. However, dementia and other age-related conditions often require years of care costing hundreds of thousands of dollars, even in the millions, with health insurance and Medicare not paying anything beyond short-term skilled care.

Professionals often advise individuals to plan for incapacity while their loved one can still communicate their intent and preferences clearly. That preparation coordinates medical directives, financial authority, and long-term care decisions within a broader estate structure.

Important conversations should address questions such as:

- Would you prefer to receive care at home as long as possible?

- When would assisted living be appropriate?

- Would a memory care community be preferred if dementia progresses?

- Who should make care decisions if family members disagree?

- Have you completed the paperwork for items such as a Medical Power of Attorney?

Clear answers help prevent conflicts among adult children and reduce stress during medical crises.

Preparing Financial Oversight

Cognitive decline often affects financial judgment before families recognize the problem.

Early warning signs may include:

- Unpaid bills or duplicate payments

- Confusion about investments or property

- Unusual withdrawals or spending

- Increased vulnerability to scams

Financial organization and oversight can protect retirement savings and reduce the risk of fraud.

Updating Estate Planning

Many people delay reviewing their wills, trusts, and beneficiary designations. However, legal documents must be signed while a person has a clear mental capacity.

If dementia progresses too far, the individual may no longer legally qualify to sign new documents or update estate plans. Outdated instructions can create complications that last for years.

Long-Term Care Planning Belongs in Every Retirement Strategy

The risk of dementia, chronic illness, and age-related frailty means long-term care planning should be part of a comprehensive retirement strategy—not something families address only after a diagnosis.

Federal research from the U.S. Department of Health and Human Services shows how significant your long-term care risk is, and the lack of planning can easily create a family crisis. If you reach the age of 65, the risk of needing help with daily living activities or supervision due ot dementia is 56 percent. That is not a risk worth ignoring.

Health conditions that often lead to long-term care include:

- Alzheimer’s disease and other dementias

- Stroke

- Parkinson’s disease

- Severe arthritis

- Age-related frailty

These conditions can make routine activities difficult, including:

- Bathing

- Dressing

- Toileting

- Mobility

- Eating

- Medication management

- Supervision for safety

When families fail to plan for these possibilities, spouses and adult children frequently become caregivers. That is a burden most loved ones can't manage for very long, and the savings are drained to pay for the quality care required. With long-term care costs rising every year, the need for extended care can become a financial disaster on top of a family crisis.

How Long-Term Care Insurance Can Help Protect Retirement Savings

One of the most effective financial tools for managing future care costs is Long-Term Care Insurance. A tax-qualified LTC policy provides guaranteed tax-free benefits to pay for the quality extended care you desire, reducing the stress on your family.

An LTC policy can help pay for services such as:

- in-home caregiving

- assisted living communities

- memory care facilities

- nursing homes

- home modifications, medical alert systems, and other equipment

Guardianship or Conservatorship Can Become Necessary Without Planning

When families delay planning, the courts may eventually become involved. That situation happens more often than many people realize when aging parents never completed legal preparations before cognitive decline began.

Dementia affects a person’s legal ability to make decisions. Once a doctor determines someone no longer understands legal documents or financial choices, creating new powers of attorney or updating estate plans may no longer be possible.

At that point, families may have little choice but to pursue guardianship or conservatorship through the courts in order to manage their finances or make medical decisions.

Guardianship proceedings can involve:

- Court petitions

- Medical evaluations

- Attorney representation

- Ongoing court supervision

Beyond legal expenses, guardianship can expose private financial information and sometimes lead to disagreements among family members over how decisions should be made. The chaos these family disagreements can create often leads to impaired family relationships that may never be repaired.

Planning early helps families avoid these complications and ensures you or your loved one's wishes guide important decisions if memory or judgment begins to decline.

Practical Steps Families Can Take Now

Several practical actions can reduce uncertainty later.

- Confirm decision-makers: Choose trusted individuals for financial and healthcare decisions.

- Review estate and financial plans: Ensure beneficiary designations and account ownership match your estate plan.

- Organize important documents: Secure financial records, insurance policies, and digital passwords.

- Hold a family discussion: Clarify expectations and responsibilities among adult children.

- Consult professionals: Work with estate planning attorneys, financial advisors, and elder law specialists.

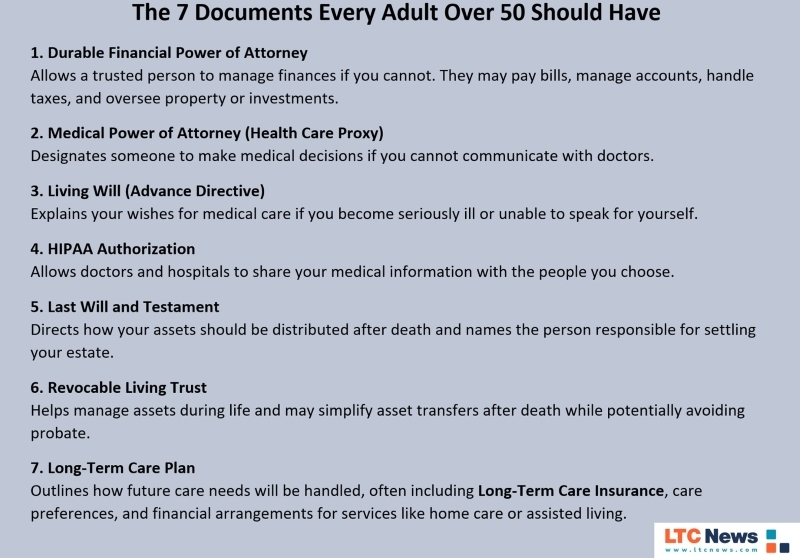

Key Legal Documents to Have in Place

Dementia planning often starts with legal documents that allow someone you trust to step in if you can no longer make decisions yourself. These documents should be completed while you are still mentally capable of understanding and signing them.

Without them, even a spouse or adult child may not have the authority to manage finances or make medical decisions. Here are the most important documents families should consider.

Durable Financial Power of Attorney

A durable financial power of attorney allows you to appoint someone to manage financial matters if you become unable to handle them yourself.

The person you choose (called your agent) may be able to:

- Pay bills

- Manage bank accounts and investments

- Handle taxes

- Oversee property or real estate

- Manage retirement accounts or insurance matters

“Durable” means the authority remains valid even if you later become mentally incapacitated. Without this document, families often must go to court to obtain guardianship in order to access accounts or manage finances.

Medical Power of Attorney (Health Care Proxy)

A medical power of attorney, sometimes called a health care proxy, allows you to designate someone to make medical decisions if you cannot communicate with doctors yourself.

That person may make decisions about:

- Medical treatments

- Hospital care

- Medications

- Surgeries or procedures

- Long-term care arrangements

Doctors typically rely on this document when patients cannot express their wishes.

Living Will (Advance Directive)

A living will, also known as an advance directive, explains the type of medical care you want if you become seriously ill or unable to communicate.

It can address decisions about:

- Life-support treatments

- Resuscitation

- Ventilators or feeding tubes

- End-of-life care preferences

The living will provides guidance to both doctors and family members so they understand your wishes during difficult medical situations.

HIPAA Authorization

A HIPAA authorization form allows doctors and hospitals to share medical information with the individuals you designate. Without this form, privacy laws may prevent healthcare providers from discussing medical conditions or treatment plans with family members.

This document ensures your chosen decision-makers can stay informed about your health.

Will or Revocable Living Trust

A will or revocable living trust outlines how your assets should be distributed after death. While these documents focus on estate planning rather than medical decisions, they are still an important part of preparing for cognitive decline.

Updating these documents early ensures your financial legacy follows your wishes.

Early Planning Protects Independence and Family Peace

Many dementia planning regrets share the same root cause: hesitation. Conversations about aging, incapacity, and caregiving are difficult. Yet avoiding those conversations can create even greater stress later.

Adult children often feel uncomfortable raising the topic, especially when parents appear healthy and independent. However, if your parents are still of sound mind, that is exactly when these conversations should happen. Encourage them to share their wishes about finances, healthcare decisions, and future care preferences now—before a health crisis forces rushed decisions.

Planning early protects personal autonomy, financial security, and family relationships. Planning for long-term care and the consequences of aging helps avoid a family crisis later in life. Most people plan before they retire, and Long-Term Care Insurance is usually purchased between the ages of 47 and 67. Be sure to seek an LTC Insurance specialist to get accurate quotes and information.

Starting that conversation today with older parents may be one of the most important steps you take for their future. Thinking about your aging now, at a younger age with good health, will ensure you have access to quality extended care services without impacting your future income and assets or creating a family crisis years from now.

Frequently Asked Questions

What legal documents are essential for dementia planning?

Common documents include:

- Durable financial power of attorney

- Healthcare power of attorney

- Living will or advance directive

- HIPAA authorization

- Updated will or trust

Does Medicare cover dementia care?

Medicare generally covers short-term skilled nursing or rehabilitation after hospitalization, usually up to 100 days under specific conditions. Medicare does not cover long-term custodial care, including assistance with bathing, dressing, or memory supervision.

Can Long-Term Care Insurance help with dementia care?

Yes. All tax-qualified Long-Term Care Insurance policies cover care related to cognitive impairment, including Alzheimer’s disease and other dementias. Benefits can pay for in-home care, assisted living, memory care, or nursing home services. However, you must have a policy in place before you need care. Be sure to start planning now, ideally before retirement. For loved ones who already need extended care, if they don't have Long-Term Care Insurance and your loved one has a life insurance policy, you could sell it for cash now to cover the costs of extended care.

When should families begin dementia planning?

Experts recommend beginning discussions in your 50s or early 60s, while cognitive health remains strong and legal capacity is clear.

How can families estimate the cost of dementia care?

Long-term care costs vary by location and level of care. Families can review current pricing using the LTC News Cost of Care Calculator, which tracks care costs nationwide.

Where can families find professional caregivers?

Families can locate professional caregiving services using the LTC News Caregiver Directory, which lists home care agencies, assisted living communities, and other care providers across the United States.