AARP Report: $600 Billion in Unpaid Caregiving Exposes Strain on U.S. Long-Term Care System

About This Article

AARP research finds that unpaid caregiving is now worth $600 billion annually, exposing the strain that long-term care places on American families and finances and why planning is critical.

James Kelly

LTC News staff writer specializing in long-term care and aging.

Table of Contents

- You’re Doing More Than Helping—You’re Holding Up the System

- A $600 Billion Backbone Few People See

- 63 Million Americans—and Many Don’t Identify as Caregivers

- Why Family Caregiving Is Expanding So Quickly

- Workforce Shortages Are Limiting Access to Quality Care

- Caregiving is Time-Consuming

- The Personal Cost: Financial, Physical, and Emotional

- The Coverage Gap That Catches Families Off Guard

- Why Long-Term Care Planning Is No Longer Optional

- How Long-Term Care Insurance Changes the Equation

- A System at a Tipping Point

- What Happens Next Is Up to You

You may already be doing it, or know someone who does. Many people today help a parent, spouse, or loved one without calling themselves caregivers. Yet that is exactly what they are, despite not being trained or prepared for a very personal and emotional job.

A new AARP report shows that family caregiving now represents a $600 billion pillar of the U.S. long-term care system, raising urgent concerns about sustainability, financial strain, and the need for better planning. Yet, even though more than half of Americans who reach the age of 65 will need long-term care services, too many families not only ignore the problem, but they also don't even talk about it until a family crisis occurs.

As long-term care becomes less affordable, caregiving increasingly shifts to family members… often beyond what they realistically have the time, resources or capacity to handle.” — Alan Weil, senior vice president at the AARP Public Policy Institute.

You’re Doing More Than Helping—You’re Holding Up the System

You drive to appointments. You organize medications. You check in more often than you used to. At first, it feels manageable. Then it becomes routine. Then it becomes essential. Your life revolves around being a caregiver; your career, family, and other responsibilities become second behind this job. Often, the care recipient is unhappy that a daughter, son, or other loved one has had to become a caregiver for them.

According to a new report from AARP released March 26, 2026, what you’re doing is not just personal—it is part of a massive, unpaid system that now underpins long-term care in the United States.

That system is growing—and under increasing pressure.

A $600 Billion Backbone Few People See

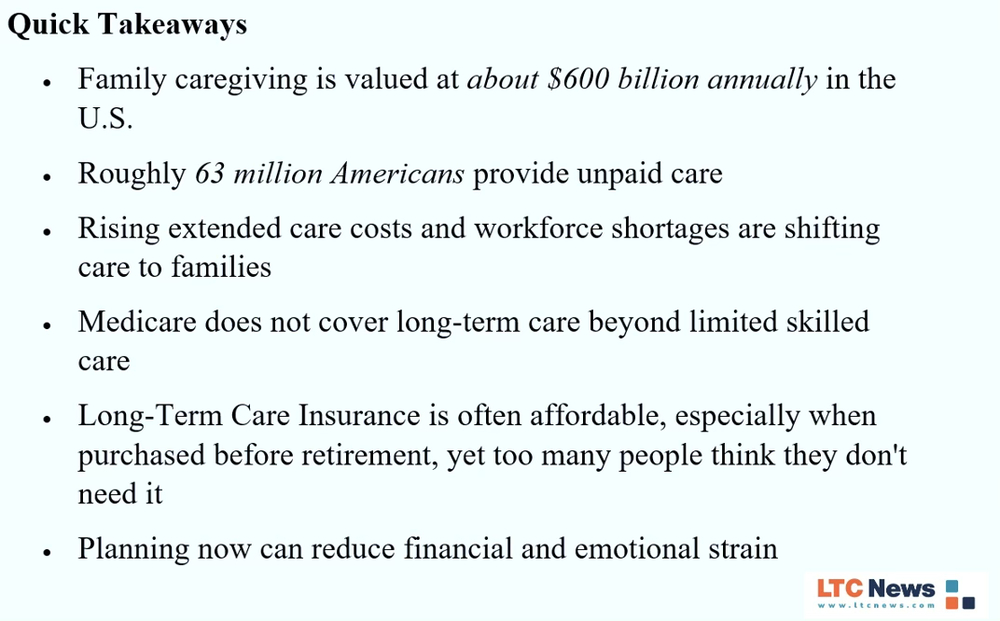

The AARP report estimates the economic value of unpaid family caregiving at approximately $600 billion annually in the United States.

That figure reflects:

- Billions of hours of care annually

- Support that exceeds total out-of-pocket health care spending

- A workforce larger than many formal health care sectors

The AARP Public Policy Institute has long described family caregivers as the backbone of long-term care in America.

Family caregivers are a backbone of our health and long-term care systems—often providing complex care with little or no training… and too often doing it alone.” — Myechia Minter-Jordan, CEO, AARP

Family caregivers are not just supporting loved ones—they are sustaining the entire long-term care system, often at significant personal cost. Without that support, the system would struggle to function.

63 Million Americans—and Many Don’t Identify as Caregivers

Caregiving today is widespread, and often unrecognized.

- About 63 million Americans provide unpaid care

- Nearly 1 in 4 adults is involved in caregiving

- Many do not identify themselves as caregivers

Responsibilities often include:

- Managing medications and appointments

- Assisting with bathing, dressing, and mobility

- Coordinating care after hospital stays

- Providing supervision for cognitive decline

LTC News reporting, based on national caregiving data, shows unpaid caregiving has increased by about 45% since 2015.

Why Family Caregiving Is Expanding So Quickly

Several forces are reshaping how care is delivered in the United States.

- Rising Costs Are Pushing Care Back Home

Long-term care costs continue to climb across all settings. Using the LTC News Cost of Care Calculator, you can see how costs vary by ZIP code, but trends remain clear:

- In-home care costs are rising due to labor shortages and increasing demand for extended care

- Assisted living and memory care continue to increase in price

- Nursing homes remain the most expensive option

As professional care becomes less affordable, and not enough people have Long-Term Care Insurance in place, families are forced to step in.

- Americans Are Living Longer—But Not Always Healthier

A longer life expectancy often means more years with chronic conditions. People require long-term care due to a chronic illness, accident, mobility problems, dementia, or frailty.

Common drivers include:

- Alzheimer’s disease and other dementias

- Heart disease and diabetes

- Mobility limitations and frailty

These conditions typically require ongoing support, often for several years.

Workforce Shortages Are Limiting Access to Quality Care

The long-term care workforce is under growing pressure—and you’re likely already feeling the effects if you’ve tried to find care for a parent or plan ahead for your own future.

Across the country, fewer workers are entering caregiving roles. These jobs are physically demanding, emotionally taxing, and often lower-paying compared to other healthcare positions. As demand rises, providers are struggling to recruit and retain staff, creating a widening gap between those who need care and those available to provide it.

At the same time, wages are increasing as agencies compete for a limited pool of caregivers. While higher pay is necessary to attract workers, it is also driving up the cost of care for families. Home care, assisted living, and skilled nursing services are all becoming more expensive—often faster than inflation.

Staffing shortages are also limiting access to care in very real ways:

- Home care agencies may have waitlists or limited hours available

- Assisted living communities may restrict admissions due to staffing ratios

- Nursing homes may reduce capacity or close units entirely

- Rural and underserved areas face even greater shortages

The result is a system under strain, where even families who can afford care may struggle to find it when they need it.

Experts tell LTC News that workforce shortages across long-term care settings are one of the most pressing challenges facing our aging population. Without enough professionally trained caregivers, access to quality care becomes increasingly limited.

With the increased cost of extended care, and not enough people with Long-Term Care Insurance to pay the bill, families are increasingly filling that gap—often without preparation, training, or support. What begins as helping with errands or transportation can quickly escalate into managing medications, assisting with mobility, or providing supervision for a loved one with dementia.

👉What is Long-Term Care Insurance and What Does it Cover?

This shift has real consequences:

- Family caregivers face emotional and physical strain

- Many reduce work hours or leave jobs entirely

- Financial pressure builds as out-of-pocket costs rise

- Quality of care can vary without professional support

You may assume the care will be there when you need it. But the reality is changing. Workforce shortages are reshaping access, affordability, and the entire long-term care landscape—making early planning more important than ever.

Caregiving is Time-Consuming

The AARP report shows that family caregivers are spending more time providing this care, averaging 27 hours each week. Trying to balance caregiving and other responsibilities adds to the stress.

More than half, 57 percent, now provide high-intensity care, meaning they spend more hours helping with daily tasks like bathing and dressing, as well as complex medical and nursing tasks like wound care and administering injections.

The value of all this family caregiving exceeds total federal, state, and local Medicaid spending nationwide, and almost doubles all out-of-pocket health care spending.

Read the full report here.

The Personal Cost: Financial, Physical, and Emotional

Unpaid caregiving carries real consequences. Many adult children tell their parents not to worry about it, only to find out, too late, that the job is physically, emotionally, and financially demanding.

Despite loving an ailing family member very much, in-home and long-distance caregiving can negatively affect physical health, mental wellness, finances, and relationships. This can lead to feelings of guilt and anxiety, further worsening burnout." — Dr. Namirah Jamshed, Director of the Geriatric Medicine Fellowship Program and Medical Director of the House Calls Program at UT Southwestern Medical Center.

Jamshed says that balancing several roles: taking care of aging parents, raising a family, working, and trying to squeeze in time for relationships and self-care. can, over time, cause physical and emotional symptoms that diminish quality of life – for you and your aging loved one.

Research from AARP and related studies shows:

- Many caregivers reduce work hours or leave jobs

- Stress and fatigue increase over time

- Health can decline with prolonged caregiving responsibilities

- Many caregivers also face out-of-pocket costs for home modifications, transportation, and medical supplies (AARP, U.S.)

What begins as occasional help can become a long-term commitment that reshapes your daily life.

The Coverage Gap That Catches Families Off Guard

Many families are surprised to learn what insurance does—and does not—cover.

- Medicare covers short-term skilled care only, typically up to 100 days, and only after a qualifying hospital stay

- Coverage is limited and does not include ongoing custodial long-term care

- Health insurance does not cover extended long-term care services

- Medicaid will only pay for long-term care for those with limited financial resources

- Long-Term Care Insurance is available, but is usually purchased when someone is younger (often between ages 47 and 67), when they are reasonably healthy, because of medical underwriting

That gap leaves families responsible for most care needs.

Why Long-Term Care Planning Is No Longer Optional

The AARP report reinforces a critical reality that without a plan, caregiving becomes a family responsibility. A plan starts with conversation and should start before a crisis starts.

Planning ahead allows you to:

- Protect retirement savings

- Reduce the burden on your children

- Access better care options, including care at home

- Maintain independence longer

Waiting limits your choices and often forces you to make decisions during a crisis.

How Long-Term Care Insurance Changes the Equation

One of the most effective planning tools is Long-Term Care Insurance.

Modern LTC Insurance policies:

- Provide guaranteed tax-free benefits for qualified care

- Cover care at home, assisted living, memory care, or nursing facilities

- Help reduce reliance on unpaid family caregivers, allowing them time to be family

Many policies now offer flexible “pool of money” designs, allowing benefits to be used as needed over time. Although you might have read articles that say Long-Term Care Insurance is expensive, an LTC policy is custom-designed and can be very affordable, especially if you purchase it in your 40s and 50s.

👉 How Much Does Long-Term Care Insurance Cost?

👉 Compare Long-Term Care Insurance Companies and Products

A System at a Tipping Point

Family caregiving is no longer a backup plan. It is a central part of how care is delivered in the United States.

It is:

- Essential

- Expanding

- Under increasing strain

The AARP report highlights a system that relies heavily on families but offers limited structural support.

What Happens Next Is Up to You

Now is the time to:

- Start a conversation with your family

- Use the LTC News Cost of Care Calculator to understand real costs in your area and compare care options nationwide

- If you have a loved one who needs quality long-term care service now, explore the LTC News Caregiver Directory, with more than 80,000 providers nationwide

- Review Long-Term Care Insurance options while you still have choices

Planning is not just about finances—it is about protecting your independence, your choices, and the people who may otherwise be forced to step in.

Frequently Asked Questions

Why do families wait too long to plan for long-term care?

Many families delay planning because it is uncomfortable to discuss or feels far off. Others assume care will be available or covered by insurance. Unfortunately, these conversations often happen only after a health crisis—when options are limited and decisions are rushed.

How many Americans are providing unpaid care?

About 63 million Americans provide unpaid care for a family member or loved one. That represents nearly one in four adults, highlighting how widespread caregiving has become in the United States.

What is the difference between Medicare, Medicaid, and Long-Term Care Insurance?

- Medicare: Covers short-term medical care, not long-term care

- Medicaid: Covers long-term care only for those with limited financial resources

- Long-Term Care Insurance: Provides benefits to pay for extended care at home, in assisted living, or in a nursing facility

Understanding these differences is critical to avoiding unexpected costs.

What are the biggest challenges family caregivers face?

Caregiving can affect nearly every part of your life. Common challenges include:

- Physical strain from lifting, mobility assistance, and daily care

- Emotional stress, anxiety, and burnout

- Financial pressure from lost income and out-of-pocket expenses

- Balancing caregiving with work and family responsibilities

Many caregivers are unprepared for how demanding the role becomes over time.

How much time do family caregivers spend providing care?

Family caregivers spend an average of about 27 hours per week providing care. More than half are now considered “high-intensity caregivers,” meaning they help with both daily living activities and complex medical tasks.

Why is family caregiving increasing?

Several factors are driving the growth of unpaid caregiving:

- People are living longer, often with chronic health conditions

- Long-term care costs are rising across all settings

- Workforce shortages are limiting access to professional care

- Many families do not have Long-Term Care Insurance

As a result, more families are stepping in to provide care themselves.

When should you plan for long-term care?

The best time to plan is before you need care—often in your 40s, 50s, or early 60s while you are still healthy. Planning early gives you more options, better pricing for Long-Term Care Insurance, and greater control over your future care decisions.

What is unpaid family caregiving?

Unpaid family caregiving refers to the support you provide to a loved one without compensation. This can include helping with daily activities like bathing, dressing, and mobility, managing medications, coordinating medical care, or supervising someone with dementia. Many people do not identify themselves as caregivers—even though they are performing essential care tasks.

Does Medicare pay for long-term care?

No. Medicare only covers short-term skilled care, typically up to 100 days after a qualifying hospital stay. It does not cover ongoing custodial care, such as help with bathing, dressing, or supervision due to dementia.

How does Long-Term Care Insurance help families?

Long-Term Care Insurance helps cover the cost of extended care services, reducing the burden on family caregivers. Policies typically:

- Provide tax-free benefits for qualified care

- Cover care at home or in facilities

- Help protect savings and retirement income

- Allow family members to focus on being family—not full-time caregivers