Why Life Insurance Claims Get Denied—and How to Fight Back

About This Article

You assume life insurance will protect your family—but claim denials happen more often than you think. This guide explains why claims get denied and what you can do to secure the benefits your loved one intended.

Jacob Thomas

Jacob Thomas writes on health, wellness, and retirement topics, including aging, caregiving, insurance, and long-term care.

Table of Contents

- Policy Rules That Can Trigger a Denial

- The Contestability Period: The First Two Years Matter Most

- The Suicide Clause: A Difficult but Important Provision

- High-Risk Exclusions You Might Not Expect

- How Insurers Investigate Claims

- What They Review

- Administrative Reasons Claims Get Denied

- Growing Role of Artificial Intelligence in Claims

- What You Can Do If a Claim Is Denied

- Step 1: Read the Denial Letter Carefully

- Step 2: Gather Evidence and File an Appeal

- Comparing Your Appeal Options

- Why This Matters for Your Retirement and Long-Term Care Plan

- Take Control Before a Crisis Happens

You expect life insurance to provide security, not stress. But when a claim is delayed or denied after a loved one’s death, it can feel like a second loss. You’re grieving, and suddenly you’re dealing with paperwork, confusion, and uncertainty. No matter your loved one's age, you expect the death benefit to be paid. For older adults, these benefits might help cover medical or long-term care bills that remain.

Life insurance claims can be denied for several reasons, including errors on the original application, policy exclusions, missed premium payments, or disputes over beneficiaries. The most common issues involve misrepresentation during the contestability period, administrative errors, or undisclosed risks.

However, many denied claims can be successfully appealed by reviewing the denial letter, gathering supporting documentation, and following the insurer’s appeals process. It happens more often than most people realize, and often when families are least prepared to deal with it. Estimates suggest 10 to 20 percent of life insurance claims face delays or initial denials, leaving families searching for answers.

Understanding why claims are denied and what you can do next can help protect your family’s financial future.

Policy Rules That Can Trigger a Denial

A life insurance policy is a legal contract. Every payout depends on the terms written in that contract. If certain conditions are met, the insurer can deny the claim even if premiums have been paid for years.

The Contestability Period: The First Two Years Matter Most

Most policies include a two-year contestability period. During this time, insurers can review the original application for errors or omissions.

Common issues include:

- Undisclosed medical conditions (such as diabetes or heart disease)

- Failure to report smoking or substance use

- Leaving out high-risk hobbies or occupations

Even unintentional mistakes can be considered material misrepresentation, which can void the policy. This is a global challenge, as incomplete or inaccurate disclosure is also a leading cause of claim denial in growing markets like India. It's also important to note that if a policyholder adds a new rider or increases the policy's value, it can sometimes restart the two-year contestability period for that specific change.

The Suicide Clause: A Difficult but Important Provision

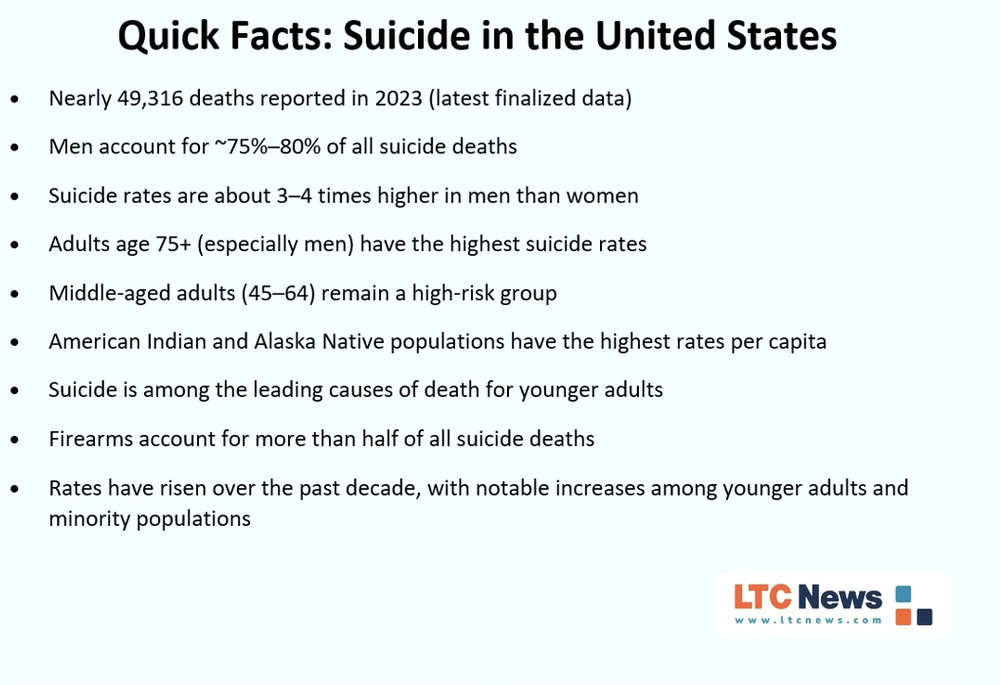

After the contestability period ends, the question of does life insurance pay for suicidal death is generally answered with a yes, but the specifics can vary based on the policy's language and state laws. Most policies include a suicide clause. Suicide remains a serious and growing public health concern in the United States, with the most recent data from the Centers for Disease Control and Prevention showing nearly 50,000 deaths in 2023, the highest number ever recorded.

While suicide affects people across all backgrounds, the risk is not evenly distributed. Men account for roughly three-quarters of all suicide deaths, and the likelihood increases significantly with age, especially among older men.

Demographics reveal important patterns. Older adults, particularly men aged 75 and older, have the highest suicide rates in the country. Middle-aged adults (45–64) also face elevated risk, often tied to health challenges, financial stress, caregiving responsibilities, and life transitions like retirement.

“Suicide rates are rising fastest among men 55 and older, with men over 75 at the highest risk.”

— Edwin Boudreaux, PhD, professor of emergency medicine.

Since most life insurance policies have a suicide clause, it can adversely impact the approval of a claim.

- If death occurs by suicide within the first two years, benefits are typically denied

- Instead, insurers usually refund premiums paid

After that period, policies often provide coverage, but rules vary by insurer and state law.

High-Risk Exclusions You Might Not Expect

Even after the contestability period ends, exclusions still apply.

Claims may be denied if death is linked to:

- Illegal activity (such as committing a felony)

- Undisclosed hazardous activities (e.g., aviation or scuba diving)

- Military action or acts of war

- Drug or alcohol-related causes

How Insurers Investigate Claims

Once a beneficiary submits a claim, the insurer will request several key documents to verify the policyholder's death and its circumstances. The process can feel invasive—but it is standard. This investigation typically includes the official death certificate, and they may also ask for medical records, autopsy reports, and police reports if applicable.

The investigation is always most thorough if the death occurs within the contestability period. The frequency of these investigations and resulting disputes is significant; at the end of 2022, nearly $970 million in death benefits were under active dispute with insurance companies, highlighting how often these reviews can lead to delays or denials.

What They Review

Expect requests for:

- Death certificate

- Medical records

- Autopsy reports (if applicable)

- Police reports (in certain cases)

Claims within the contestability period often face deeper scrutiny. At the end of 2022, nearly $970 million in life insurance benefits were under dispute, highlighting how often reviews can lead to delays or denials.

Administrative Reasons Claims Get Denied

Not all denials are tied to the cause of death. Many stem from procedural issues that are often avoidable.

Common Problems:

- Policy lapse: Missed premium payments beyond the grace period

- Incomplete paperwork: Missing forms or documentation

- Beneficiary disputes: Conflicts due to divorce or outdated designations

- No named beneficiary: Payment goes through probate, delaying access

Regular policy reviews can help prevent many of these issues.

Growing Role of Artificial Intelligence in Claims

The insurance industry is evolving. In recent years, the insurance industry has increasingly turned to artificial intelligence to handle claims at high speed. While automation can accelerate approvals, it also introduces new challenges for families.

Critics worry that these systems can lead to rapid-fire denials without adequate human review. This trend is already causing concern in healthcare, where over 60% of physicians report that unregulated AI tools are systematically denying necessary coverage. This trend creates a new dynamic where families may find themselves fighting a decision made by an algorithm, a concern echoed by industry experts who predict a rise in claims related to failing AI systems and wrong decisions.

More companies are now using artificial intelligence to process claims more efficiently. While automation can speed approvals, industry experts have raised concerns that automated systems may contribute to faster denials without full human review.

Legal experts also caution that relying too heavily on automation introduces new risks. If a claim is denied based solely on AI output without meaningful human oversight, it could raise concerns about fairness—or even bad faith in the claims process.

This trend mirrors challenges seen in health care, where automated decision-making has raised questions about fairness and oversight.

What You Can Do If a Claim Is Denied

A denial is not always the final outcome. You have the right to appeal—and many families succeed.

Step 1: Read the Denial Letter Carefully

The insurer must explain:

- The specific reason for denial

- The policy clause used to justify it

This letter becomes your roadmap for appeal.

Step 2: Gather Evidence and File an Appeal

Do not be discouraged from taking action. While data shows that fewer than 0.2% of beneficiaries formally contest a denial, those who do often succeed. In fact, approximately 40% of appealed denials are ultimately overturned in favor of the beneficiary. To begin, write a formal appeal letter that directly addresses the reason for denial stated by the insurer. Include any supporting evidence you have, such as medical records that clarify a condition, proof of premium payments, or witness statements.

Take action promptly. Include:

- Medical records to clarify conditions

- Proof of premium payments

- Any missing documentation

While very few beneficiaries appeal, those who do often see results. About 40% of appealed denials are overturned.

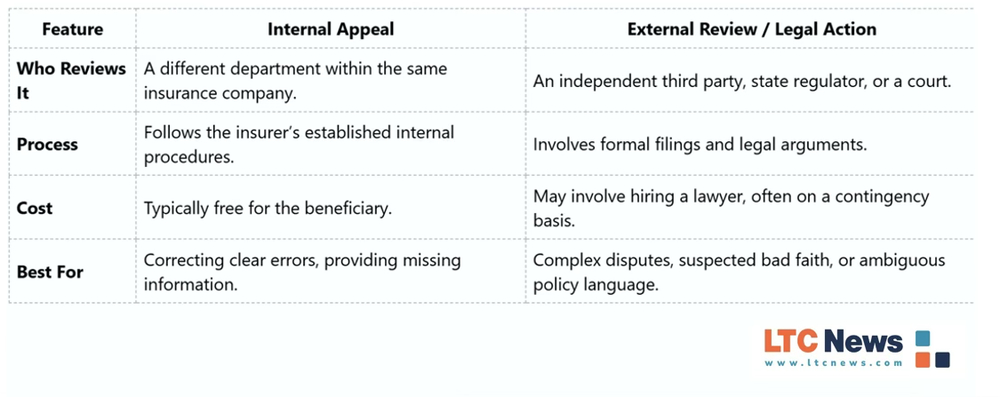

Comparing Your Appeal Options

When you contest a denial, you generally have two main paths you can take. An internal appeal is the first step, while an external review or legal action is an option for more complex disputes or if the internal appeal fails.

Internal Appeal

- Reviewed within the insurance company

- No cost

- Best for correcting errors

External Review or Legal Action

- Independent review or court involvement

- May require legal support

- Best for complex disputes

Why This Matters for Your Retirement and Long-Term Care Plan

Life insurance is only one part of your financial strategy, but it’s often the moment families realize how unprepared they are for what comes next. Planning for aging means preparing for both income protection and care needs.

According to the U.S. Department of Health and Human Services, more than half of adults who reach age 65 will need long-term care.

At the same time:

- Medicare and health insurance only cover limited short-term care

- Most long-term care—whether at home or in a facility—is paid out of pocket unless you’ve planned ahead

- Extended care costs can last years

- Families often absorb financial and caregiving strain

This is why many people include Long-Term Care Insurance as part of a retirement plan. These policies provide tax-free benefits that can help cover care at home, assisted living, or nursing facilities—helping protect assets and reduce family burden.

There are hybrid Long-Term Care Insurance policies that combine life insurance with long-term care.

Take Control Before a Crisis Happens

You don’t want your family figuring this out during a time of grief.

You can act now:

- Review your life insurance policy regularly

- Keep beneficiary designations up to date

- Maintain organized records

- Be fully transparent when applying

- Plan for long-term care alongside life insurance

Life insurance is meant to protect your family—but preparation ensures it works as intended. Start the conversation today—before a crisis forces decisions your family isn’t ready to make. Be sure you've reviewed your (or a loved one's) policies, so you don't assume everything is already in place.

Frequently Asked Questions

Can artificial intelligence affect life insurance claims?

Yes. Some insurers now use AI to process claims more quickly, but experts have raised concerns that automation may lead to faster denials without full human review.

Does life insurance pay for suicide?

Most policies include a suicide clause. If death occurs within the first two years, benefits are usually denied and premiums refunded. After that period, coverage may apply depending on the policy terms and state laws.

How long does it take to receive a life insurance payout?

Most claims are processed within 30 to 60 days, but disputes or missing documentation can significantly delay payment.

What is the contestability period in life insurance?

The contestability period is typically the first two years after a policy is issued. During this time, insurers can review the application for errors or omissions that could lead to a denial.

Can you appeal a denied life insurance claim?

Yes. Many denied claims can be appealed successfully by reviewing the denial letter, gathering supporting documentation, and following the insurer’s appeals process.

What happens if there is no beneficiary listed?

If no beneficiary is named, the death benefit is typically paid to the policyholder’s estate, which may require probate and delay access to funds.

How often are life insurance claims denied?

Estimates suggest about 10% to 20% of claims face delays or initial denials, often due to application errors or missing documentation.

Why would a life insurance claim be denied?

Life insurance claims are most often denied due to misrepresentation on the application, policy exclusions, missed premium payments, or administrative issues such as incomplete paperwork or beneficiary disputes.

What are the chances of winning an appeal?

While few people appeal, about 40% of appealed life insurance claim denials are overturned in favor of the beneficiary.