Nebraska Long-Term Care Tax Credit Proposal Fails — But Key Tax Benefits Still Exist

About This Article

Nebraska’s LTC tax credit proposal failed, but key tax benefits remain to help Nebraskans protect assets from the rising cost of long-term care services.

James Kelly

LTC News staff writer specializing in long-term care and aging.

Table of Contents

- Proposal Aimed to Encourage Planning — But Didn’t Advance

- Nebraska’s Budget Reality Slows Policy Changes

- Nebraska Long-Term Care Savings Plan: A Hidden Tax Break You Should Understand

- The Key Tax Benefit: State Income Tax Deduction

- Who Can Use It? More Flexible Than You Think

- What Counts as a Qualified Expense?

- The Catch: Penalties for Non-Qualified Use

- Why This Plan Matters More Than the Failed Tax Credit

- What Other Tax Benefits Still Exist?

- Asset Protection Through Partnership Policies

- Why Long-Term Care Planning Matters More Than Ever

- What Happens Next?

- Bottom Line: You Still Have Powerful Planning Tools

- Take Control Before It Becomes a Crisis

- Prepare Now for Future Aging

For most of us, long-term care is a "someday" problem—a shadow on the horizon we’ll deal with when the sun starts to set. We don’t think about the logistics of aging until the phone rings in the middle of the night, or until a routine doctor’s visit ends with a diagnosis that changes everything. It’s in that jarring moment, when a slip on the ice or a sudden lapse in memory steals a loved one’s independence, that the financial reality of the future finally hits home.

Nebraska lawmakers had the chance to soften that blow. A proposed tax break aimed to incentivize families to plan ahead, offering a rare bit of proactive support for the grueling costs of elder care. It was a bid to turn "someday" into "today."

However, as we move through 2026, that hope has hit a legislative dead end. Despite the growing urgency of an aging population and the concern for access to quality extended care, the proposal failed to become law, leaving Nebraskans to navigate the high-stakes maze of long-term care planning with other options to prepare for the consequences of aging.

Quick Takeaways

- Nebraska’s proposed LTC Insurance tax credit did not pass

- The state still offers a Long-Term Care Savings Plan deduction

- Federal tax benefits for LTC Insurance remain available

- Benefits from LTC Insurance are generally tax-free

- Planning early helps protect savings and reduce family burden

Proposal Aimed to Encourage Planning — But Didn’t Advance

You’ve probably thought about it at some point—what happens when you or a loved one needs long-term care? The impact of long-term care is both a cash flow problem and a family problem. Unfortunately, too many Nebraskans, like most Americans, ignore the problem until the family crisis forces them into action. At that point, options are limited, and the pressure on the family can often be life-changing.

A proposal introduced by state Senator Merv Riepe (R-District 12) would have created a state income tax credit equal to 25 percent of Long-Term Care Insurance premiums, capped at:

- $250 for individuals

- $500 for couples

The goal was simple: encourage earlier planning and reduce reliance on Medicaid, which requires an individual to have limited financial resources to qualify.

But as of this update, March 2026:

- The bill did not pass

- It failed to advance out of committee

- It is not part of Nebraska law today

Lawmakers, including former state senator Sara Howard, acknowledged the growing pressure an aging population places on state budgets, but fiscal constraints have slowed the adoption of new tax incentives.

Nebraska’s Budget Reality Slows Policy Changes

Nebraska faces the same challenges seen across the country:

- Rising long-term care costs

- Increased Medicaid spending

- A rapidly aging population

These pressures make reform necessary—but also difficult.

Even widely supported ideas, like tax incentives for Long-Term Care Insurance, can stall despite bipartisan interest.

Nebraska Long-Term Care Savings Plan: A Hidden Tax Break You Should Understand

You might assume Nebraska offers no meaningful tax incentives for long-term care planning—especially after the proposed tax credit failed.

But that’s not entirely true.

Nebraska already has a lesser-known but valuable tax advantage: the Nebraska Long-Term Care Savings Plan.

What Is the Nebraska Long-Term Care Savings Plan?

This plan is not insurance, but it’s a state-recognized savings account designed specifically for future long-term care costs. You can establish one through an approved financial institution, and the funds can be used for:

- Long-term care services, including home care and facility care

- Long-Term Care Insurance premiums

- Qualified care expenses tied to aging, chronic illness, or cognitive decline

According to the Nebraska Department of Revenue, the program is outlined under Nebraska Revised Statute Section 77-6103 and administered through approved financial institutions.

👉 Long-Term Care Savings Plan Contribution – State of Nebraska

The Key Tax Benefit: State Income Tax Deduction

Nebraska allows you to deduct contributions from your state taxable income.

As of 2026:

- Up to $1,000 per year (individual)

- Up to $2,000 per year (married filing jointly)

This deduction reduces your Nebraska taxable income each year you contribute.

👉 You cannot claim the same contribution as a tax benefit under both federal and state rules for the same purpose.

Who Can Use It? More Flexible Than You Think

This plan is designed for early planning:

- No age requirement to contribute

- Funds can be used later for care

- Or beginning at age 50, for Long-Term Care Insurance premiums

That makes it especially valuable if you’re in your 40s or 50s and planning ahead.

What Counts as a Qualified Expense?

To maintain the tax advantage, funds must be used for qualified long-term care purposes, including:

- Assistance with activities of daily living (bathing, dressing, mobility)

- In-home care or facility-based care

- Long-Term Care Insurance premiums for yourself, your spouse, or another eligible individual

The Catch: Penalties for Non-Qualified Use

If funds are used for non-qualified expenses:

- A 10 percent penalty applies

- Previously deducted amounts must be added back to income

This ensures the account is used strictly for long-term care planning.

Why This Plan Matters More Than the Failed Tax Credit

While the proposed tax credit would have provided a limited annual benefit, this savings plan offers:

- Ongoing annual tax deductions

- A way to build a dedicated care fund over time

- Flexibility to pay for care or LTC Insurance

It’s not widely discussed—but it’s already available and actionable today.

What Other Tax Benefits Still Exist?

Even without a state tax credit, Nebraska residents still have multiple ways to reduce the financial impact of long-term care planning.

- Federal Tax Deductions

You may deduct qualified Long-Term Care Insurance premiums as medical expenses:

- Subject to IRS age-based limits

- Must exceed 7.5% of adjusted gross income

The Internal Revenue Service updates these limits annually, allowing higher deductions as you age.

- Self-Employed and Business Owners

If you are self-employed:

- You can deduct 100% of premiums (within IRS limits)

- No need to itemize

This remains one of the most valuable tax advantages available.

- Health Savings Accounts (HSA)

If you have an HSA:

- You can use pre-tax funds to pay premiums

- Subject to IRS limits

- Tax-Free Benefits

Perhaps the most important advantage that is available when you have Long-Term Care Insurance is that the benefits are tax-free, even if you can deduct the premium.

👉 Benefits from Long-Term Care Insurance are generally tax-free.

This applies whether care is received:

- At home

- In assisted living

- In memory care

- In a nursing facility

Asset Protection Through Partnership Policies

Nebraska participates in the Long-Term Care Partnership Program, which allows you to protect assets equal to the amount your policy pays in benefits.

For example:

- If your policy pays $475,000

- You can protect $475,000 in assets from Medicaid spend-down

Why Long-Term Care Planning Matters More Than Ever

You’re living longer—but longevity brings new risks. A report from the U.S. Department of Health and Human Services (Office of the Assistant Secretary for Planning and Evaluation) states that about 56% of Americans will need long-term services and supports that meet the federal definition of long-term care.

At the same time:

- More than 63 million Americans now provide unpaid care, a 45% increase since 2015

- Costs continue to rise nationwide, driven by labor shortages and increasing demand for services

- Families provide most care unpaid

And there’s a critical gap many people don’t realize:

👉 Medicare and traditional health insurance only cover short-term skilled care—typically up to 100 days—and do not pay for ongoing long-term care services - Medicare Falls Short on Long-Term Care: Families Face Financial Strain

That leaves many families unprepared.

“Too often people don’t think about long-term care until it is too late. These plans are far more affordable when purchased in your 40s and 50s while you’re still healthy.” — Matt McCann, long-term care planning specialist.

What Happens Next?

The Nebraska tax credit proposal is not law, but the conversation is far from over. As Medicaid costs grow and more families face caregiving challenges:

- Expect renewed legislative proposals

- Increased focus on private planning solutions

- Continued discussion around tax incentives

More than 25 states already offer some form of tax incentive for Long-Term Care Insurance, putting pressure on states like Nebraska to revisit the issue.

Bottom Line: You Still Have Powerful Planning Tools

The proposed tax credit didn’t pass—but you are not without options.

You can still leverage:

- Nebraska’s Long-Term Care Savings Plan

- Federal tax deductions

- Tax-free insurance benefits

- Asset protection through partnership policies

Take Control Before It Becomes a Crisis

Too many families wait until something happens—a fall, a diagnosis, or a sudden decline. By then, options are limited.

Planning now gives you:

- More control over care decisions

- Protection for your savings

- Relief for your family

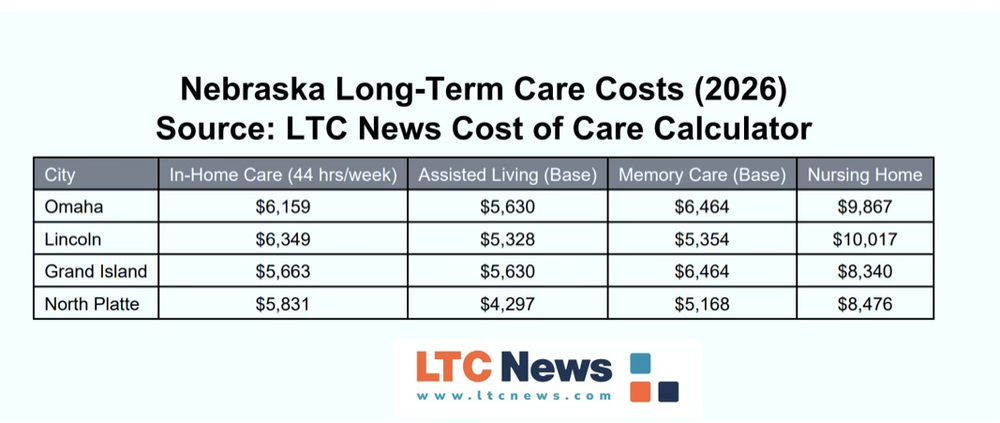

The LTC News Cost of Care Calculator provides one of the most comprehensive, ZIP code–based cost comparisons available, based on ongoing provider surveys nationwide. You can also find local care providers for older family members by searching through the LTC News Caregiver Directory.

The cost of long-term care services is increasing nationwide, and you can see this throughout Nebraska.

Prepare Now for Future Aging

If you needed care tomorrow, would your plan protect your independence—or leave your family scrambling? Can you protect your home, farm, or business? Can you reduce the stress and burden that would normally be placed on your loved ones?

Long-Term Care Insurance can be very helpful. However, be sure to get the help of a qualified LTC Insurance specialist when getting quotes and discussing policy design. Most financial advisors and general insurance agents lack the skills and experience in long-term care.

LTC News can vetted insurance agents who specialize in long-term care. The vetted specialists who partner with LTC News are independent, highly experienced professionals dedicated to long-term care planning. Many hold the Certified in Long-Term Care (CLTC) designation — the industry’s most recognized credential — and are endorsed by the American Association for Long-Term Care Insurance (AALTCI). Several are also Ramsey Trusted Pros, recommended by Dave Ramsey’s organization for their integrity and expertise. In addition, some maintain strong ties with Christian and Jewish community groups, underscoring their commitment to ethical service and values-based guidance.

This article is for informational purposes only and should not be considered tax or financial advice. Consult a qualified tax professional regarding your specific situation.