How to Protect Your Assets Before a Long-Term Care Crisis

About This Article

Long-term care costs can drain your savings fast. There are several ways to protect your assets, understand Medicaid rules, and plan now before a crisis strikes.

James Kelly

LTC News staff writer specializing in long-term care and aging.

Table of Contents

- Why Long-Term Care Planning Can’t Wait

- What Long-Term Care Really Costs Today in the U.S.

- What Long-Term Care Actually Includes

- The Biggest Mistake: Assuming Medicare Covers It

- Medicaid: The Safety Net with Strict Rules

- The Spend-Down Reality

- The Medicaid Look-Back Rule: A Critical Trap

- How You Can Protect Your Assets

- Does a Living Trust Protect Your Assets?

- Option Many Families Overlook

For many families, the transition to long-term care isn't a choice it's a crisis. It often begins with a single phone call: a parent has fallen, a spouse has received a life-altering diagnosis, or a gradual decline in health has reached a breaking point. Other times, it is a gradual decline due to aging.

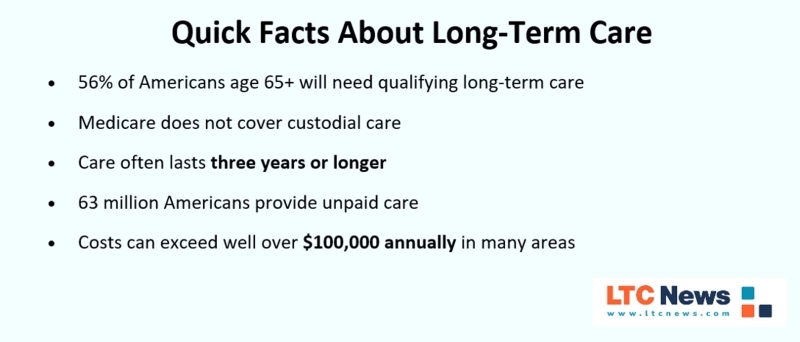

What starts as a few hours of weekly assistance often spirals into a 24-hour necessity, exposing a harsh financial reality that many Americans overlook until it is too late. Experts warn that without a proactive strategy, the soaring costs of professional care can rapidly deplete a lifetime of retirement savings.

Effective long-term care planning is increasingly being viewed by financial advisors not as an "extra" insurance step, but as a fundamental pillar of retirement security. Beyond the balance sheet, it is a race to maintain personal autonomy—ensuring that an individual’s care, independence, and ultimate legacy remain under their own control.

Looking for quality long-term care services for a loved one right now? Use the LTC News Caregiver Directory and search from over 80,000 providers nationwide. If they have Long-Term Care Insurance get free help processing the claim — File a Long-Term Care Insurance Claim.

Why Long-Term Care Planning Can’t Wait

It’s easy to assume long-term care is something that happens to “other people”—or something you can deal with later. But aging doesn’t wait for the perfect time, and neither do health events.

For many families, the need for care begins gradually. Maybe it starts with getting help around the house. Then rides to appointments. Then assistance with daily routines. Before long, those small needs become ongoing care, help with the daily living activities most of us take for granted.

They’re managing medications, coordinating appointments, assisting with essential needs like bathing and dressing … many are doing all of this while working. — Myechia Minter-Jordan, CEO of AARP, quoted in MarketWatch.

All of this places a lot of pressure on family members, and the financial impact follows quickly as professional caregivers or even facility care becomes required.

You might think it won't happen to you or even your older parents. The facts and common sense say otherwise. Federal government research shows that 56 percent of Americans who reach age 65 will require long-term services.

Higher estimates—such as 70 percent—often include people needing minimal assistance, which does not meet the legal definition of long-term care. The only statistic that matters is it will happen, or not, and when it does, you want to avoid the family crisis.

That’s not a small risk. It’s a coin flip—and one that carries serious physical, emotional, and financial consequences.

What Long-Term Care Really Costs Today in the U.S.

The cost of long-term care is one of the most underestimated risks in retirement planning. Many people assume care will be short-term or manageable. In reality, even part-time help can quickly turn into a major monthly expense that, in some cases, will last for years.

The costs of extended care vary widely depending on where you live and the level of care required. What begins as a few hours of help each week can evolve into daily assistance—or even 24-hour care.

The LTC News Cost of Care Calculator—based on monthly provider surveys nationwide—shows the real financial exposure:

- In-home care: often $5,000 to $7,000+ per month, depending on hours

- Assisted living: the base costs before sur-charges typically run $4,500 to $7,500+ monthly

- Nursing home care: frequently exceeds $9,000+ per month

These are not short-term bills. They are ongoing expenses that can last for years. Market volatility can make this risk even more severe, forcing families to sell investments at a loss to pay for care.

According to the Administration for Community Living, most people who need long-term care require services for about three years, with longer durations for some people, like those living with dementia.

These numbers highlight the scope of the issue, but understanding what care actually involves is just as important.

What Long-Term Care Actually Includes

When people hear “long-term care,” they often picture a nursing home. But that’s only one part of the story—and often not where care begins.

Most long-term care begins at home and gradually increases over time. It’s not always medical. In fact, much of it involves helping with everyday tasks that become harder with age or illness.

Spouses, siblings, children and other family members are the ‘cornerstone’ of the United States’ long-term care system. - says Jennifer Ailshire, a professor of gerontology at the University of Southern California, quoted in the Washington Post.

This type of support is called custodial care—and it forms the foundation of long-term care services.

It includes:

- Help with bathing, dressing, and mobility

- Meal preparation and medication reminders

- Supervision for dementia or Alzheimer’s disease

- Support after illness, injury, or surgery

Understanding this distinction is critical—because it directly affects how care is paid for.

The Biggest Mistake: Assuming Medicare Covers It

One of the most costly misunderstandings in retirement planning is believing Medicare will cover long-term care. It’s an easy assumption to make. After all, you’ve paid into Medicare your entire working life. But Medicare was never designed to cover ongoing personal care needs.

Instead, it focuses on short-term medical recovery, not long-term support.

Medicare:

- Covers only short-term skilled care

- Requires a qualifying hospital stay

- Pays fully for the first 20 days, then partially up to 100 days

- Provides no coverage for ongoing custodial care

That means:

- No long-term home care coverage

- No assisted living coverage

- No extended nursing home coverage

What would happen if you needed care tomorrow—who would step in, and how would you pay for it?

Medicaid: The Safety Net with Strict Rules

When Medicare falls short, many families eventually turn to Medicaid after the money runs out, and family members can no longer be caregivers. But Medicaid is not a simple solution—it’s a solution of last resort with strict financial requirements.

Medicaid is designed for individuals with limited income and assets. To qualify, you must meet very specific financial thresholds, which often means spending down much of what you’ve saved.

Typical eligibility includes:

- About $2,000 in countable assets (individual)

- Limited income thresholds

- State-specific protections for spouses

Countable assets include:

- Savings and investments

- Retirement accounts (depending on state rules)

- Additional property

Even your home, while often protected initially, may be subject to estate recovery after death.

The Spend-Down Reality

To qualify, many families must:

- Liquidate savings

- Sell assets

- Exhaust financial resources

This process can leave a healthy spouse financially vulnerable, sometimes forcing difficult financial and lifestyle decisions, and significantly reducing what you can pass on to your family.

The Medicaid Look-Back Rule: A Critical Trap

Many families believe they can simply transfer assets to children when care is needed. Unfortunately, Medicaid rules are designed to prevent exactly that.

The five-year look-back period allows Medicaid to review all financial transactions before approving an application. This rule is established under federal law through the Deficit Reduction Act of 2005 and enforced by each state Medicaid program.

Under the federal Deficit Reduction Act of 2005, Medicaid officials are required to "look back" at every financial transaction an applicant has made in the 60 months preceding their application. This forensic audit is designed to ensure assets weren't gifted simply to qualify for state aid.

The "Disqualifying" List:

- Direct Gifts: Writing a check to a grandchild for tuition.

- Property Transfers: Signing the family home over to children.

- Under-Market Sales: Selling a vehicle or asset to a friend for a "bargain" price.

Violating these rules triggers a penalty period, a period during which Medicaid coverage is denied. Unlike older laws, this clock only starts ticking once the applicant is already in a care facility and has exhausted their savings.

The Math of a Mistake: If a senior gifts $120,000 to family and later requires long-term care, they could face a penalty lasting a year or more. During that time, the family is left to foot a massive private-pay bill with a bank account that is already at zero.

It’s worth noting that certain transfers are exempt from these penalties, such as transfers to:

- A spouse.

- A child who is blind or permanently disabled.

- A "Caregiver Child" (who lived in the home and provided care for at least two years before institutionalization).

How You Can Protect Your Assets

There is no one-size-fits-all solution to protecting your assets from long-term care costs. The right strategy depends on your health, finances, and how early you begin planning.

Planning must begin at least five years before care is needed, and those planning with Long-Term Care Insurance often obtain coverage in their 40s or 50s. Most people purchase LTC Insurance between the ages of 47 and 67.

What is clear, however, is this: the earlier you act, the more options you have—and the more flexibility you retain.

1. Long-Term Care Insurance

One of the most effective ways to protect your assets is through Long-Term Care Insurance. These policies are specifically designed to cover the types of care Medicare and health insurance do not—allowing you to use tax-free insurance dollars instead of personal income and assets.

A Long-Term Care Insurance policy helps pay for:

- Home care

- Adult day care

- Assisted living

- Memory care

- Nursing home care

It allows you to:

- Protect your income and assets

- Maintain independence

- Access your choice of quality care, even at home

- Reduce the burden on family

Premiums are based on age and health, making early planning critical.

2. Partnership Long-Term Care Insurance

Partnership policies are a type of LTC policy that adds another layer of protection by allowing you to preserve assets while still qualifying for Medicaid. These policies are available in most states and are designed to encourage early planning.

- They provide: Dollar-for-dollar asset protection.

Example:

- A policy that paid $300,000 in benefits allows you to protect $300,000 in assets in a process called "asset disregard." The benefits paid by the policy will equal the amount the government will ignore when calculating your qualification for Medicaid. In other words, you or your loved one will not have to be poor to qualify for Medicaid.

The goal is not to get to Medicaid, but if you exhaust all the benefits from your Partnership LTC policy, you can qualify for Medicaid without being poor.

3. Medicaid Asset Protection Trust (MAPT)

For those planning well in advance, a Medicaid Asset Protection Trust can be an effective tool. These trusts are designed to remove assets from your countable estate—but they require careful planning and strict compliance.

An irrevocable trust can:

- Remove assets from Medicaid calculations

- Preserve wealth for future generations

But only if:

- Established more than five years before care is needed

- You give up control of the assets

4. Caregiver Agreements

Family caregiving is common—but without proper structure, financial support can create problems under Medicaid rules. A formal caregiver agreement (often called a Personal Care Agreement) allows you to compensate family members legally while avoiding penalties.

These agreements can:

- Provide income to caregivers

- Help preserve assets

- Ensure compliance with Medicaid regulations

However, for them to be "Medicaid-compliant" and avoid being flagged as an improper "gift," they must meet several strict federal and state criteria.

Without a formal contract, money paid to a family member is almost always treated by Medicaid as a gift, triggering a penalty period. Plus, most people want to avoid having a loved one be their caregiver.

Does a Living Trust Protect Your Assets?

One of the most common—and expensive—misconceptions in retirement planning is the belief that a "Living Trust" is a shield against the skyrocketing costs of long-term care. For many, the realization that their assets are still vulnerable comes only when they are sitting in a Medicaid office.

To understand why, you have to look at the "fine print" of the trust itself.

1. The Revocable Living Trust: Flexibility Without Protection

Most people choose a Revocable Living Trust for its primary benefit: avoiding probate. Because you retain total control and can "revoke" or change the trust at any time, the law treats those assets as if they are still in your pocket.

If all you need is a living trust, families can learn how to set up a trust without an attorney, as online platforms have made revocable trusts accessible and affordable for straightforward estates. But a revocable trust alone is not a long-term care plan, nor is it a Medicaid planning tool.

The Verdict: For Medicaid purposes, these assets are fully countable. They must be spent down before the government will provide assistance.

2. The Irrevocable Trust (MAPT): The Protective Shield

To actually safeguard a home or a life savings, the trust must be Irrevocable—specifically a Medicaid Asset Protection Trust (MAPT). This requires a trade-off: you give up the right to change the trust or take the principal back.

The Verdict: Once assets have "seasoned" inside this trust for five years, they are generally no longer counted by Medicaid.

The Bottom Line: A traditional estate plan is designed to manage your assets after you pass away. A long-term care strategy is designed to protect those assets while you are still alive.

Option Many Families Overlook

Despite the financial risk, many people delay or avoid planning altogether. Some assume they will never need care. Others believe they can address it later.

But timing matters.

By the time many people consider Long-Term Care Insurance:

- Health issues may limit eligibility

- Premiums are significantly higher if you have not planned until you are in your 70s or have substantial health issues

Most long-term care needs don’t begin in a facility, they begin quietly at home and grow over time.

Without a plan, families often rely on:

- Spouses

- Adult children

- Out-of-pocket spending

Long-Term Care Insurance, in all its various forms, is often the best way to safeguard income and assets, ensure access to quality care, and ease family stress and burden. Be sure to seek professional help from an experienced, qualified Long-Term Care Insurance specialist to obtain accurate quotes and recommendations.

When you ask for information through LTC News, we transfer you to professionals, as LTC News does not sell insurance. The vetted specialists who partner with LTC News are independent, highly experienced professionals dedicated to long-term care planning. Many hold the Certified in Long-Term Care (CLTC) designation — the industry’s most recognized credential — and are endorsed by the American Association for Long-Term Care Insurance (AALTCI). Several are also Ramsey Trusted Pros, recommended by Dave Ramsey’s organization for their integrity and expertise. In addition, some maintain strong ties with Christian and Jewish community groups, underscoring their commitment to ethical service and values-based guidance.

Long-term care planning is not about fear, it’s about preparation.

Frequently Asked Questions

Does a living trust protect assets from Medicaid?

No. A revocable living trust does not protect assets from Medicaid because you retain control of those assets. Only an irrevocable trust—such as a Medicaid Asset Protection Trust—can potentially protect assets, and only if established at least five years before care is needed.

What happens if you don’t plan for long-term care?

Without a plan, you may be forced to:

- Pay out of pocket until assets are depleted

- Rely on family members for care

- Qualify for Medicaid under restrictive conditions

Planning ahead gives you more control over your care, finances, and independence.

What is long-term care, and who needs it?

Long-term care refers to ongoing assistance with daily activities such as bathing, dressing, eating, mobility, and supervision due to cognitive decline. According to the U.S. Department of Health and Human Services, about 56% of Americans age 65 and older will need long-term care that meets the federal definition—meaning help with at least two Activities of Daily Living or cognitive impairment.

Where can you find long-term care services near you?

You can use the LTC News Caregiver Directory to search for local providers, compare services, and review current costs in your area. This helps you make informed decisions before care is needed.

How can you protect your assets from long-term care costs?

Common strategies include:

- Long-Term Care Insurance

- Partnership LTC policies (asset protection)

- Medicaid Asset Protection Trusts (MAPTs)

- Caregiver agreements

Each option has specific rules and works best when implemented early—ideally before retirement.

What is the Medicaid five-year look-back period?

The Medicaid look-back period is 60 months (five years). During this time, Medicaid reviews financial transactions to identify asset transfers such as gifts or below-market sales. Violations can result in a penalty period during which Medicaid will not pay for care.

How much does long-term care cost in the U.S.?

Costs vary by location and level of care, but current data from the LTC News Cost of Care Calculator shows:

- In-home care: $5,000 to $7,000+ per month

- Assisted living: $4,500 to $7,500+ per month

- Nursing home care: $9,000+ per month

These costs can last several years, creating a significant financial burden without proper planning.

Can you give assets to family members to qualify for Medicaid?

Not without consequences. Giving assets away during the five-year look-back period can trigger penalties that delay Medicaid eligibility. Certain transfers—such as to a spouse or disabled child—may be exempt, but most gifts will be penalized.

What is Long-Term Care Insurance and how does it work?

Long-Term Care Insurance is designed to cover services not paid for by Medicare, including:

- In-home care

- Assisted living

- Memory care

- Nursing home care

Policies provide tax-free benefits that help protect income and assets while allowing you to choose where and how you receive care.

Does Medicare pay for long-term care?

No. Medicare only covers short-term skilled care after a qualifying hospital stay. It does not pay for ongoing custodial care such as help with bathing, dressing, or supervision for dementia, whether at home or in a facility.

How long do people typically need long-term care?

According to the Administration for Community Living, most people who need long-term care require services for about three years, with longer durations common for individuals with dementia or chronic illness.

What is the difference between Medicare and Medicaid for long-term care?

- Medicare is health insurance for medical treatment and short-term recovery.

- Medicaid is a government assistance program that may cover long-term care—but only after you meet strict income and asset limits.

Medicaid often requires individuals to spend down most of their savings before qualifying.

When is the best time to buy Long-Term Care Insurance?

Most people purchase coverage between ages 47 and 67. Applying earlier generally means:

- Lower premiums

- Better health qualification

- More coverage options

Waiting too long can result in higher costs—or being declined due to health conditions.